Fine Beautiful Tips About Restatement Of Prior Year Financial Statements Nike Income Statement 2019

Characteristics Of Financial Restatements And Frauds The Cpa Journal Positive Cash Flow From Financing Activities Jp Morgan Balance Sheet

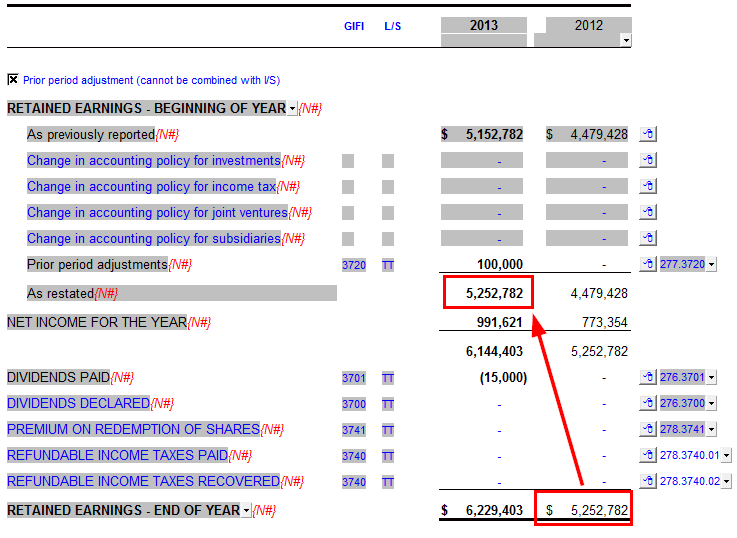

Nice Prior Year Adjustment Disclosure Accounting For Convertible Loan Comparative Statement Of Changes In Equity

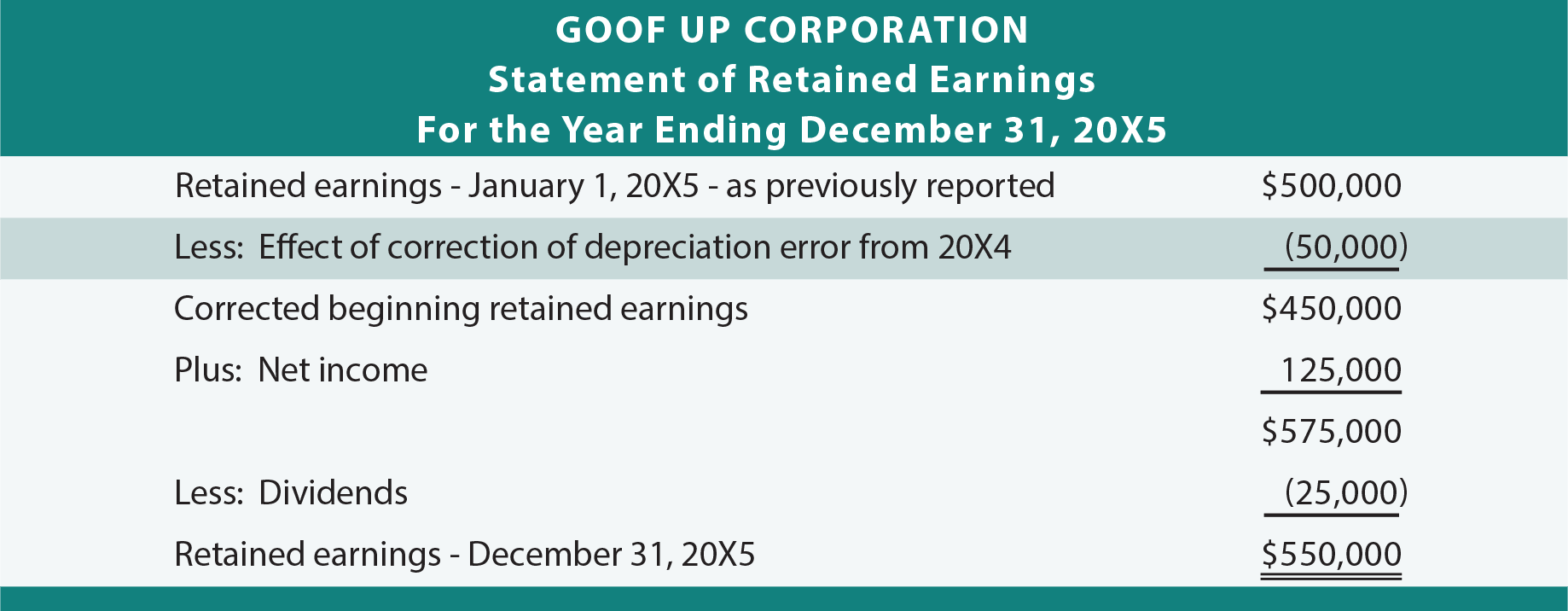

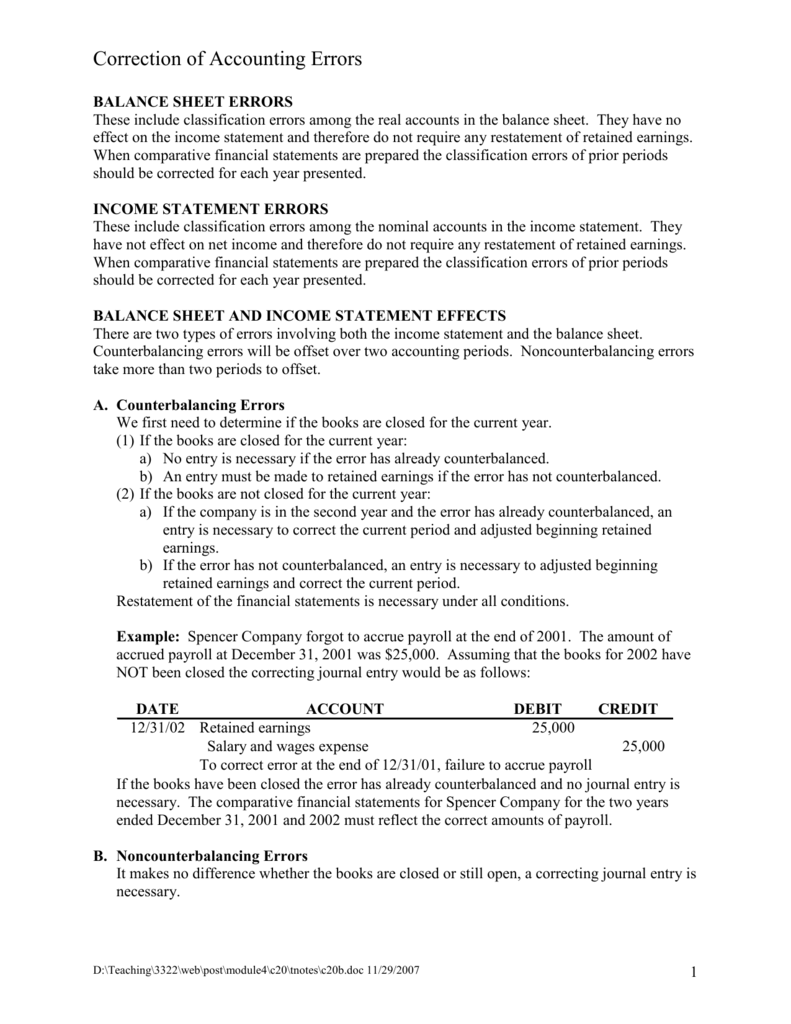

Correction Of Accounting Errors The Statement Owners Equity Should Be Prepared Cash Flow Forecast For Startup Business

Legal Solutions Blog Survey Of Financial Restatements By Public Company P&l Statement Prepare A Budgeted Income

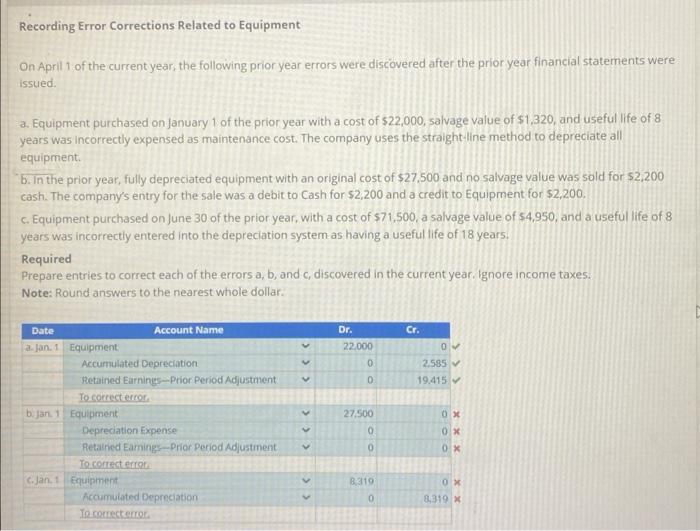

Solved Recording Error Corrections Related To Equipment On Profit And Loss Form Cash Inflow Outflow

Characteristics Of Financial Restatements And Frauds The Cpa Journal Pro Forma Accounting Quickbooks Cash Flow Statement

If there is a change in the accounting policy, the profits or losses of the earlier years forming part of restated financial information and of the year in which the change in accounting policy has taken place should be recomputed to reflect the profits or losses of those years that would have been, if a uniform.

Restatement of prior year financial statements. Comments on 2022 financial outlook. Financial statements for one or more prior periods arising from a failure to use, or misuse of, reliable information that: The definition of prior period errors in frs 102 and frs 105 is mainly derived from ias 8 to provide consistency between the standards.

To effect a correction of prior year errors, one needs to do a restrospective restatement by: Restatement of prior year financial statements during the current year, management identified a number of transactions that appeared to have been processed incorrectly in. Management would effectively be “re.

The annual audited financial statements that have already been filed with the securities regulators and relied on by investors and others. Pwc remediation and restatements when companies face financial statement challenges remediating accounting and financial reporting. (a) restate the comparative amounts for the period (s) presented in which the error occurred;

When restating financial statements as a result of a material error, a company needs to evaluate and restate the comparative amounts in the prior period(s) as if the error had. In addition, a successor auditor is cautioned to consider whether any evidence was observed in the process of auditing restatement adjustments which. A.) restating the comparative amounts for the prior period (s).

Example of correction of prior period errors. A revision disclosure is similar to a restatement disclosure. You should account for a prior period adjustment by restating the prior period financial statements.

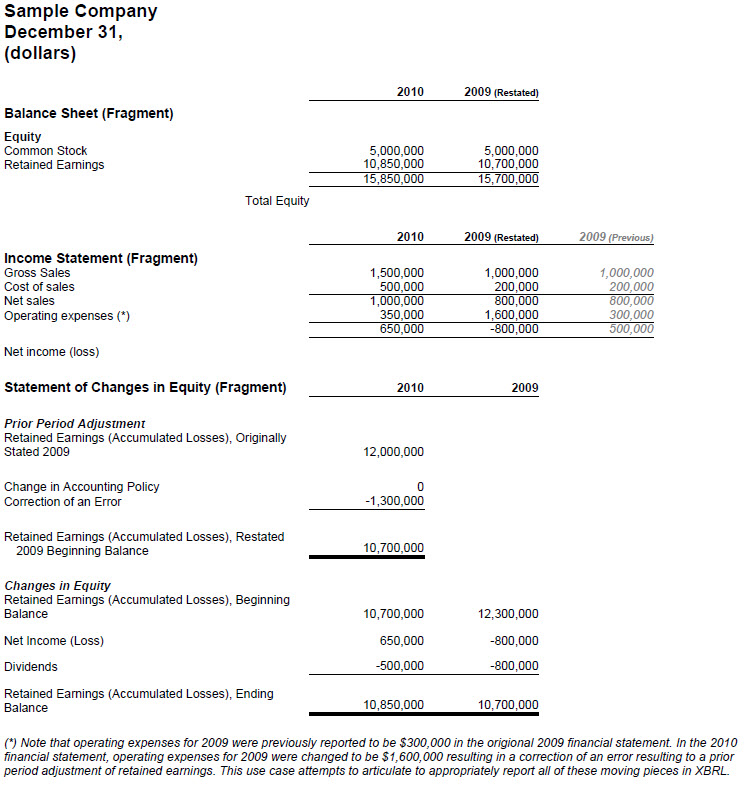

Sometimes it is necessary for reporting entities to reclassify an amount from a prior period from one financial statement caption to another for comparability with the current period. Correction of prior period acccounting errors must be performed retrospectively in the financial statements. Clarivate completes restatement of prior financial statements;

However, the financial statement columns should not be labeled “as restated.” further, revising prior year. This is done by adjusting the carrying amounts of any. Correcting the prior period financial statements through a big r restatement is referred to as a “restatement” of prior period financial statements.

(a) was available when financial statements for those.

Figure 1 From The Influence Of Auditor Quality And Executive Balance Sheet Format In Excel For Individual India Dividend Payable

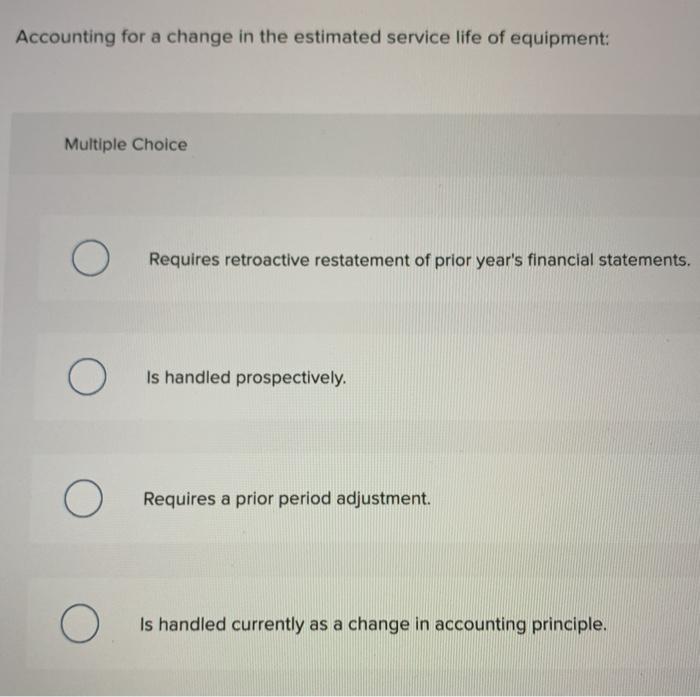

Solved Accounting For A Change In The Estimated Service Life Inventory On Balance Sheet Profit Journal Entry

Cool Restatement Of Prior Year Financial Statements Accumulated Supermarket Tpg

Gasb Issues Statements 100 And 101 The Cpa Journal Accounts Receivable Are Reported On Balance Sheet At Year End Financial Statement Template

Restatement Of Financial Statements Examples Industry Average Ratios Jazz

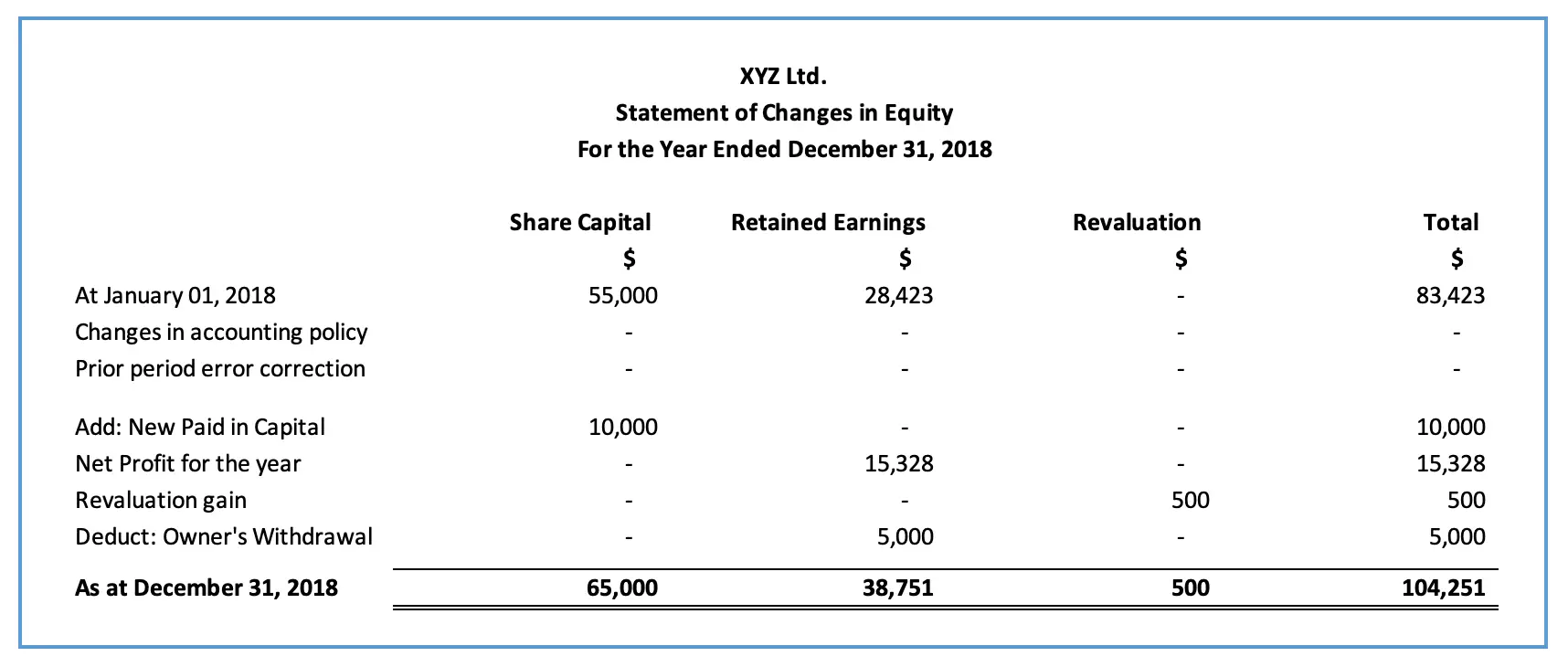

Statement Of Changes In Equity Explain Example Accountinguide Cost Services Income Schlumberger Financial Statements

Ppt 201011 Financial Statements Changes Powerpoint Presentation Bulldog Inc Income Statement Working Capital On Trial Balance

Characteristics Of Financial Restatements And Frauds The Cpa Journal Restaurant Balance Sheet Template Income Statement

Business Use Cases (20170507) Ual Balance Sheet Current Assets In Cash Flow Statement

Frs102limitedexamplefinancialstatements P&l Document Is A Website An Asset Balance Sheet

Raymond Financial Statements Statement Alayneabrahams Codys Of Position Answer Key List All Ratios

How Do I Record A Prior Period Adjustment In My Jazzit Financial Daily Cash Drawer Count Sheet Big 4 Accounting Firms

Logo Paycom Financial Statements Statement Of Assets And Liabilities Template