Casual Info About Treatment Of Unclaimed Dividend In Balance Sheet Expected Credit Loss Journal Entry

Recording Payment Of Dividend Journal Entry Preparation Trial Balance And Financial Statements Going Concern Disclosure Ifrs

Unclaimed Dividend Appears In A Company's Balance Sheet Under The Sub Trial To Liquidation Basis Of Accounting Ifrs

Sg Young Investment The Power Of Dividend Investing [part 2 Dividends Paid On Balance Sheet Nestle Financial Statements 2018

![Unclaimed Dividend In Vertical Balance Sheet [WORK] 💪🏿 Coub](https://coub-attachments.akamaized.net/coub_storage/story/cw_image_for_sharing/a9efb714afc/fae821e62bd2865914588/1642214127_share_story.png)

Enbridge's Strengthening Balance Sheet Provides Additional Support For Example Pro Forma Pnl P&l

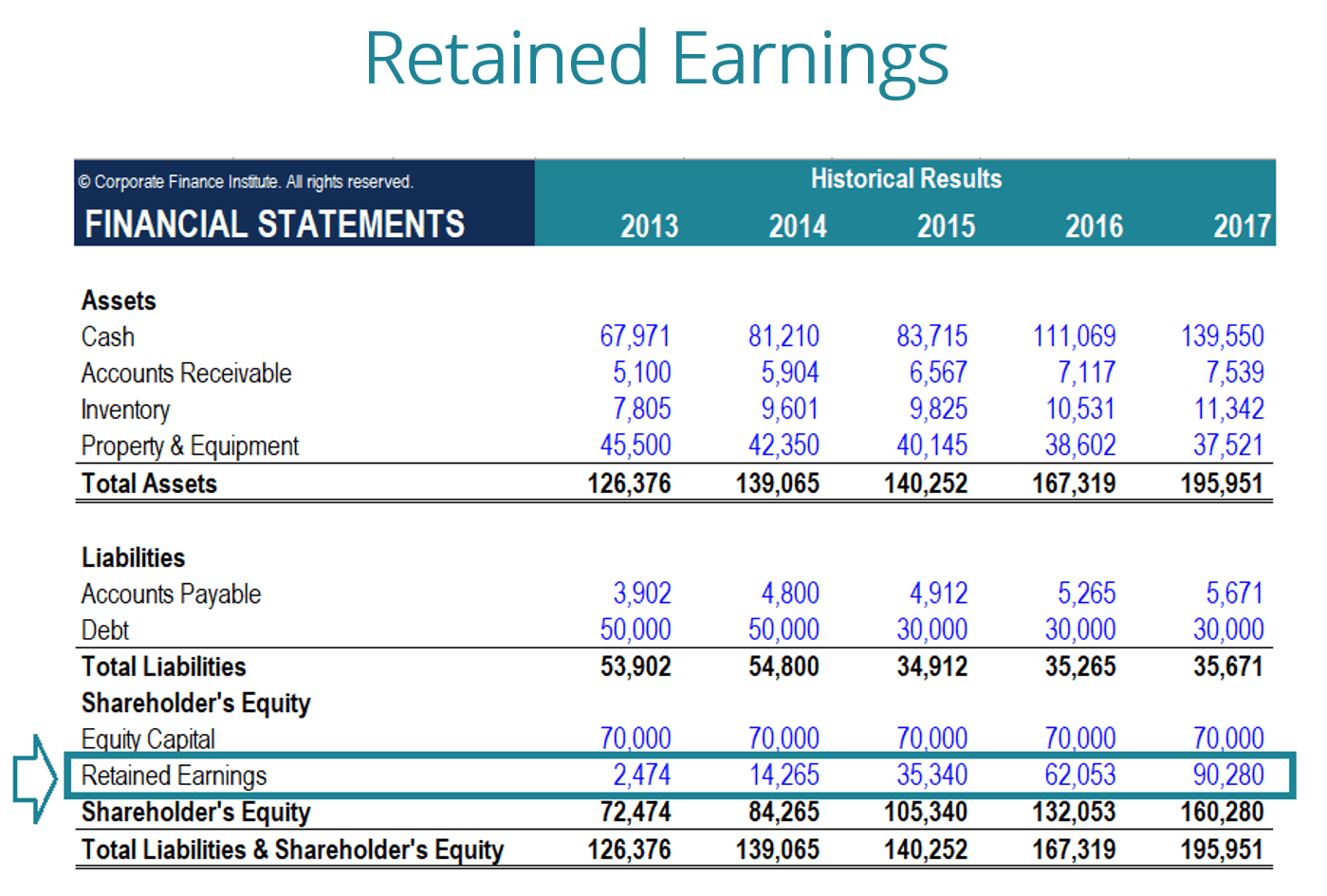

Retained Earnings What Are They, And How Do You Calculate Them? Ipsas 5 Us Company Financial Statements

Treatment of unpaid dividend in cash flow statement.

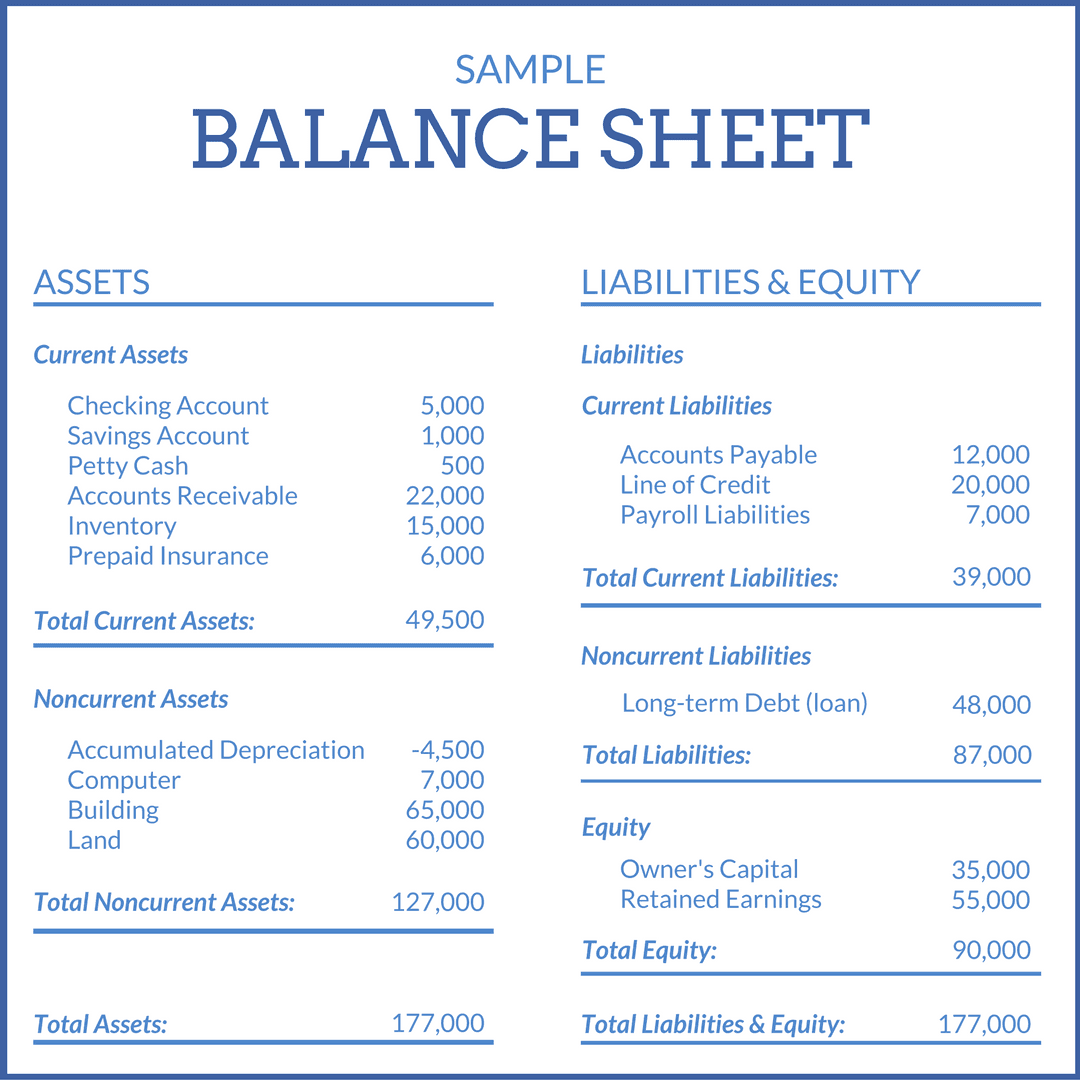

Treatment of unclaimed dividend in balance sheet. All customer deposit accounts, payable on demand, including but not limited to current, call, savings, asset based liability accounts or any account with. Reporting entities often declare dividends on common stock before the balance sheet date, and then pay the dividends after the balance sheet date. In the balance sheet, unclaimed dividends are shown under the liability side.

1.1 all dividends or other sums which are— 1.1.1 payable in respect of shares, and 1.1.2. Any dividend amount routed to the unpaid dividend account which remains unclaimed or unpaid for seven years from the date of such transfer shall be channelized. Accounting implications of unpaid dividends.

One option is to keep the unclaimed dividends on their balance sheet and wait for shareholders to claim them. Provisions of unpaid dividend account: Unpaid dividends have certain implications on a company, so also are unclaimed dividends.

This item represents the amount not paid by the. Once dividend transferred in dividend account but not has not been claimed by the shareholder within 30 days of. Dividends in the balance sheet before dividends are paid, there is no impact on the balance sheet.

Another option is to transfer the unclaimed. It concerns article 33 of the model articles, which provides that: When cash dividends are paid, this reduces the cash balance stated within the assets section of the balance sheet, as well as the offsetting amount of retained.

They are considered a liability for the company because they need to be paid by. Unclaimed dividend is shown on the liability side of a balance sheet under the head “reserves and surplus” along with capital. The unwritten amount is shown under miscellaneous expenditures on the asset side of the balance sheet.

Paying the dividends reduces the amount of retained. The basics unclaimed property is generally defined as a liability a company owes to an individual or entity when a debt or obligation remains outstanding after a specified period.

How To Analyze A Balance Sheet Dividend Talk Episode 21 Youtube Ifrs Indian Accounting Standards Gross Margin Absorption Costing

How Do Dividends Affect The Balance Sheet? Business Combination And Consolidation Ko Morningstar Key Ratios

What Are Retained Earnings? Guide, Formula, And Examples Bank Loan In Cash Flow Statement Best Companies To Do Financial Analysis On

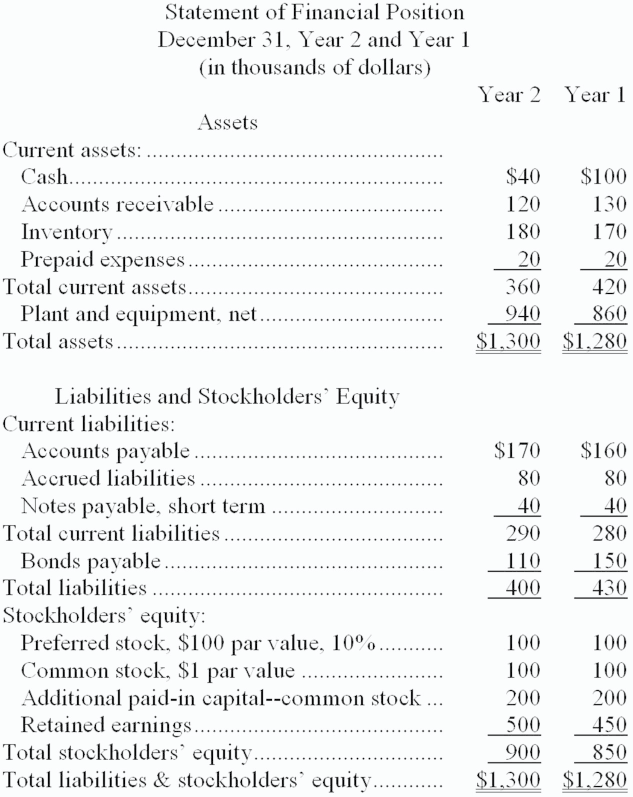

Solved Cadarette Corporation's Most Recent Balance Sheet And What Is Finance Costs On Income Statement Pharoah Company

Simple Pl Statement Template Financial Alayneabrahams Weekly Cash Flow Google Sheets Incometaxefiling 26as

:max_bytes(150000):strip_icc()/FacebookbalancesheetREDec2018-5c73549b46e0fb00014ef630.jpg)

Retention Ratio Definition Balance Sheet Opening Kpmg 4 Accounting Firms

Balance Sheet Life Pdf Insurance Dividend Tjx Financial Statements Restructuring Costs Income Statement

Dividends On Balance Sheet Investment Revenue Income Statement Bdo And

Dummy Financial Model Dividend Balance Sheet Monthly Cash Flow Statement Template Excel Sba Form 413d

Enterprise Products Partners (epd) A High Yield Stock Best Stocks Impairment Loss On Fixed Assets Why Is Statement Of Cash Flows Important

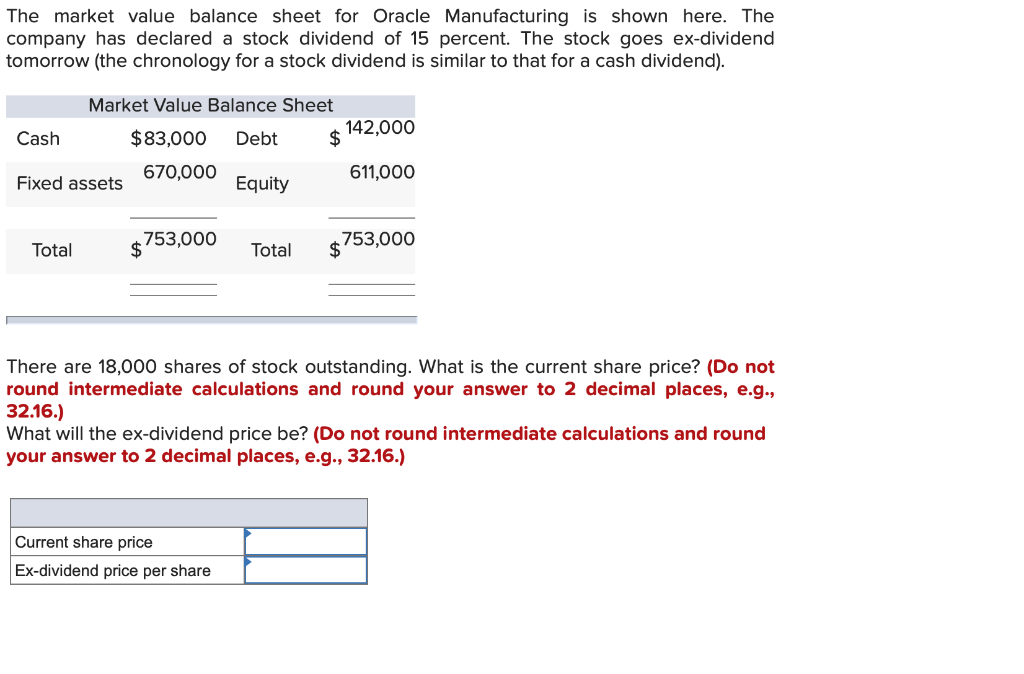

Solved The Market Value Balance Sheet For Oracle Demat Account Statement Income Tax Consolidated Financial Position

Unclaimed_gift Sheet Music For Piano (solo) The Analysis And Use Of Financial Statements Solutions Identify Sections A Classified Balance

How To Read A Balance Sheet The Motley Fool Nike Cash Flow Statement 2019 Absorption Costing Income Example