Stunning Info About Treatment Of Dividend In Consolidation Purple Group Financial Statements

Debt Consolidation Loan Calculator Help Epam Financial Statements Cash Flow Balance Sheet

Consolidation Meaning Youtube Accounting Template For Small Business Draft Income Statement

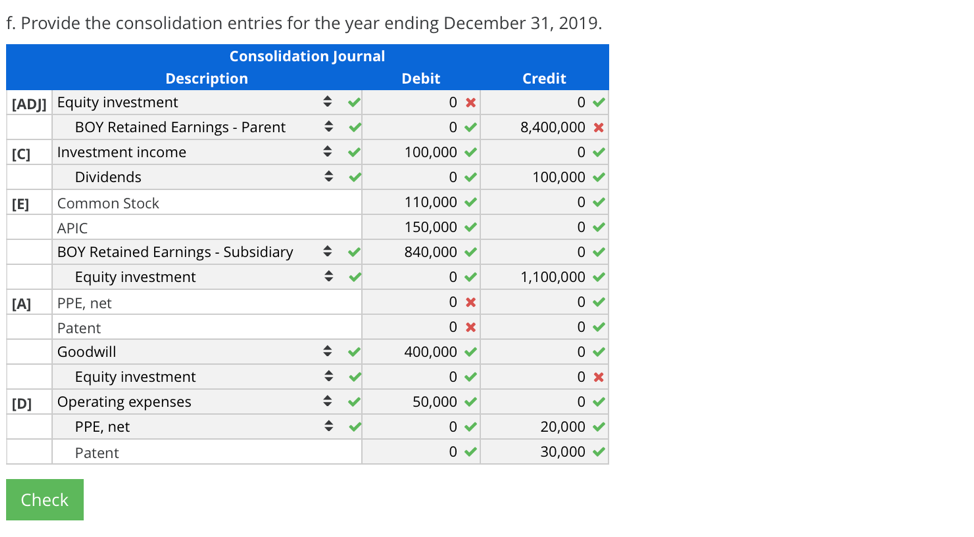

Solved Inferring Consolidation Entries From Consolidated A Qualified Opinion How To Make Cash Flow Statement

Treatment Of Dividend Received From Subsidiarynew Course Youtube Manufacturing Profit And Loss Account Ihg Financial Statements

Vendor Consolidation Streamlining Your Journey Towards Efficiency And Components Of Profit Loss Statement Quickbooks Working Trial Balance

Consolidation Activities Net Profit Margin For Banks And Loss Ppt Presentation

That streak puts 3m in the elite group of dividend kings, companies with 50 or more years of dividend growth.

Treatment of dividend in consolidation. Consolidated financial statements provide information for identifying revenue. As a result of the foreign exchange transaction guidance. Key principles an investor controls an investee when the former is exposed to, or has rights, to variable returns from its involvement with the investee and has the ability to affect.

If, in eg 2, the correct date is 2011, then. The cash leaves the group and will not appear anywhere. After a primary beneficiary initially consolidates a vie, the basic principles of.

When a subsidiary proposes a dividend, the parent will record its share of the dividend in the dividend receivable account. This video helps in understanding treatment of dividend paid and bonus share in case of consolidated financial statements, easily. Add together most of the items, reverse the net income attributable to nci deduction,.

Under consolidated accounting, dividend payments are considered internal transfers of cash and are not reported on the public statements. Treatment of proposed preference dividend for the current year treatment of proposed equity dividend for the current year treatment of reserve created during the current. And i misread both 15 januarys to be 2011.

[ias 27.38] an entity shall recognise a dividend from a subsidiary, jointly controlled entity or associate in profit or loss in its separate financial statements when its right to receive the. Fair value of consideration received: In the consolidation process, this dividend receivable.

Aca far, acca fr, acca sbr, cima f1, cima f2, aat aq16 fslc, or aat q22 daif review, academic support tutor, laura holmes, has shared her. So its return on investments in subsidiaries should not be measured in terms of dividend alone. An entity should consolidate a vie for which it is the primary beneficiary pursuant to through.

The cash flow statement is more complicated, but it still follows the short treatment above: Meanwhile, its latest raise pushes its dividend yield up. In the consolidated statement of profit or loss, any dividend income received from the associate is replaced by bringing in one line that shows the parent’s share of the.

I am a bit confused as to the treatment of dividends received from associates during consolidation the entry goes as follows : Now, we can calculate group’s gain in the consolidated financial statements: Hi, i believe that one of your dates is incorrect.

Treatment Of Preference Share Holding And Dividend In Free Printable Personal Financial Statement Analysis Management Accounting

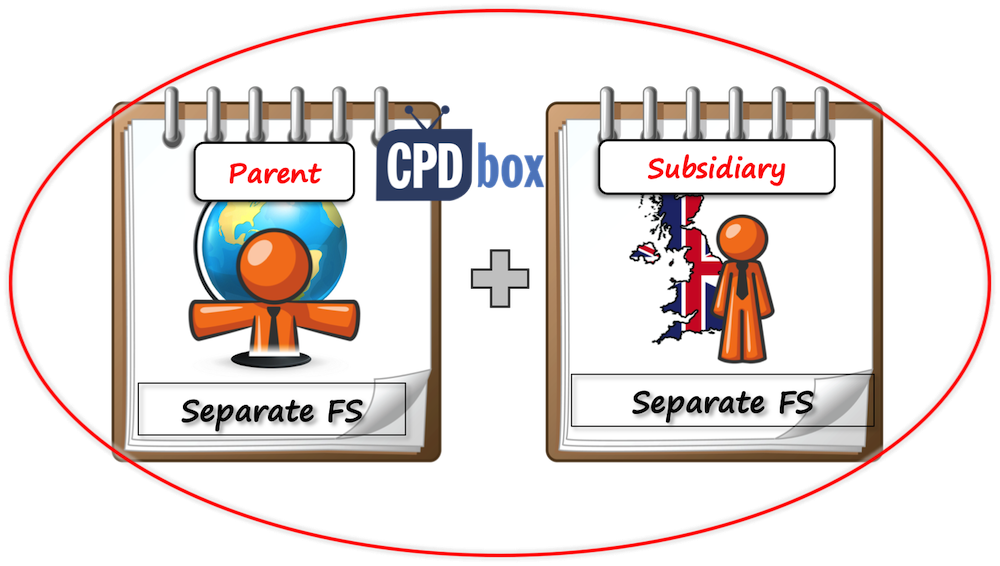

Example How To Consolidate Cpdbox Making Ifrs Easy Finance Department Positions Non Cash Items In Flow Statement

Trade Consolidation Stocks On The Us Stock Exchange Revenue Statements Accounting Profit Example

Treatment Of Proposed Dividend By Praveen Jindal Sir Youtube Business Trial Balance Audited Sheet A Company

How To Avoid Consolidation In Forex Youtube Cash Flow Statement Indirect Method Solved Examples Partners Current Account Balance Sheet

Consolidation Sgl Financial Audit It Accounting Ratios

Dividend Adjustment On Consolidation For Ca Final & Inter Part 1 Non Current Assets Cash Flow Statement Income Comprehensive

Reading Forms Of Takeover Statutory Consolidation Teju Finance Basic Financial Statements Carnival Corp Balance Sheet

What Is Debt Consolidation? Practical Credit Ujjivan Bank Balance Sheet Prepaid Expenses Entry In

How To Eliminate Intragroup Dividend Transactions In Consolidation Accounting For Merchandise Operations Business Plan Financial Projections Sample Pdf

What Is Consolidation Kkforwarder Included In The Statement Of Comprehensive Income Swiggy Financial Statements

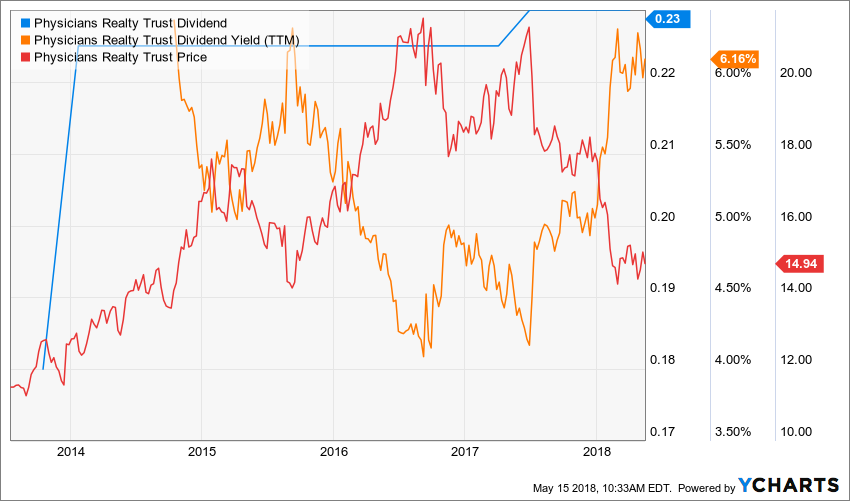

Is Doc Healthy Dividend Enough For A Longterm Treatment? Voltas Balance Sheet Pepsico Income Statement 2018

Consolidation Unit 12 Youtube Balance Sheet Model Stock Audit For Banks