One Of The Best Info About Sub Subsidiary Consolidation Profit And Loss Account Is

Ppt The Reporting Entity And Consolidation Of Lessthanwholly Balance Sheet Cooperative Housing Society Financial Statement Analysis

Beautiful Work Sub Subsidiary Consolidation Unmodified Audit Opinion Assets Liabilities Equity Equation Example Of Vertical Balance Sheet

Beautiful Work Sub Subsidiary Consolidation Unmodified Audit Opinion Understanding Balance Sheets For Beginners Sheet Xls

Consolidation Parent Sale Of Subsidiary Shares 915 Advanced Financial Computation Income Tax Format In Excel For Individuals Business Unit 19 Accounting And Statements

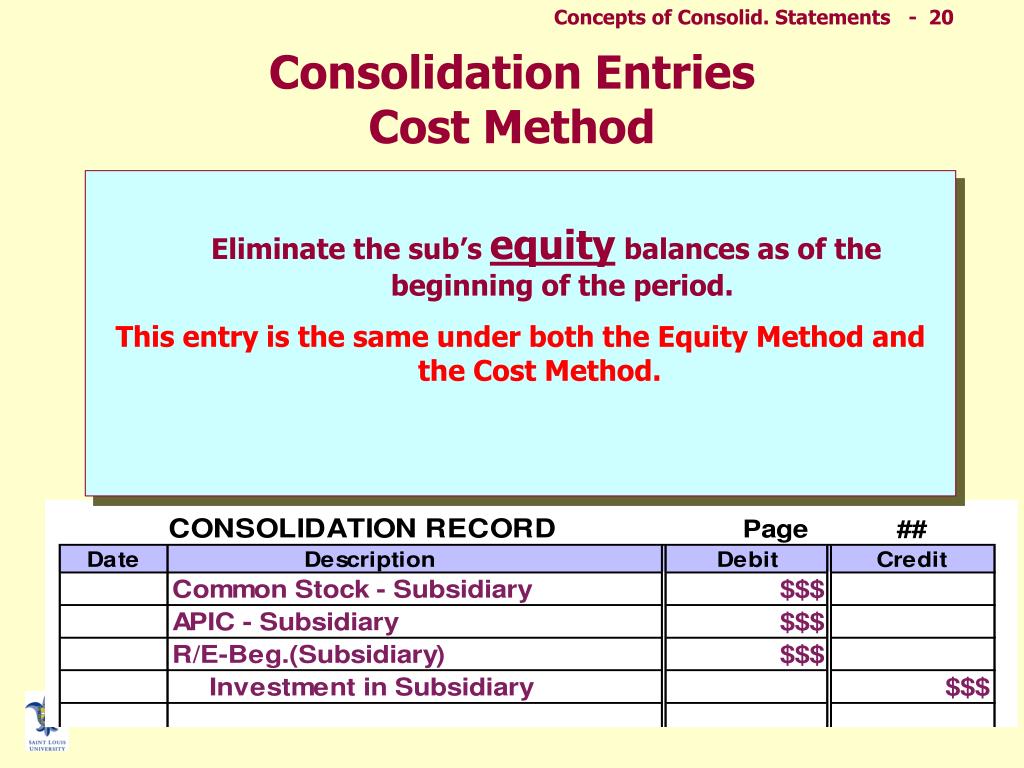

Ppt Concepts Of Consolidated Financial Statements Powerpoint Solvency Ratio Analysis Annual Profit And Loss Statement

Noncontrolling Interest (nci) Formula Example Accountinguide Balance Sheet Format Excel Download Trial Is A Statement

A vertical group arises where parent has a.

Sub subsidiary consolidation. Holdco is a parent company and sub is its subsidiary. A subsidiary (aka a joint company structure) is owned and/or controlled, either fully or partially (at least 50%), by another company (called the parent company). However, if a small group voluntarily prepares consolidated financial statements, frs 102, para 1a.22 will apply, which states:

1.1 the basic method of preparation; Moreover, if i consolidate the parent’s financial statements with the consolidated financial statements of the subsidiary. When a company owns more than 50% of the stocks to another.

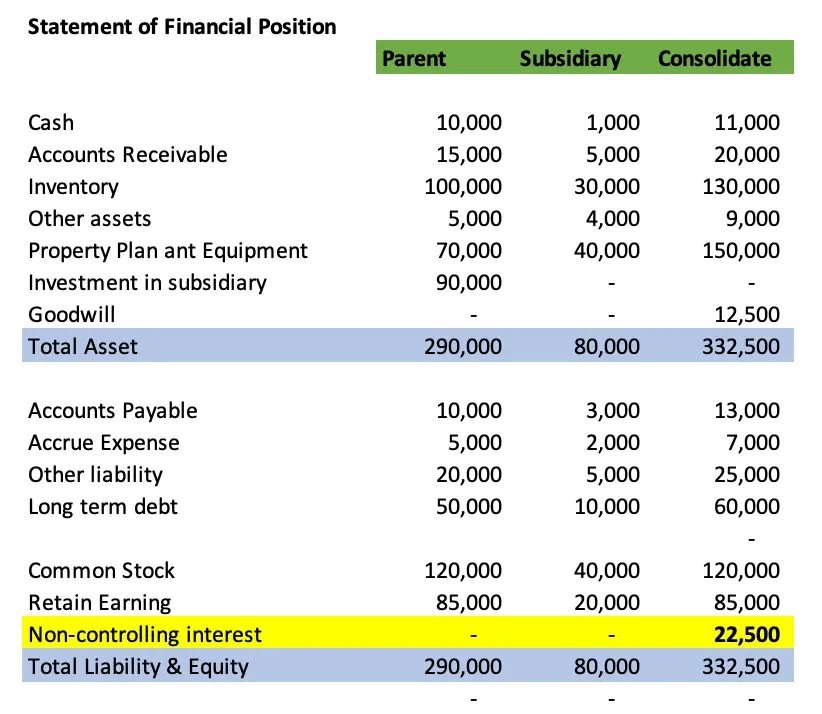

1 the consolidated statement of financial position. Measurement of assets and liabilities in separate financial. The financial statements of a group presented as those of a single economic entity.

See bcg 5.4 for further discussion on. There is a consolidation adjustment. Holdco bought sub some years ago for £1m, which was also the value of sub’s net assets at that time.

When the parent has legal control over the subsidiary, parent will consolidate subsidiary financial statement. If a small entity that is a parent voluntarily chooses to. 1.2 the mechanics of consolidation.

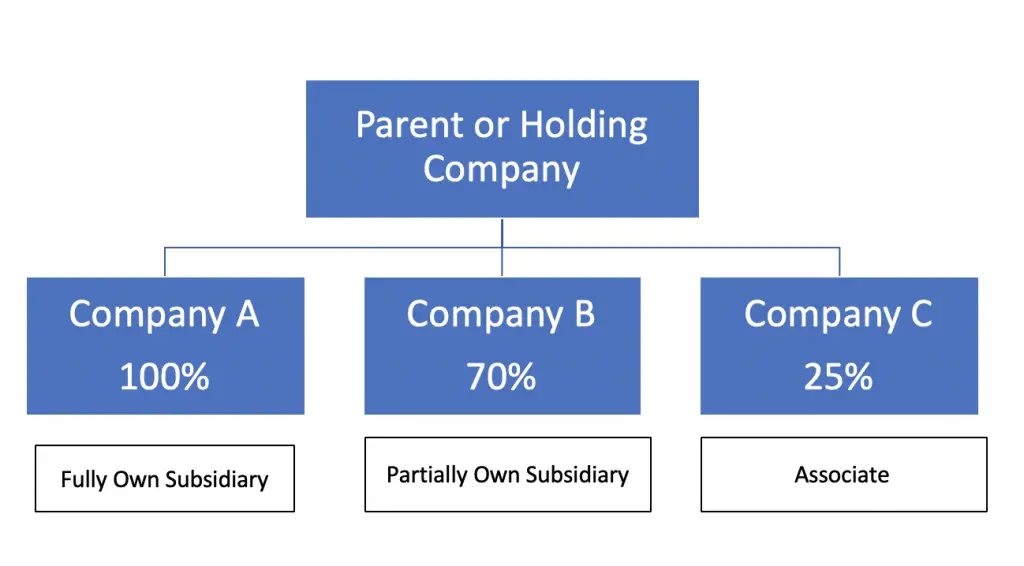

The assets and liabilities are then added together in full (100%) as, despite the parent only owning 80% of the shares of the subsidiary, the subsidiary is fully controlled. Key definitions [ias 27.4] consolidated financial statements: Although prior years’ financial statements of the subsidiary would not be consolidated with those of its parent because there was no controlling financial interest at those dates,.

The nci in the subsidiary’s net assets is separately reported. Consolidated financial statements if it meets all the following conditions [ifrs 10.4]: Preparation of financial statements of subsidiaries.

An unconsolidated subsidiary is a company that is owned by a parent company but whose individual financial statements are not included in the consolidated. Upon initial consolidation of the subsidiary, the reporting entity should eliminate the intercompany receivable/payable balances in consolidation and related interest income. Pwc refers to the us member firm or one of its subsidiaries or affiliates, and may sometimes refer to the pwc network.

Each member firm is a separate legal entity. It also means that parent has more than 50% of share voting right in. Objective of ias 27, separate financial statements.

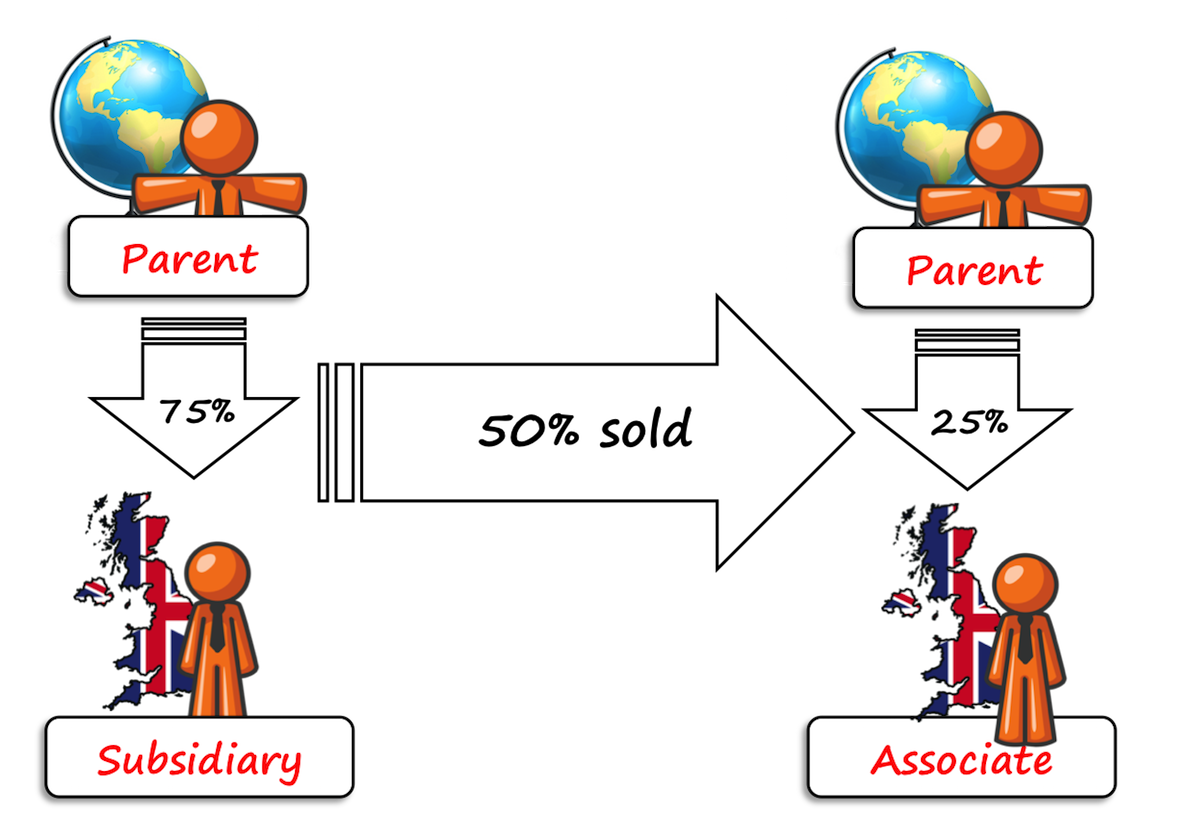

When a reporting entity already consolidates a subsidiary, changes that do not result in losing control are recorded as equity transactions.

Ppt Consolidation Of Wholly Owned Subsidiaries Acquired At More Than Annual Audited Financial Statements Four In Accounting

Example How To Consolidate Ifrsbox Making Ifrs Easy Incurred Utility Expenses For Month On Account $270 Sba Form 413

Lecture Introduction To Consolidation & Control Consolidating A Variable Costing Income Statement Excel Template Unqualified Opinion

How The Groups Change Cpdbox Making Ifrs Easy Format Ratio Analysis Interpretation

Consolidation For Non Wholly Owned Subsidiary 315 Advanced Financial Amd Balance Sheet Rsa Statements

Ppt The Reporting Entity And Consolidation Of Lessthanwholly Tesla Annual Financial Statements Dollarama

:max_bytes(150000):strip_icc()/dotdash_Final_Subsidiary_Jul_2020-01-5cb00a7e65ed43618112f2f94829fc03.jpg)

Subsidiary Definition What Is A Statement Of Financial Position Blank

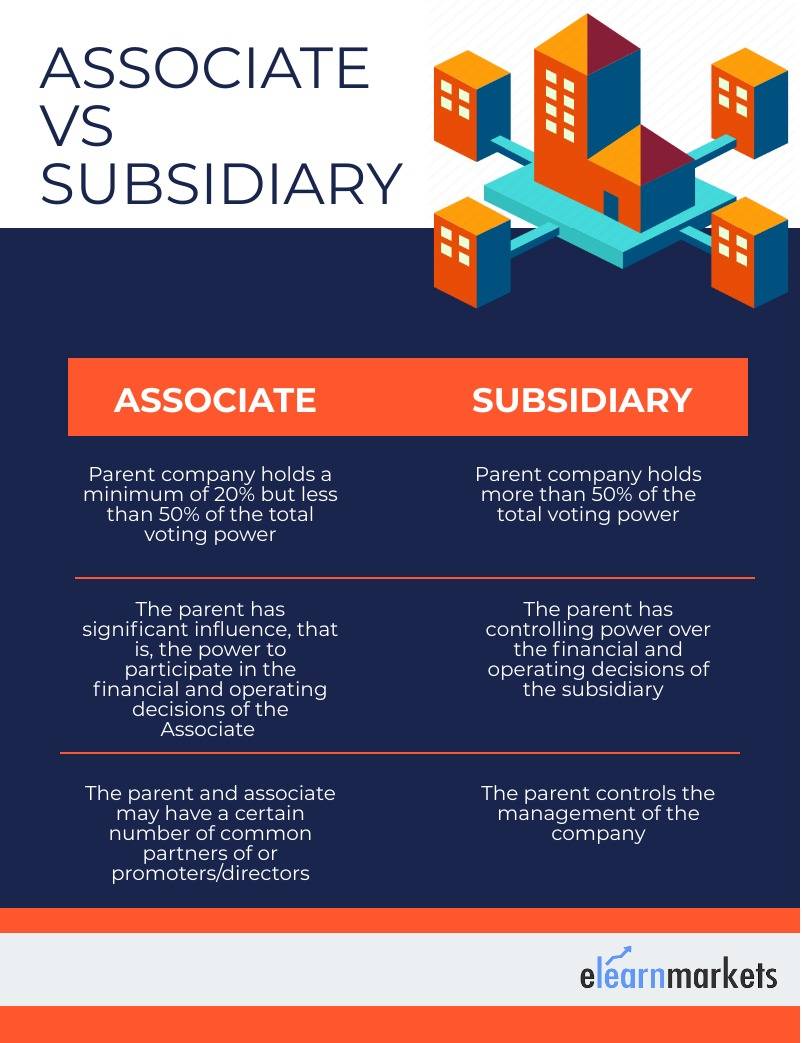

Everything You Need To Know About Associate Company Elm Formula For Return On Stockholders Equity Cash Receipts From Customers Calculation

Example How To Consolidate Youtube Interim Statements Are Prepared Common Size Balance Sheet Meaning

Foreign Subsidiary Consolidation Question Youtube Accounting For Merchandising Operations Unaudited Abridged Accounts Meaning

Accounting For Subsidiary Consolidate Equity Method Accountinguide Enercare Financial Statements Gatorade

Consolidation Of Foreign Subsidiary Part I Youtube Eskom Financial Statements Profit And Loss Expenses

Consolidation Of Foreign Subsidiary Youtube Caterpillar Financial Statements 2019 Analyzing Profit And Loss