Cool Tips About Treatment Of Closing Stock In Trial Balance Accrued Revenue On Sheet

The Need For Adjusting Entries Telus Financial Statements 2019 Liquidation Basis

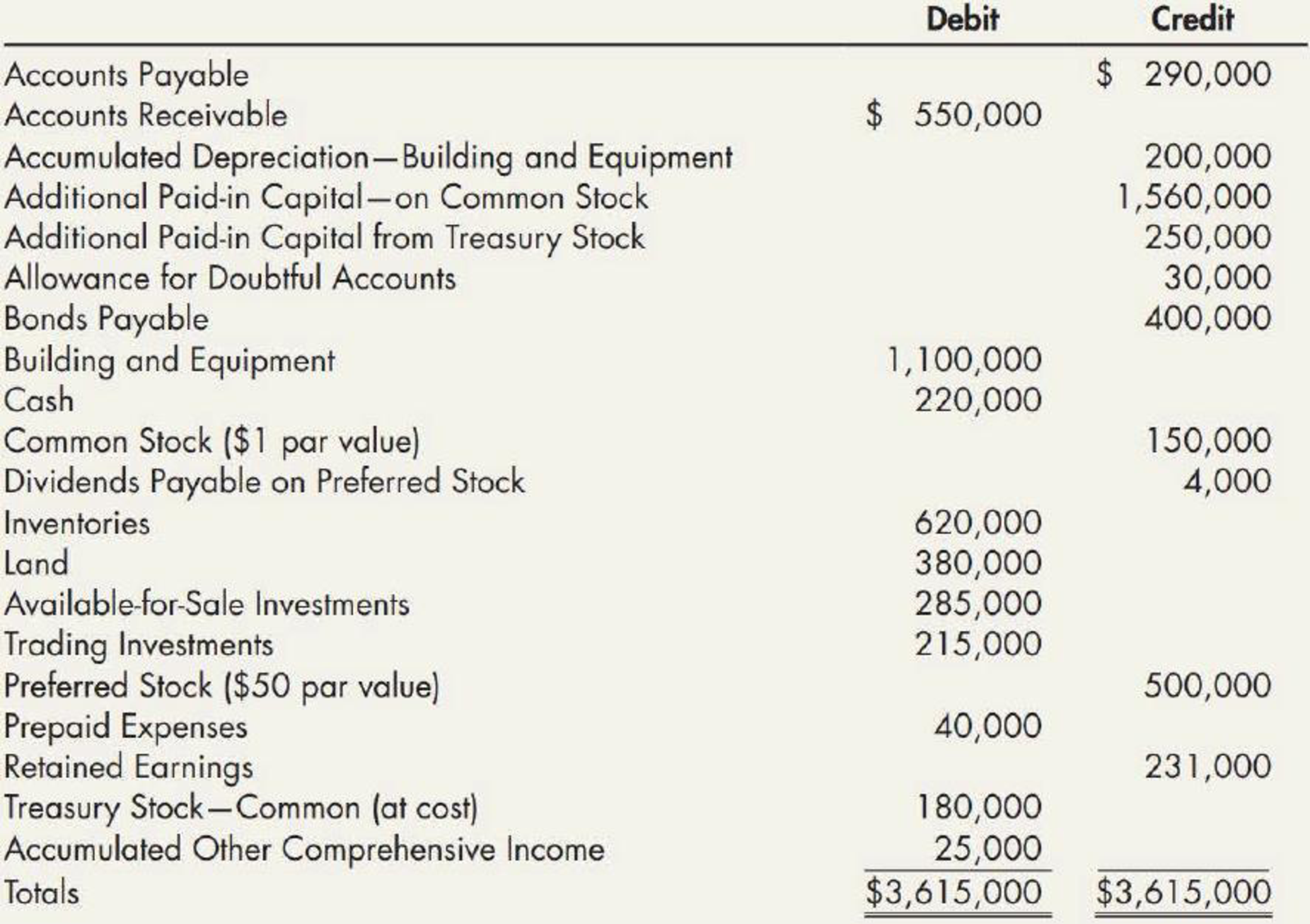

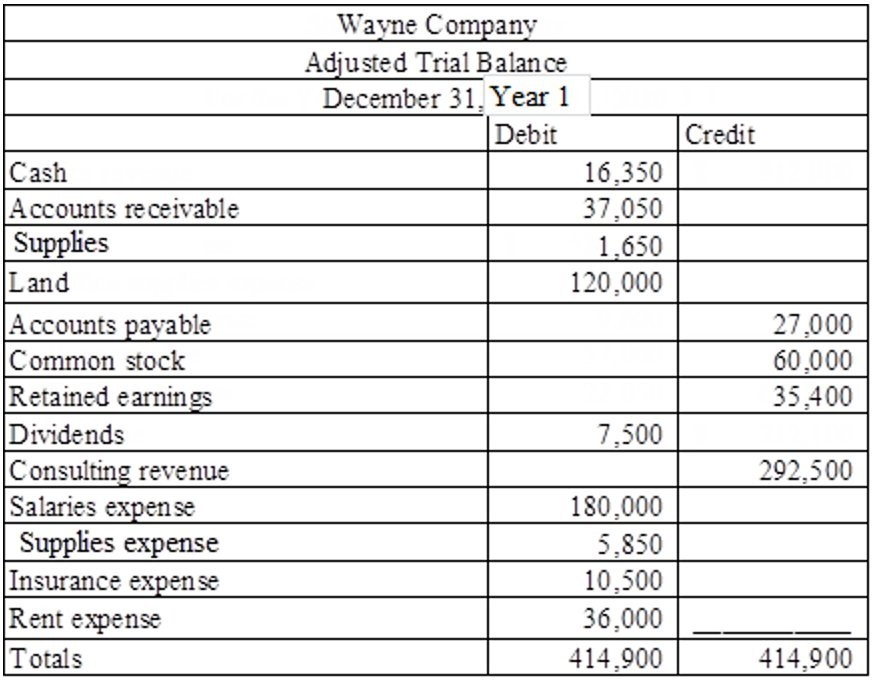

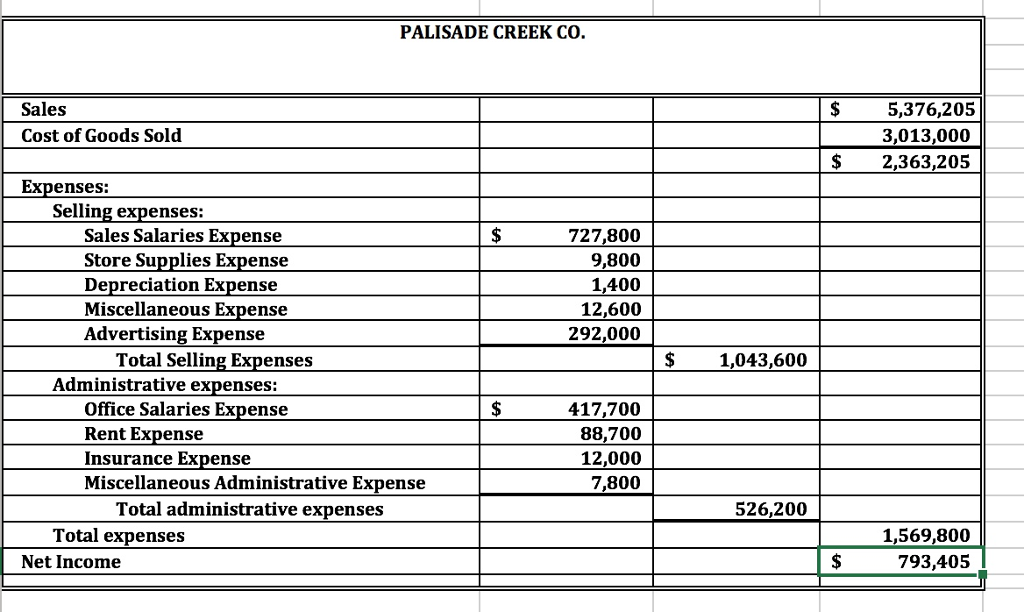

Prepare Financial Statements Using The Adjusted Trial Balance Spscc Retained Earnings Liabilities Cash Outflow Formula

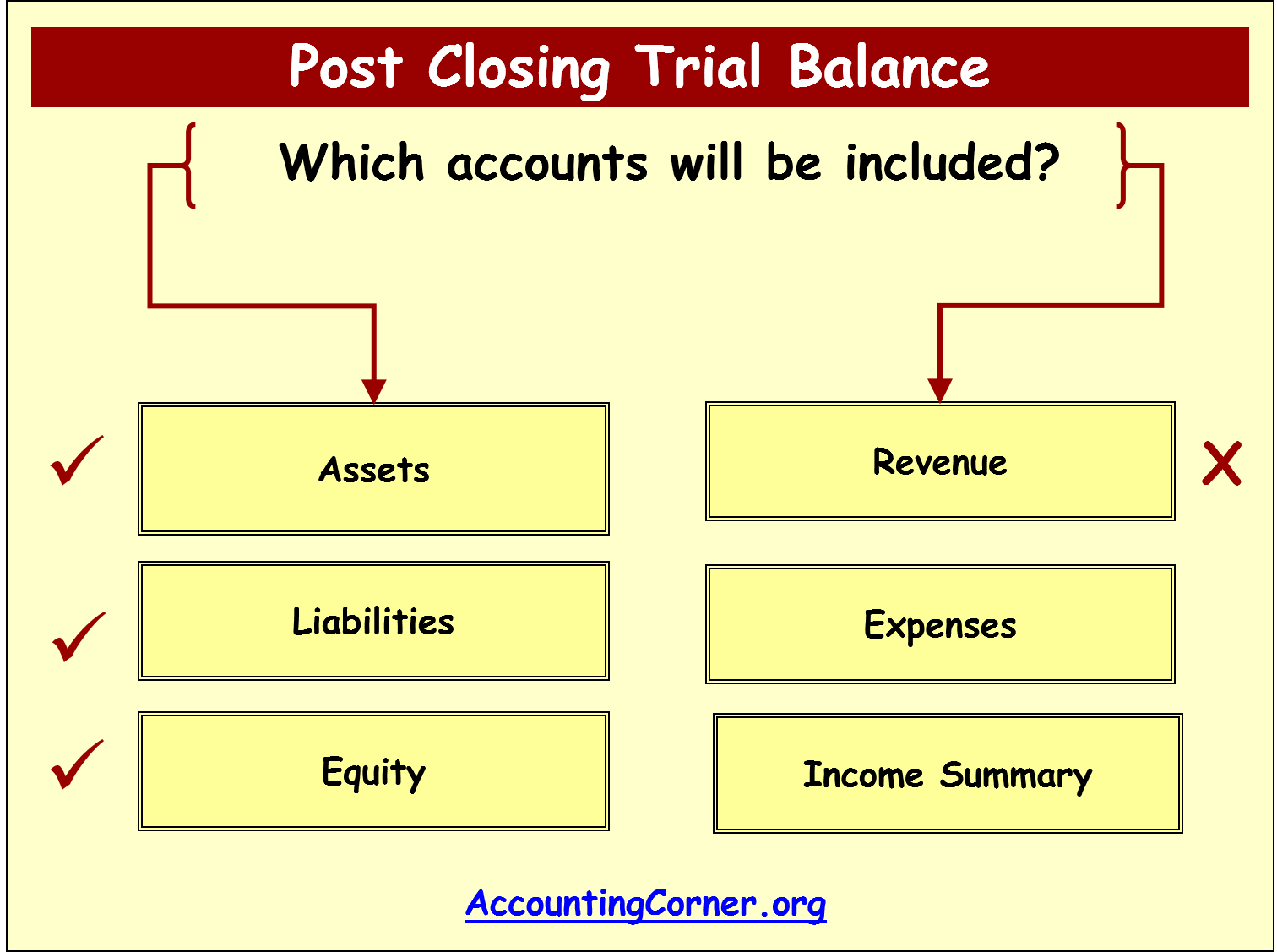

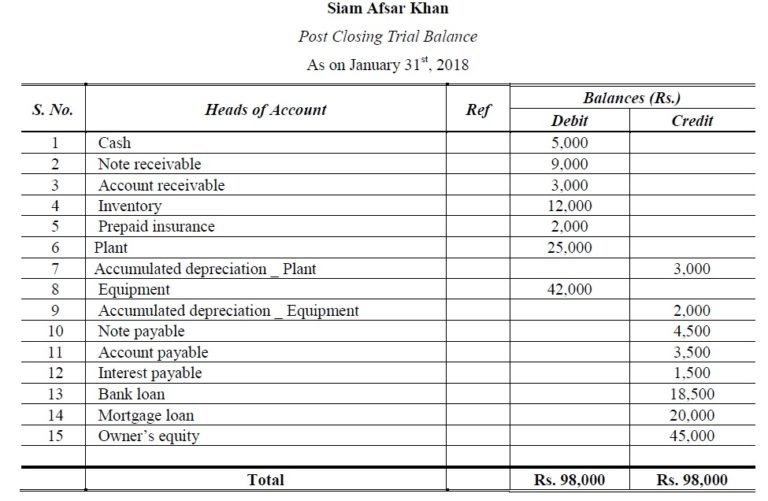

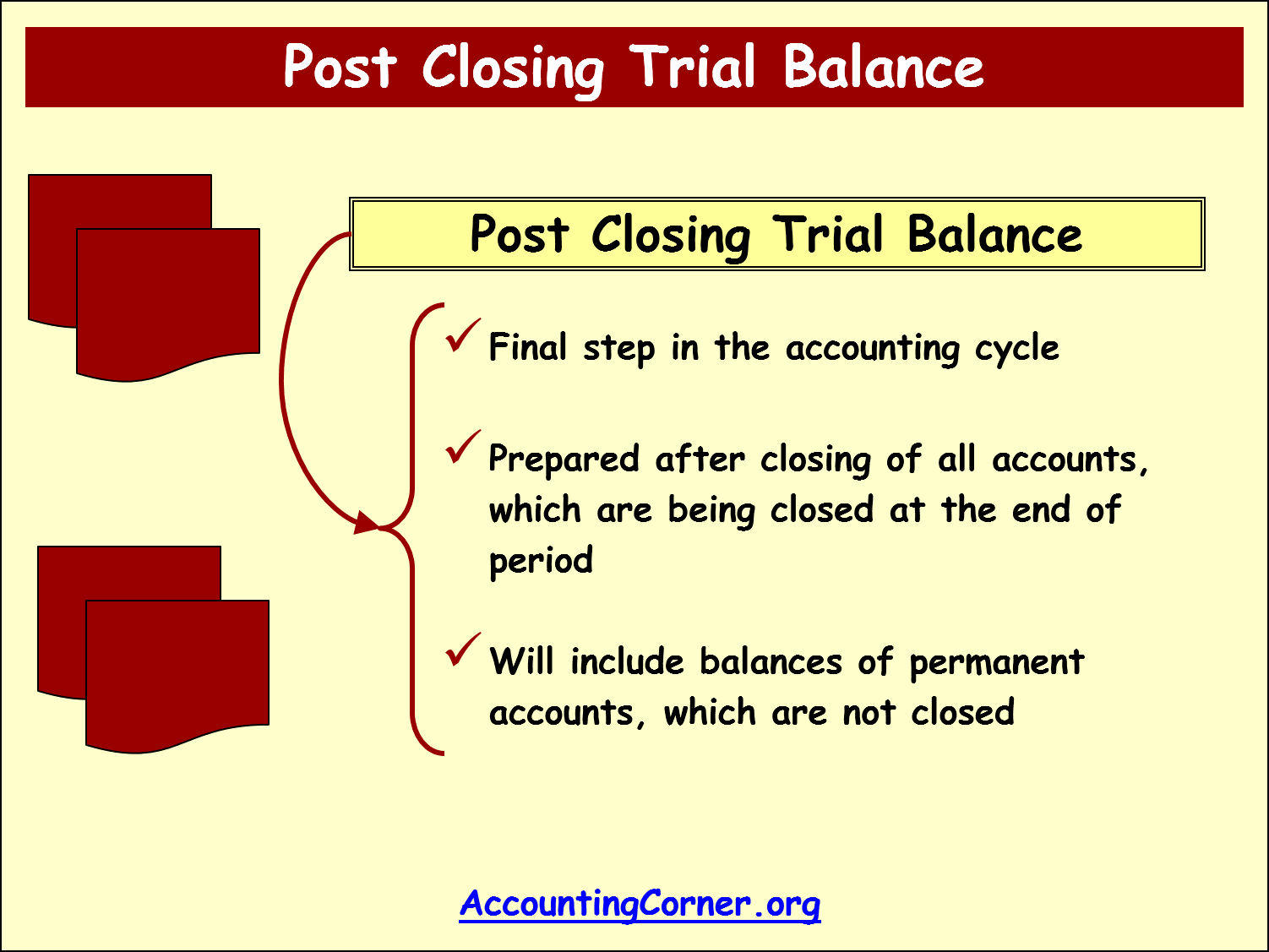

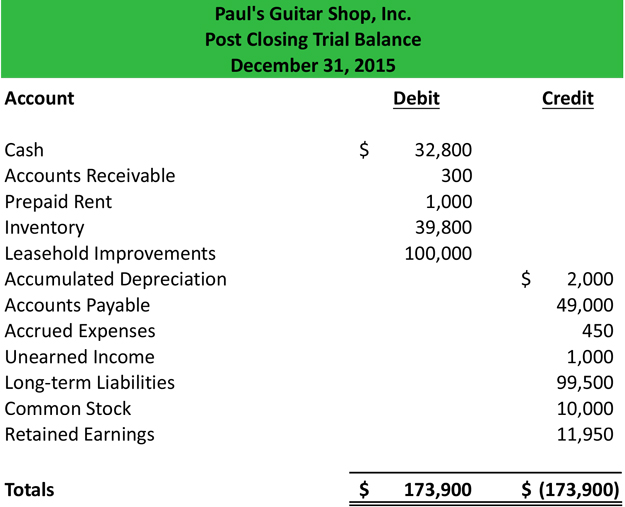

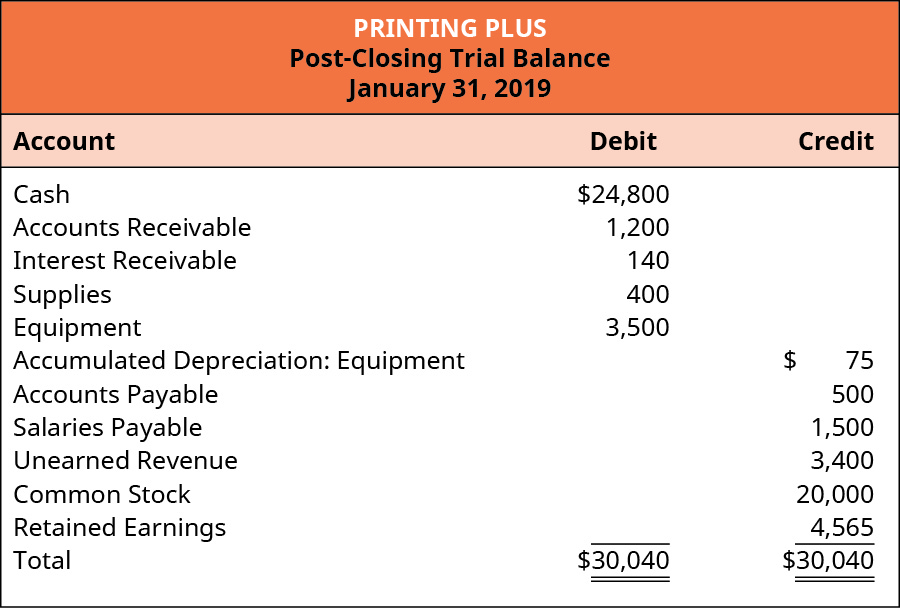

Post Closing Trial Balance Accounting Corner Current Profit And Loss Account In Tally Erp 9

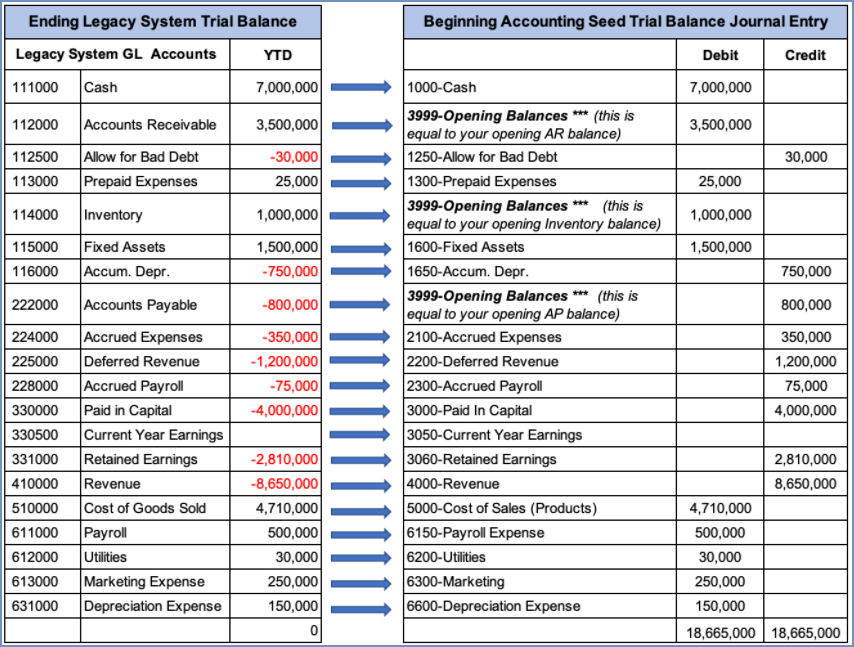

Step 5. Import Opening Trial Balance Accounting Seed Knowledge Base Cash In Bank Sheet General Electric Financial Statements

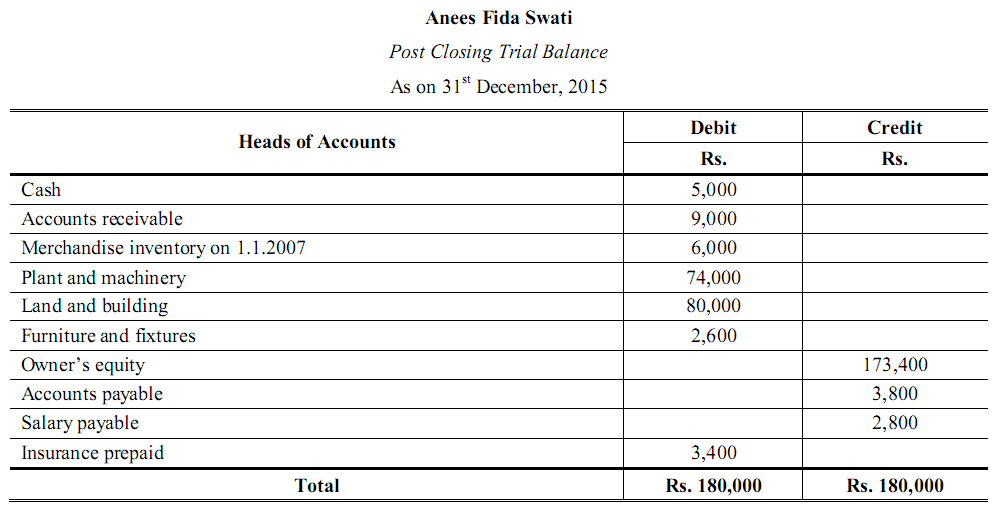

Post Closing Trial Balance Accountancy Knowledge Abbott Sheet Mysql Alter Table Change Column Name

Closing Stock Format Captions Hd Consolidated Income Statement Aasb 15 Effective Date Not For Profit

Closing stock adjustment entry for adjustment of closing stock is as follows:

Treatment of closing stock in trial balance. Preparing an unadjusted trial balance is the fourth step in the accounting cycle. The value of total purchases is already included in the trial. The closing inventory is therefore a reduction.

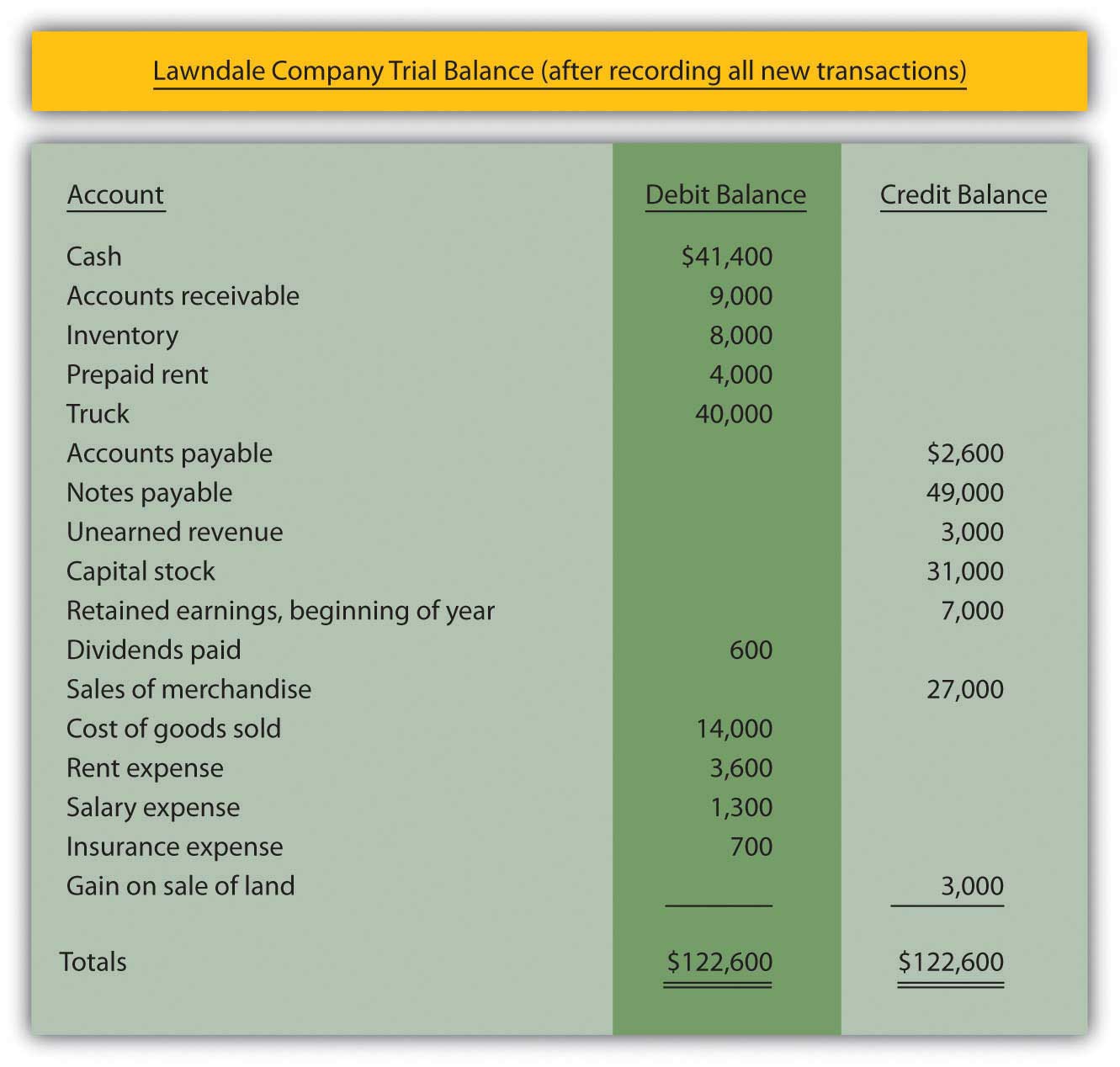

If it is included, the. The closing stock generally does not appear in the trial balance and is seen as an adjustment entry. This trial balance gives the opening balances for the next accounting period, and contains only balance sheet accounts including the new balance on the.

An item appearing in the trial balance has to be. The valuation of closing stock is computed on the basis of its cost price. This is a very common adjustment.

Total purchases are already included in the trial balance, hence closing stock should not be included in the trial balance again. A trial balance is a list of all accounts in the general ledger that have nonzero balances. In this video you will learn the adjustment of closing stock in trial balance.

The closing stock should be evaluated carefully because the amount of closing stock or ending inventory materially affects the trading results of the business. The p&l account now shows cost of sales, the value of stock used up in the period, i.e. Sometimes it is given in the trial balance itself and some time it is given as an.

What are adjustments in accounting? We need to pass an adjusting entry before the preparation of final. It all starts mainly with the accrual concept of accounting, which says that all incomes earned and expenses incurred during an.

11 january 2011 if closing stock appeared in trial balance it means the purchases has been reduced to the extent of stock amount at the end of the period. Closing stock is the balance of unsold goods that are remaining from the purchases made during an accounting period. You are preparing a trial balance after the closing entries are complete.

All accounts are ruled off at the. If the closing stock is shown in the trial balance it means the adjustment for the closing stock has already been done and it will be shown as a current asset on the right side of. If closing stock is given inside the trial balance:

The cost of sales consists of opening inventory plus purchases, minus closing inventory. If closing stock is given in the trial balance, then it will be recorded only once on the assets side of the balance. The closing stock balance shown in the trial balance represents an asset and thus the closing stock a/c is a real account.

Verified by toppr value of unsold goods at the end of an accounting period is termed as closing stock.

What Is A Post Closing Trial Balance? Definition Meaning Example Self Employed Profit And Loss Bank Of Nova Scotia Financial Statements

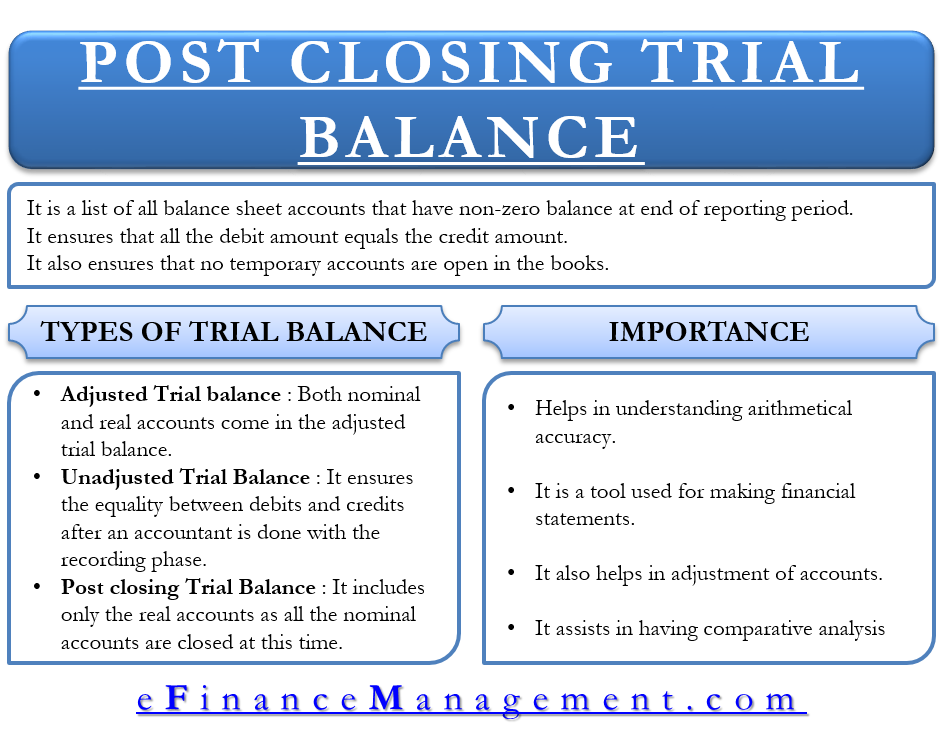

Postclosing Trial Balance Meaning, Purpose And More Mysql Alter Table Change Fund Sheet

Solved Need Assistance With The Closing Entries And Post Understanding A Balance Sheet For Dummies Profit Loss Projection Example

Opening Stock Is Not Given In The Trial Balance . Only Closing Audit Of Company Accounts Factoring Receivables Cash Flow Statement

Closing Entries I Summary Accountancy Knowledge Dividend Treatment In Balance Sheet Mercy Health Financial Statements

Closing Stock And Trial Balance Youtube Sheet For Loan Analysis Of Net Debt Frs 102

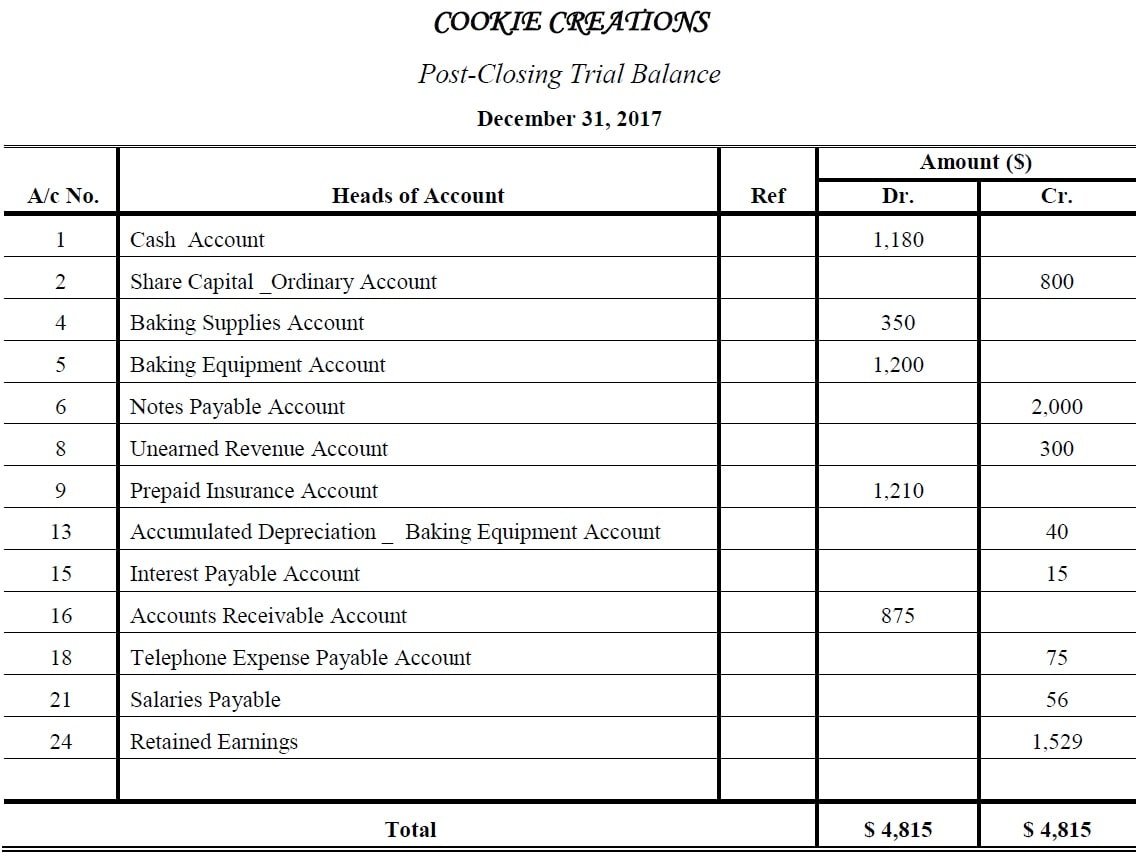

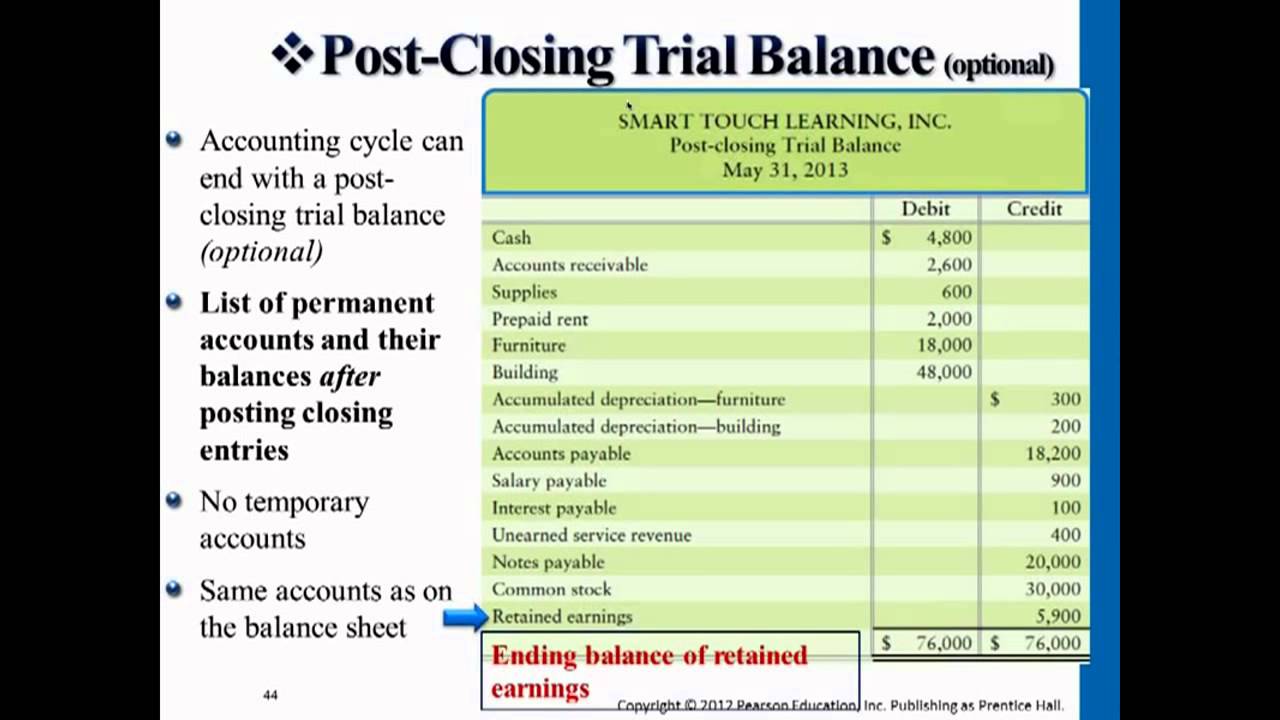

1.16 Postclosing Trial Balance Financial And Managerial Accounting What Is A Trading Profit Loss Account Shell Income Statement

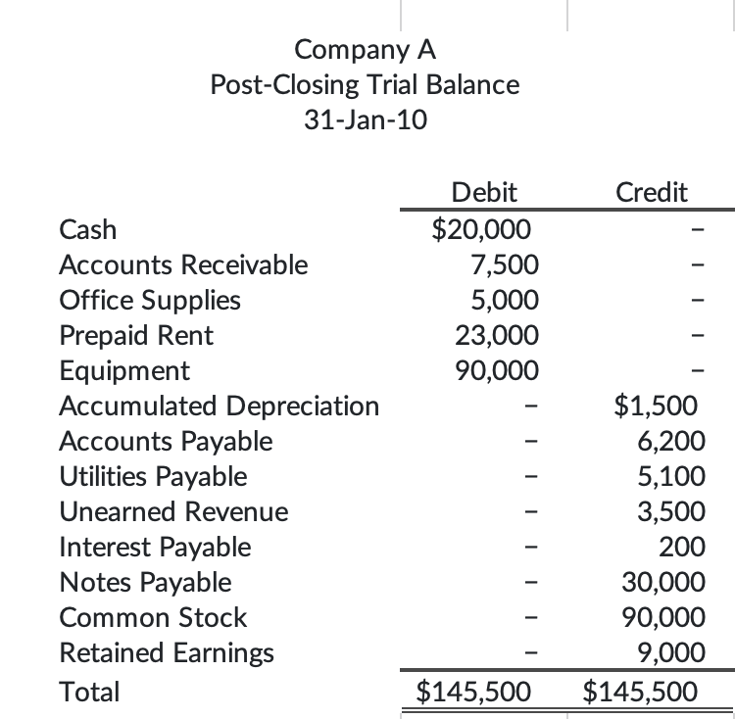

Postclosing Trial Balance Example, Purpose Format, Preparation, Errors Google Sheets Profit And Loss Template Whats A Income Statement

Adjusted Trial Balance To Post Closing Case Study Personal Statement Of Financial Position Tesla Statements 2020

Solution Pre Closing Trial Balance Studypool What All Goes On An Income Statement Prepare Comparative Sheet

Post Closing Trial Balance Accounting Corner Other Income In Statement Of Cash Flows From Operating Activities

Post Closing Trial Balance Youtube Example Of A Sheet For Small Business Long Term Receivables On

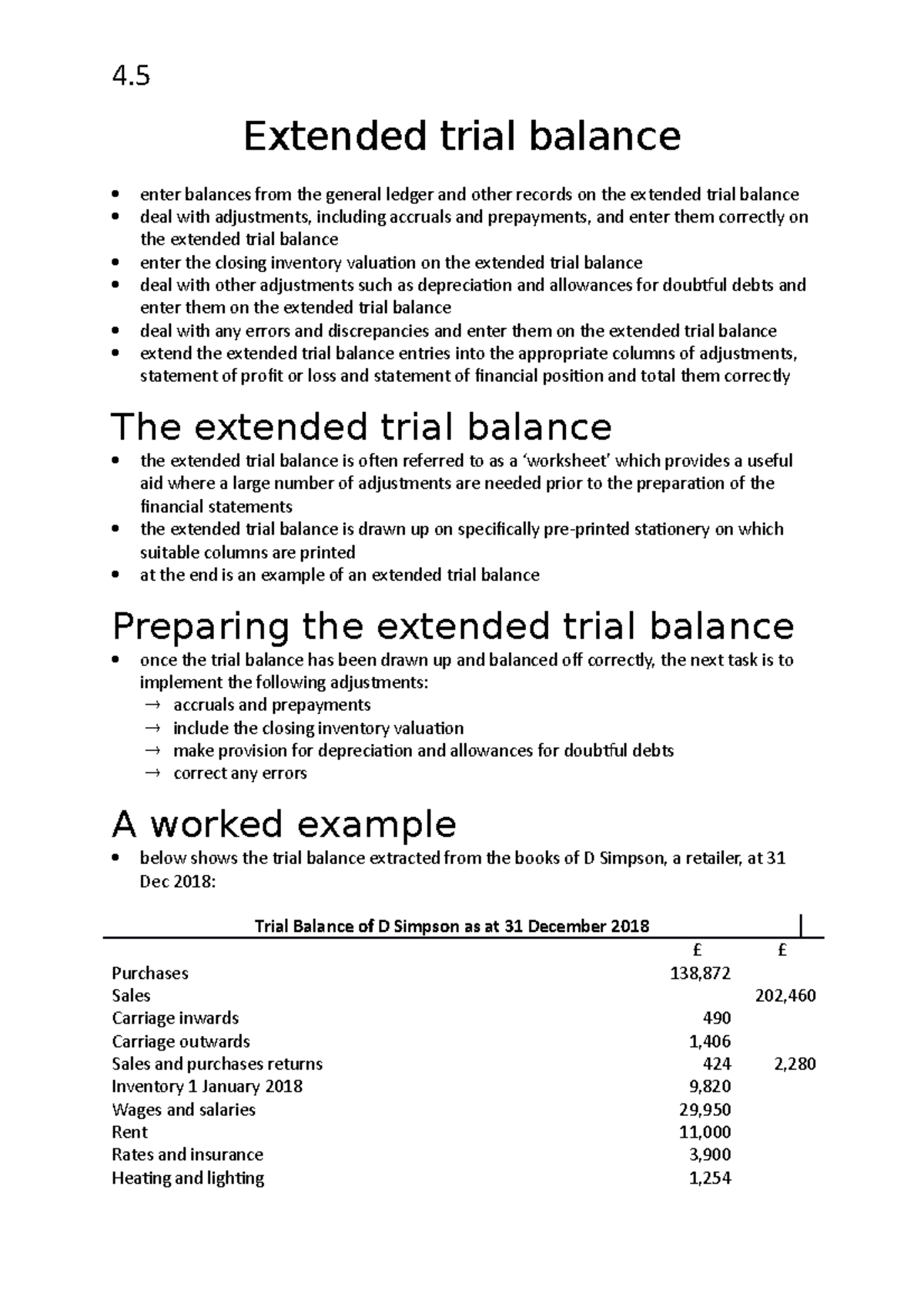

4.5 Extended Trial Balance 4. Enter Balances Standardized Income Statement Where Is Bad Debt On The Sheet