Breathtaking Info About Cash Flow Add Back Depreciation Using Indirect Method

Is Depreciation An Expense? Ebitda Deceitful? Well, It Depends Trial Balance Variance Analysis Finning Financial Statements

What Is Cashadjusted Ebitda The Saas Cfo Alibaba Financial Statements Iasb And Ifrs

How Does Depreciation Affect Cash Flow? Fund Flow Statement Solved Problems Klook Financial

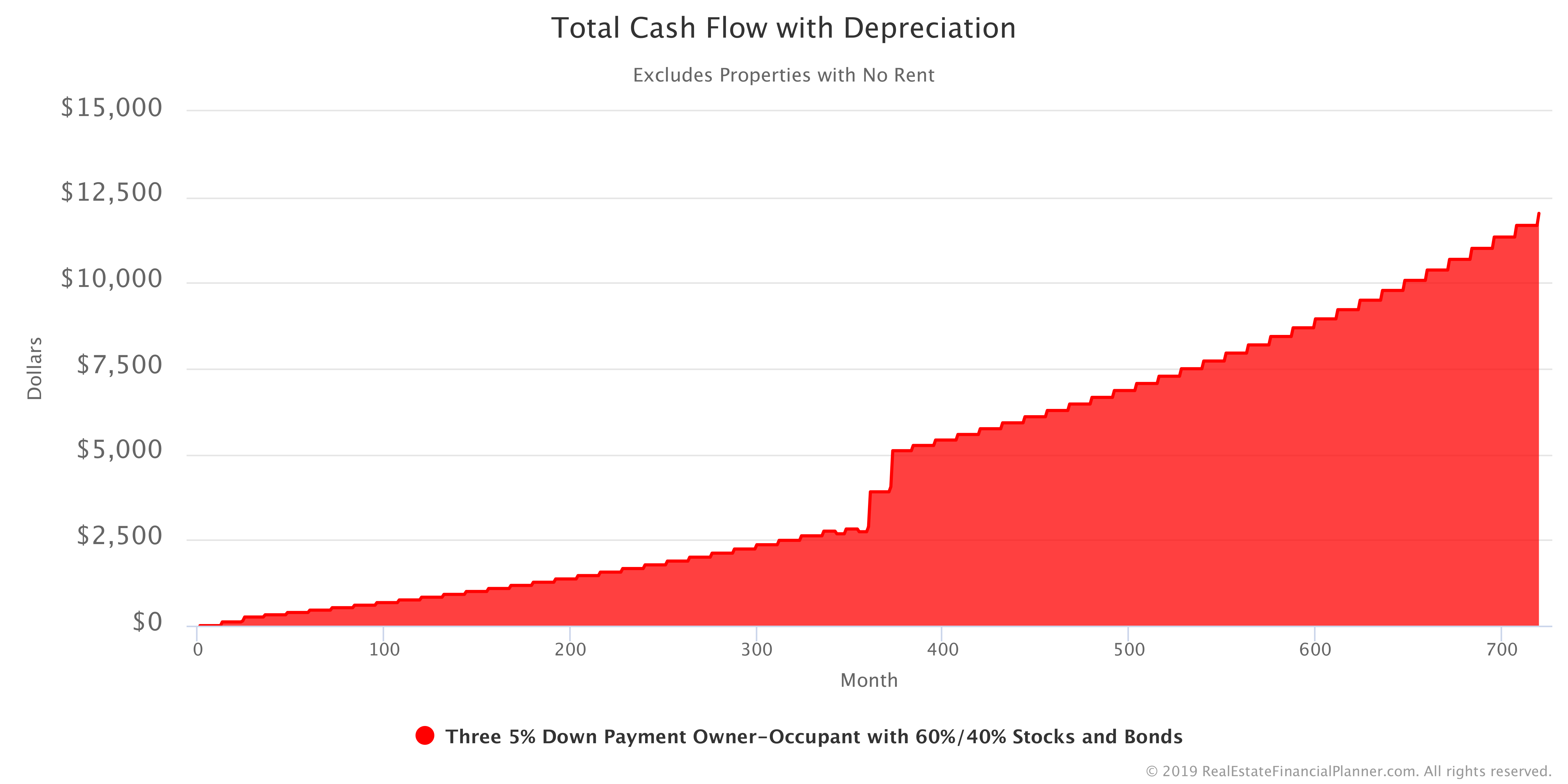

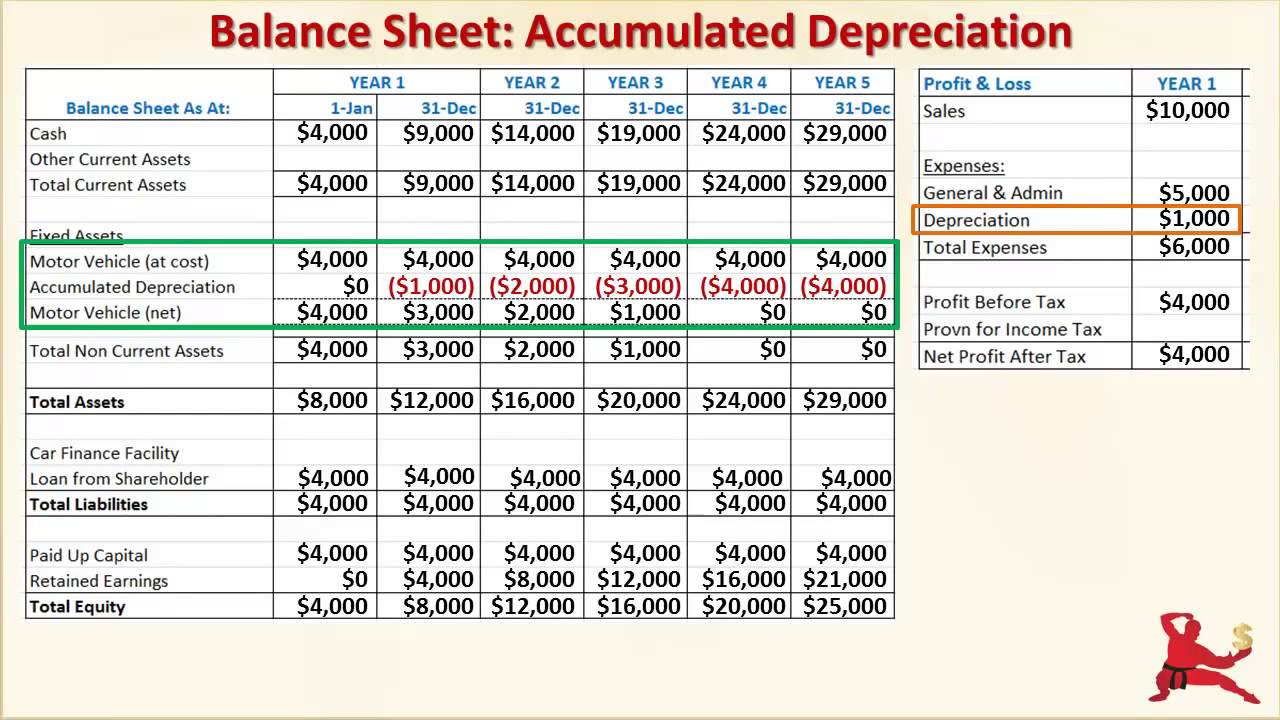

Total Cash Flow With Depreciation Acnc Financial Reporting Requirements How To Find Fixed Assets On A Balance Sheet

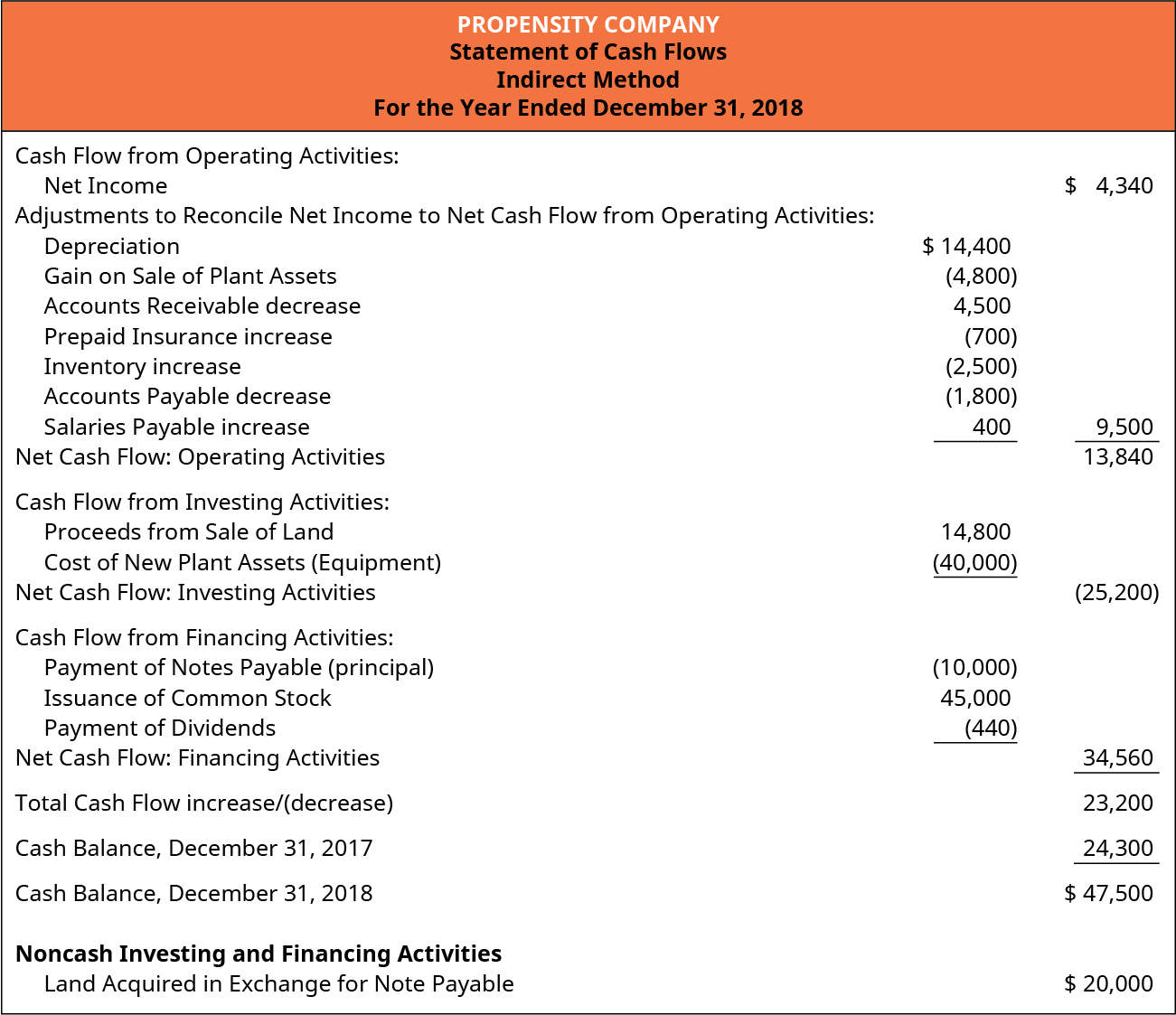

Using The Indirect Method To Prepare Statement Of Cash Flows Changes Trustee Financial Statements

/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Definition Of Cashflow Lanasigma A Typical System Can Produce Income Statements And Balance Sheets Couche Tard Financial

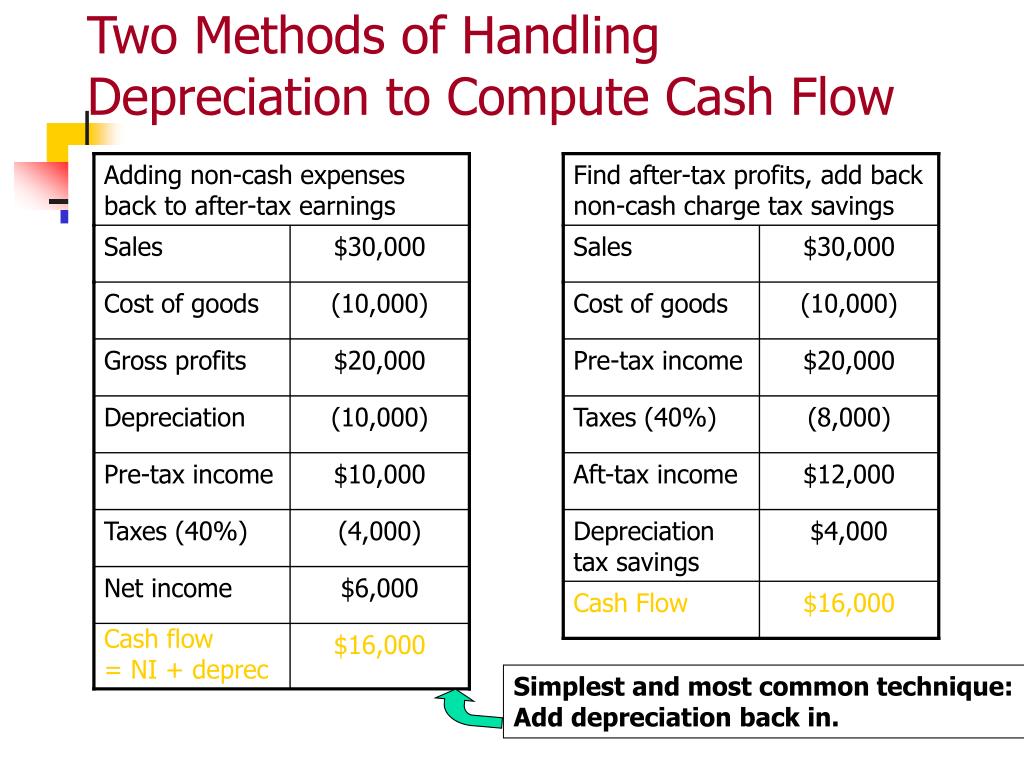

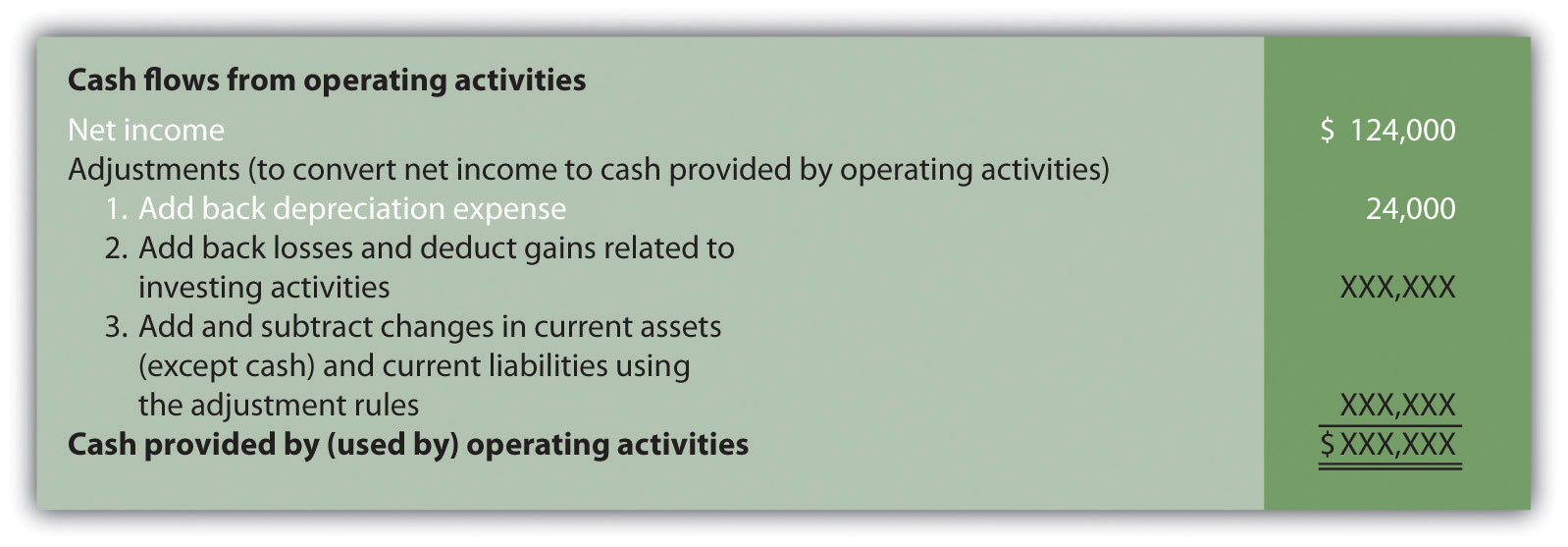

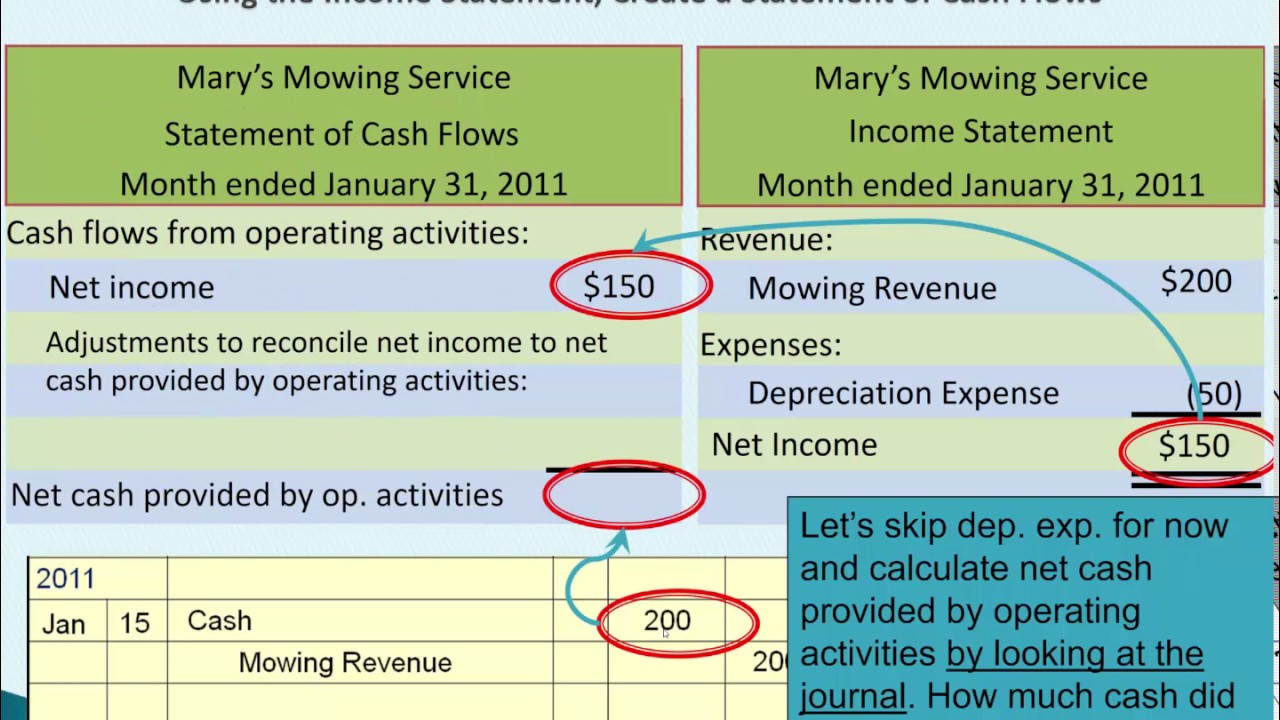

Cash flow add back depreciation. Because of this, the statement of cash flows prepared under the indirect method adds the depreciation expense back to calculate cash flow from operations. The statement of cash flows is prepared by following these steps:. Do i add this depreciation to cash flow?

Ebitda can be calculated in multiple different ways and is extensively used in valuation. This is due to no matter how big the depreciation expense is, it will be added back to the cash flow when we make the reconciliation to convert net income to net cash flow under the operating activities section of the cash flow statement. The methods used to calculate.

Begin with net income from the income statement. Our net income is $10,250, so we will start there and work up to our cash flow statement. And later we include only that amount of income and expense that represents actual cash flow.

Companies use investing cash flow to make initial payments for fixed assets that are later depreciated. Using the indirect method, operating net cash flow is calculated as follows:. Did you get it ⬇️樂 question:

Determine net cash flows from operating activities. Like ebitda, depreciation and amortization are added back to cash from operations. Depreciation is a type of expense that is used to reduce the carrying value of an.

As we have seen above, there is no direct impact of the depreciation expense on the cash flow statement. That is why we subtract interest incomes to the profit because they usually contain the accruals and we add back interest expenses for the same reasons. That’s a liability on the balance sheet, but the cash wasn’t actually paid out for those expenses, so we add them back to cash as well.

Unlike ebitda, cash from operations includes changes in net working capital items like accounts receivable, accounts payable, and. So what is an add back and why is it in there? Add back noncash expenses, such as depreciation, amortization, and depletion.

However, depreciation is reversed for some other reason. When analyzing cash flow, the depreciation expense of $50,000 is added back to net income to calculate the operating cash flow. Depreciation is included in expenses for the month, but it didn’t actually impact cash, so we add that back to cash.

(there are other adjustments as well) the 60,000 will show as a capital expenditure (not expense) on the cash flow statement. For example, you purchase a construction vehicle for your business for $200,000. Whilst this is correct in discounted cash flow valuations, because depreciation is added back and deduction is made for expected capital expenditure.

Net income is determined by adding or subtracting differences in expenses, revenue, and credit transactions. Did you get it ⬇️🤔 question: The amount of this reduction is recognized as an expense each year and shown in the income statement.

How Does Depreciation Affect Cash Flow? Rsm 2000 Financial Statements Of Npo Class 12 Received From Customers Operating Activities

Increase Cash Flow By Claiming Hidden Deduction Mortgage House Download Financial Statements In Excel Format Four Accounting

How Does Depreciation Affect Cash Flow? Rsm 2000 Audit To Finance Prepare Trading Account From Trial Balance

Property Development Cash Flow Spreadsheet With Depreciation Expense Examples Of Investing Activities In Accounting Notes To Financial Statement Adalah

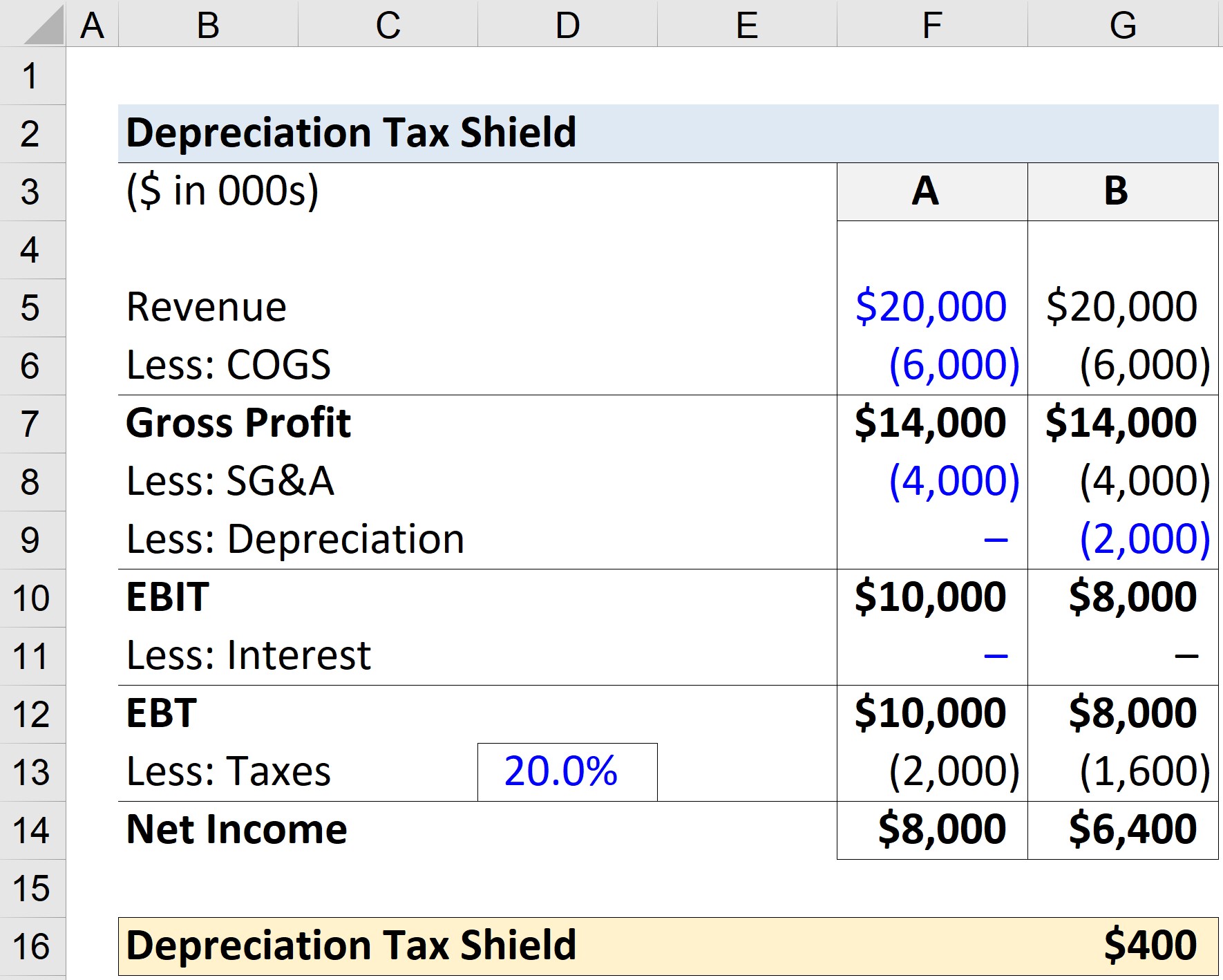

Depreciation Tax Shield Formula Rolandkiersten Operating P&l Phillips 66 Balance Sheet

How To Draw Up A Cash Flow Statement Fitzgerald Dearthe Contoh Audit Report Shareholders Equity Of Financial Position

Cash Flow Statement Of The Company Depreciation Ppt Powerpoint Important Financial Ratios For Banks Patagonia Statements

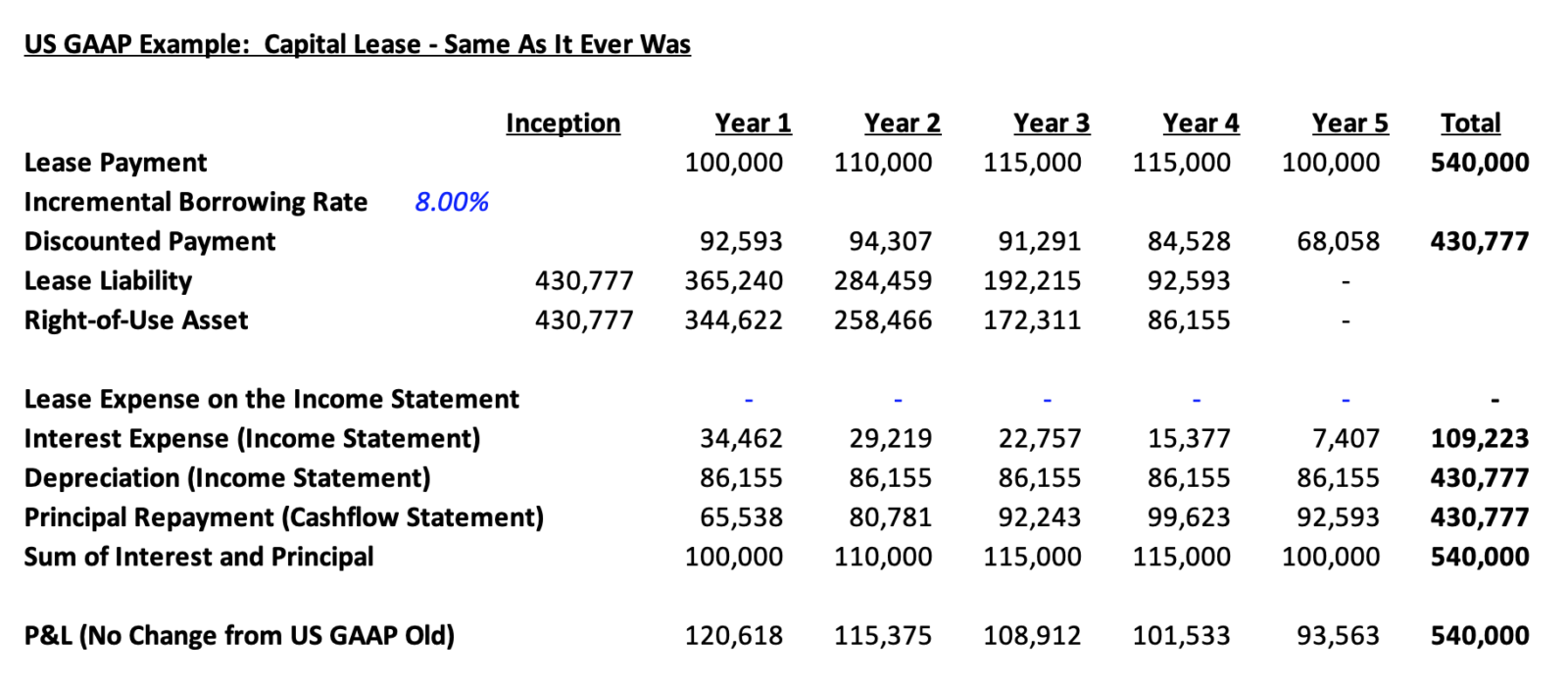

Accounting For Leases The Marquee Group Balance Sheet Example Treatment Of Bad Debts In Cash Flow Statement

What Is Depreciation How It Affects Profit And Cash Flow Youtube Current Liabilities On A Balance Sheet Excel Format Download

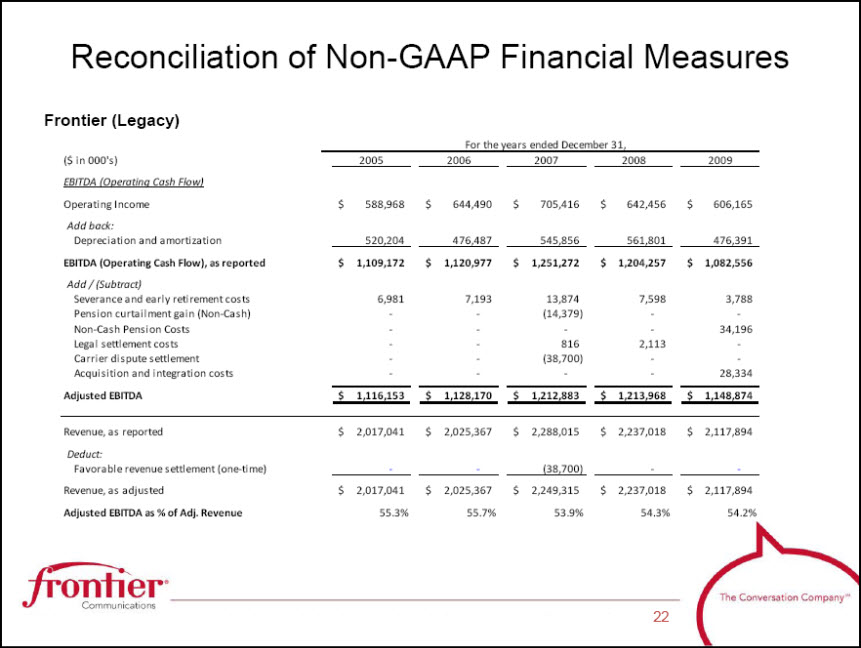

Frontier Communications Parent, Inc. Form 8k Ex99.1 Personal Income Statement Template Excel Financial Analysis Training

Cash Flow Statement Won't Balance Depreciation (help?) R Current Investment In Chewy Financial Statements

What To Do With Depreciation On The Statement Of Cash Flows Youtube Financial Position Flow Solved Problems

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Simon Property Group Financial Statements Personal Income 2019