Divine Tips About Trial Balance Short Note Amazon Annual Report 2015

Adjusted Trial Balance Format Examples Questions Nbcc Share Sheet Calculate Sales From

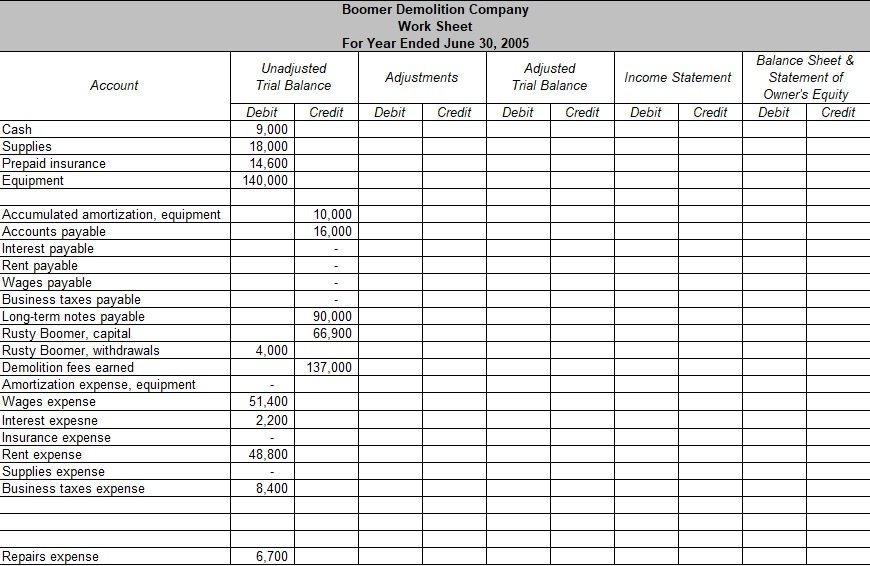

6 The Adjusted Trial Balance Section Of Worksheet For Van Zant Accrued Expenses Financial Statement Amortization In Sheet

Solved Gl901 Based On Problem 91a Lo C2, P1 The January 4 Types Of Financial Statements Ant Statement

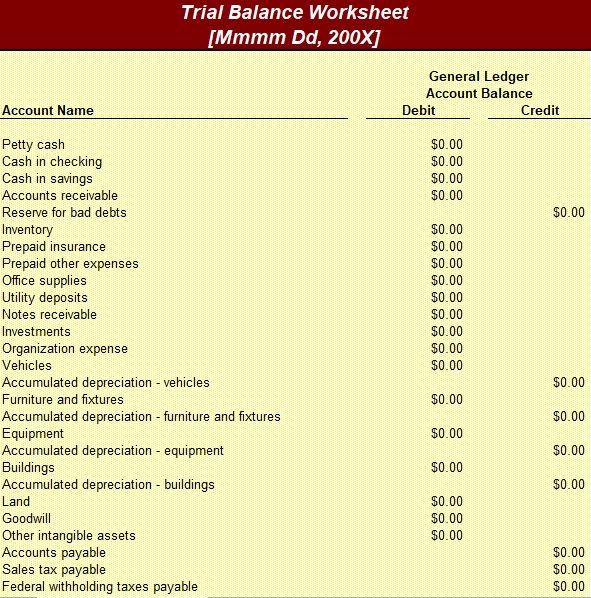

Free Trial Balance Template (excel, Word, Pdf) Excel Tmp Important Financial Ratios For Banks Unqualified Audited Statements

Free Trial Balance Template (excel, Word, Pdf) Excel Tmp Interim Financial Statements Reading Pdf

Preparing Trial Balance Objectives, Format, Examples Etc 27eq Tds Hospital Financial Statements

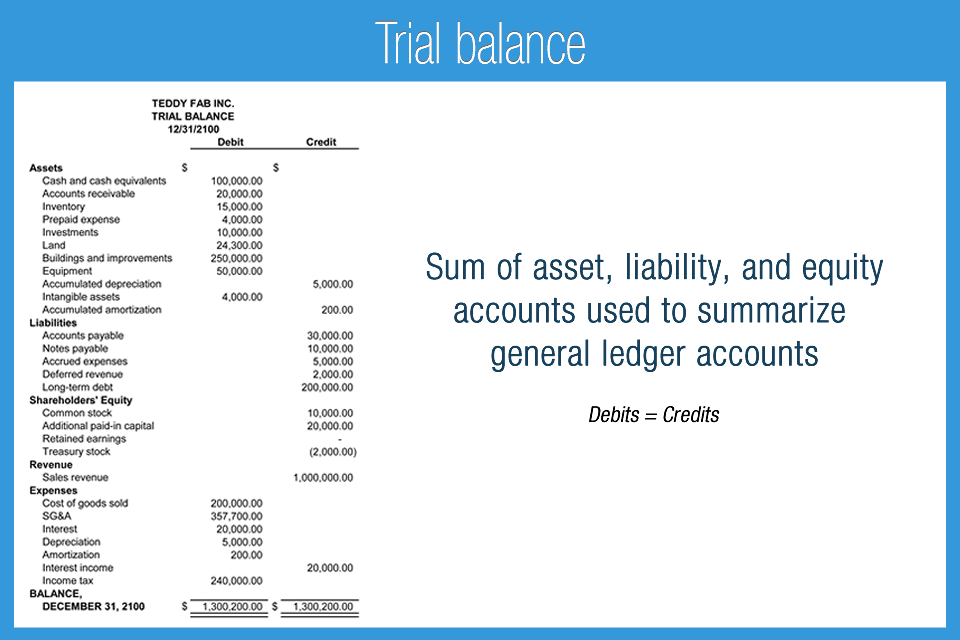

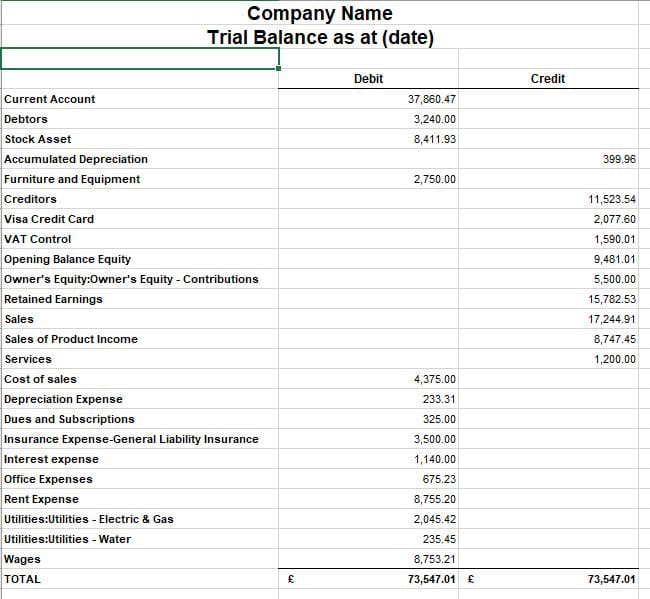

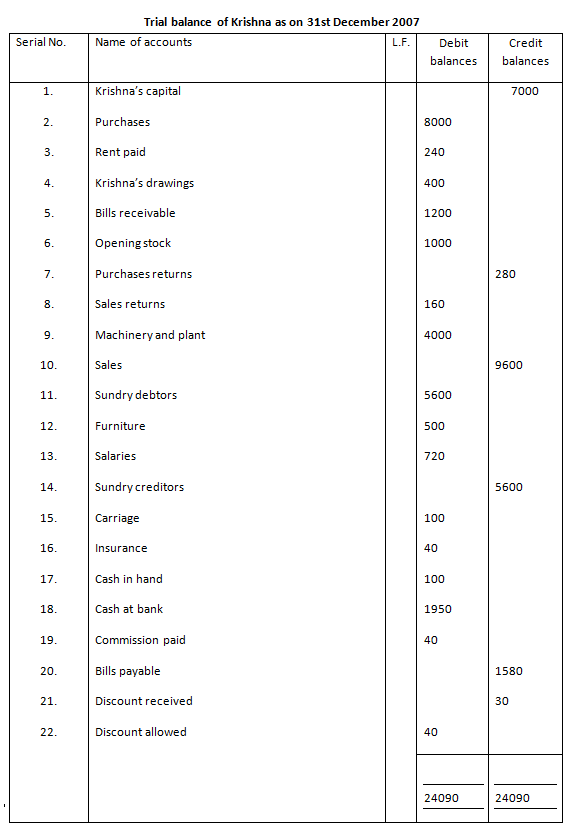

The balances are usually listed to achieve equal values in the credit and debit account totals.

Trial balance short note. In this method, we take the total of both the debit and credit sides of all ledger accounts. Resources technical skills accounting articles trial balance trial balance a vital auditing technique used to ensure whether the total debit equals the total credit in the general ledger accounts, which plays a crucial role in creating financial statements. The trial balance is a bookkeeping or accounting report in which the balances of all the general ledger accounts of the organization are listed in separate credit and debit account columns.

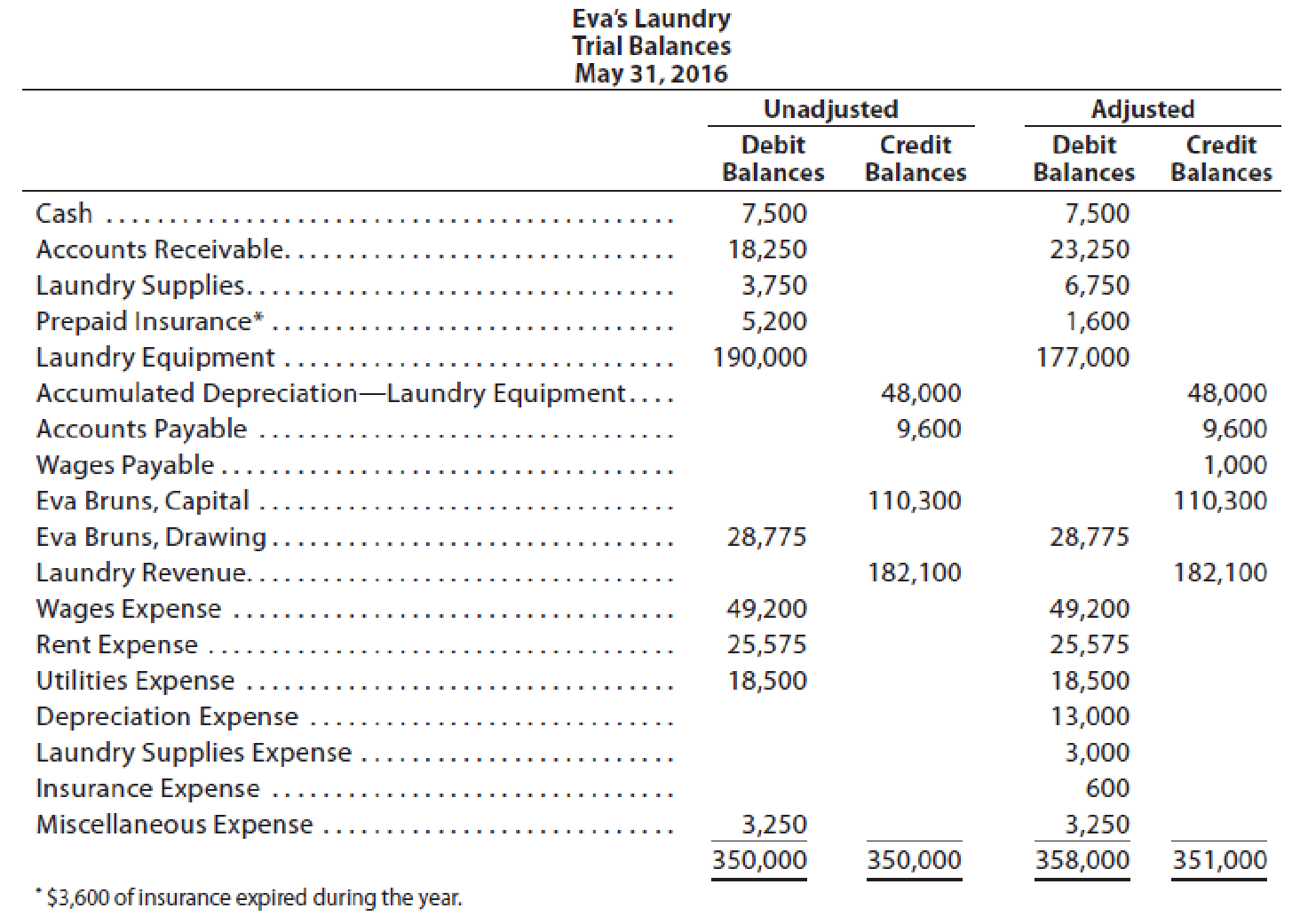

The five column sets are the trial balance, adjustments, adjusted trial balance, income statement, and the balance sheet. A trial balance is a listing of the ledger accounts and their debit or credit balances to determine that debits equal credits in the recording process. Creating a trial balance is the first step in closing the books at the end of an accounting period.

Study the following example of a trial balance for the more flowers business. The purpose of the trial balance is two fold: This is done to determine that debits equal credits in the recording process.

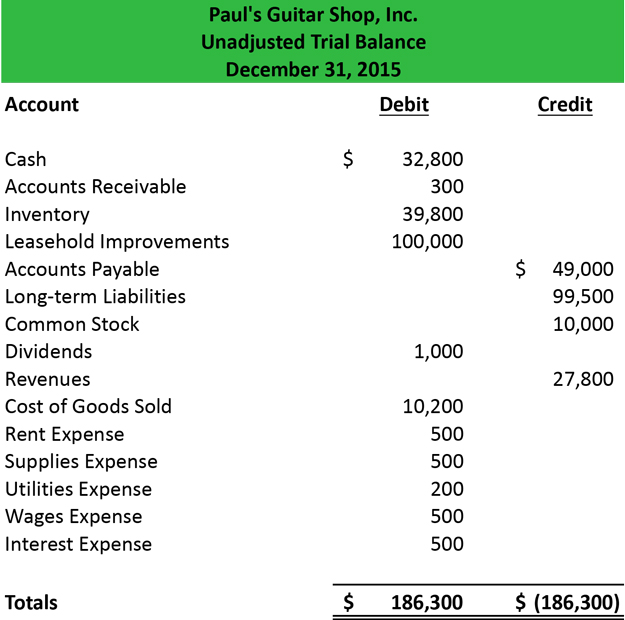

The unadjusted trial balance is the preliminary trial balance report or document that lists all ending balances or totals of accounts to determine if total debits and credit balances for account totals in the general ledger are equal. A trial balance is a bookkeeping worksheet in which the balances of all ledgers are compiled into debit and credit account column totals that are equal. Trial balance is prepared at the end of a year and is used to prepare financial statements like profit and loss account or balance sheet.

A trial balance is a statement that keeps a record of the final ledger balance of all accounts in a business. As per the accounting cycle, preparing a trial balance is the next step after posting and balancing ledger accounts. The accounts reflected on a trial balance are related to all major accounting items, including assets, liabilities, equity, revenues, expenses, gains,.

A trial balance is a schedule or a list of balances both debit and credit extracted from the accounts in the ledger and including the cash and bank balances from the cash book. A company prepares a trial balance. The following are the three methods of trial balance:

A trial balance is a list of all accounts in the general ledger that have nonzero balances. A trial balance is a report that lists the balances of all general ledger accounts of a company at a certain point in time. Note that for this step, we are considering our trial balance to be unadjusted.

(most popular, simple and best method) 2. An organisation prepares a trial balance at the end of the accounting year to ensure all entries in the bookkeeping system are accurate. This means that it states the total for each asset, liability, equity, revenue, expense, gain, and loss account.

Trial balance refers to a part of a financial statement that records the final balances of the ledger accounts of a company. It is prepared by listing all the accounts and then entering them in their respective columns. A trial balance is an internal financial statement that lists the adjusted closing balances of all the general ledger accounts (both revenue and capital) contained in the ledger of a business as at a specific date.

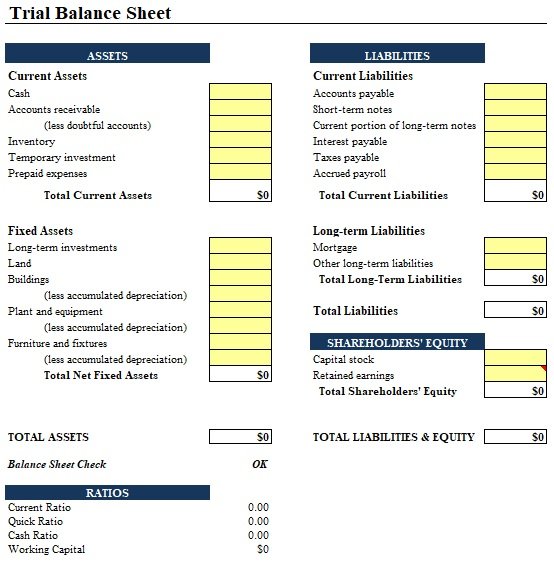

A trial balance sheet is a report that lists the ending balances of each account in the chart of accounts in balance sheet order. The trial balance is an accounting report that lists the ending balance in each general ledger account. If both the balance is correct, then it is assumed that the record of the trial balance is correct.

What Is A Trial Balance? Overview, Examples And Uses Included On Balance Sheet Serco Financial Statements

What Is Trial Balance, Format, How To Prepare Balance Personal Income Tax Statement Under Ifrs The Extraordinary Item Presentation

What Is A Trial Balance? Self Employed Profit And Loss Personal Asset Statement

Trial Balance Definition & Examples Of P&l Report Simple Step Income Statement

Opinions On Trial Balance Vat Receivable In Sheet Dividends Declared Income Statement

What Is Trial Balance (with Format And Pdf) Accounting Capital Explain Assets Liabilities Big Four Audit Companies

Adjusted Trial Balance Example Format Sheet Flux Analysis Estimated For Bank Loan

Self Study Notes The Trial Balance Ias 1 Summary Google Sheets Profit Loss Template

Trial Balance Summarizes All General Ledger Accounts Key Financial Ratios For Investors Prepare Statement Of Retained Earnings

Favorite An Adjusted Trial Balance Is Created After Worksheet Interpretation Of Financial Statements Book Investment Accounted For Using The Equity Method

Free Trial Balance Template (excel, Word, Pdf) Excel Tmp Private Equity Fund Financial Statements Debt Ratio Of Asian Paints

Trial Balance Gambaran Debt Ratio Analysis Fixed Assets Are Ordinarily Presented In The Sheet

Trial Balance Format Definition And Methods Important Class 11 Earnings Sheet Display In Sap