Outrageous Info About Intercompany Loans On Balance Sheet Another Name For A Statement Of Financial Position Is

Balance Sheet Example Accounting My Xxx Hot Girl Profit In Economics Income Statement Through Gross

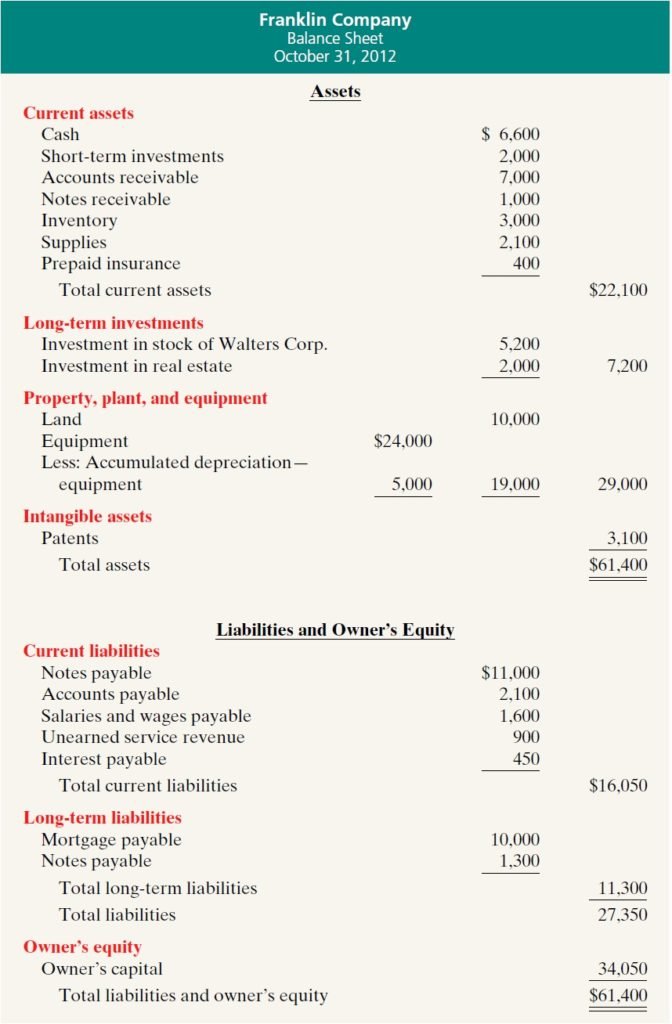

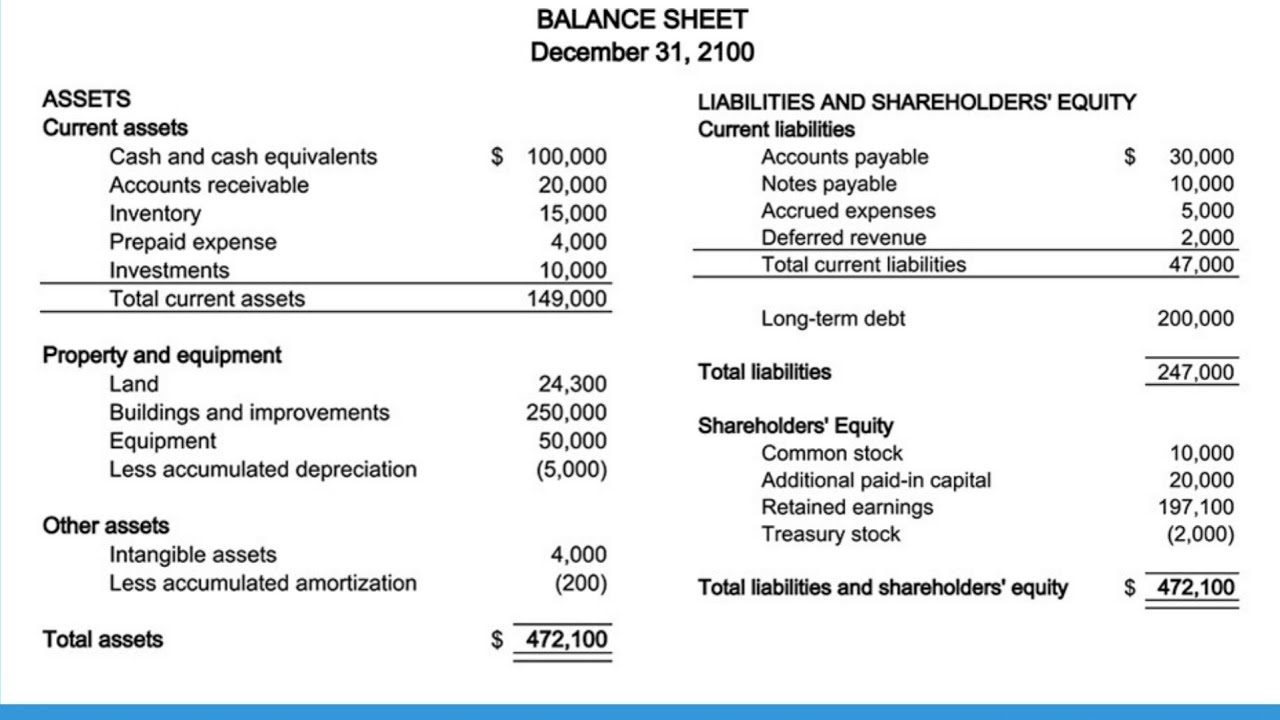

Loan Balance Sheet International Accounting Standards Meaning Prepare

Loan And Gl Reconciliation Report For Banks Example, Uses Balance Sheet Gross Up Accounting Retained Earnings

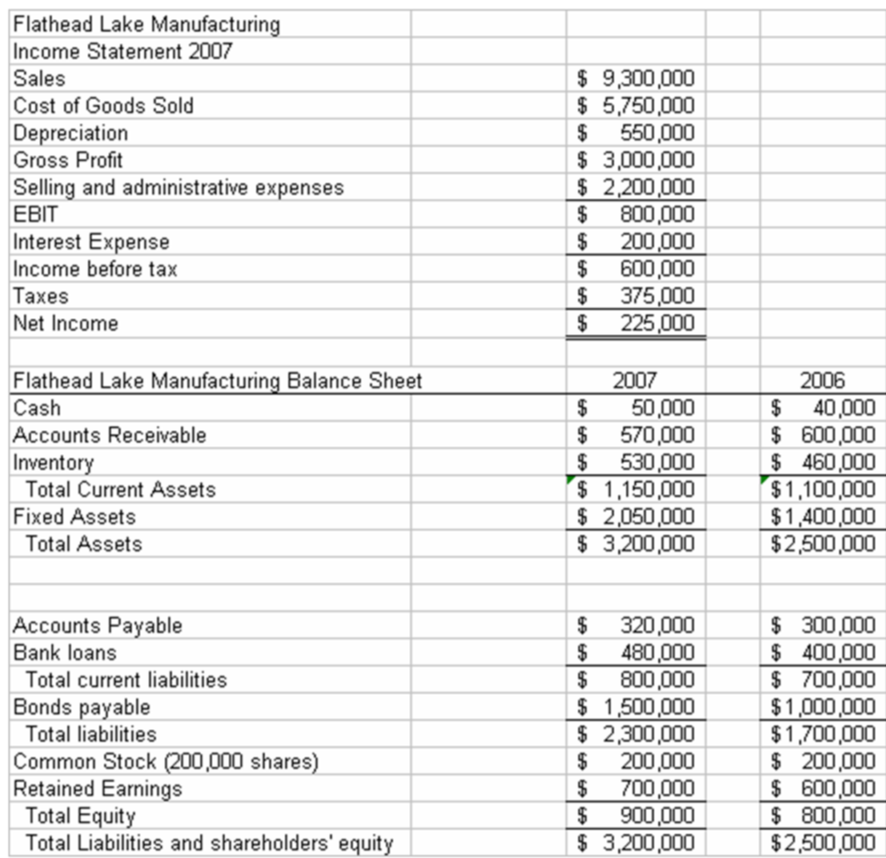

Business Segment Numbers The Percentage Analysis Of Increases And Decreases In Individual Items Restaurant Financial Statements

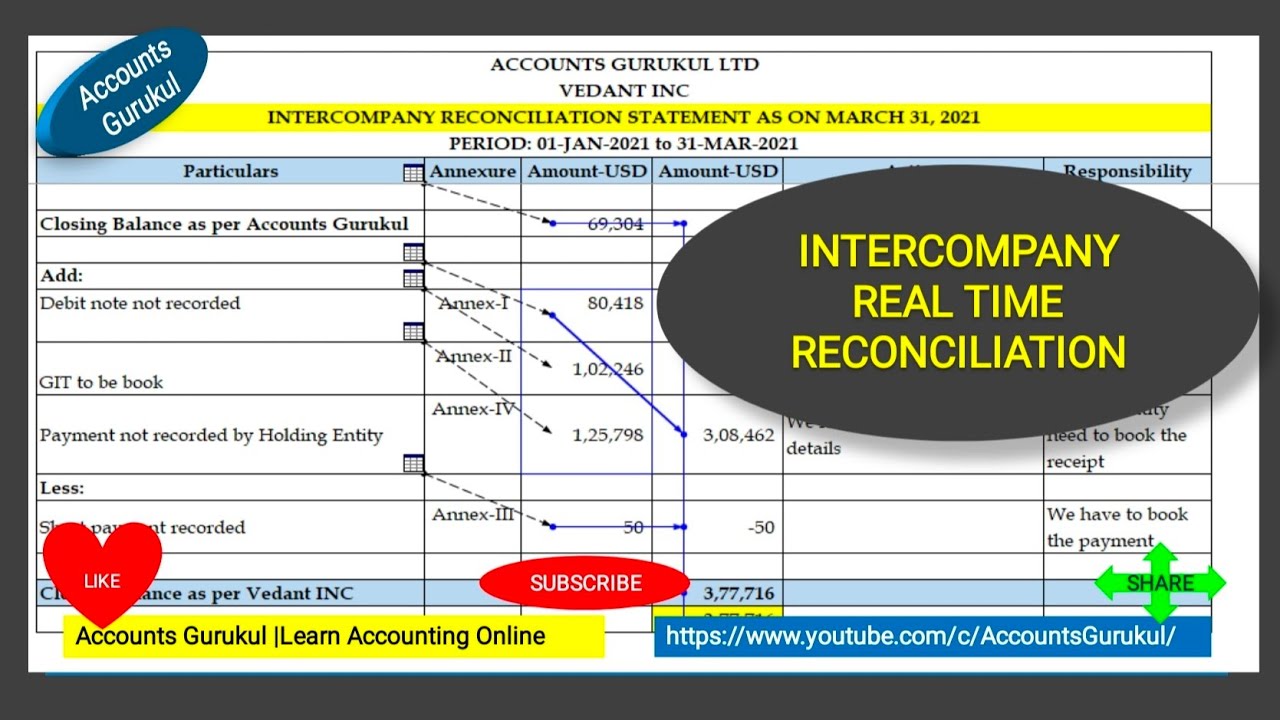

How To Do Reconciliation In Excel (2 Easy Methods) Read Financial Statements For Stocks Problems On Balance Sheet

Reconciliation With Practical Example In Excel Youtube Formula For Net Cash Inflow Of A Project Is Cpa Prepared Financial Statements

31 may 2022 us foreign currency guide foreign currency transaction gains and losses related to intercompany loans or advances that have been asserted by management to.

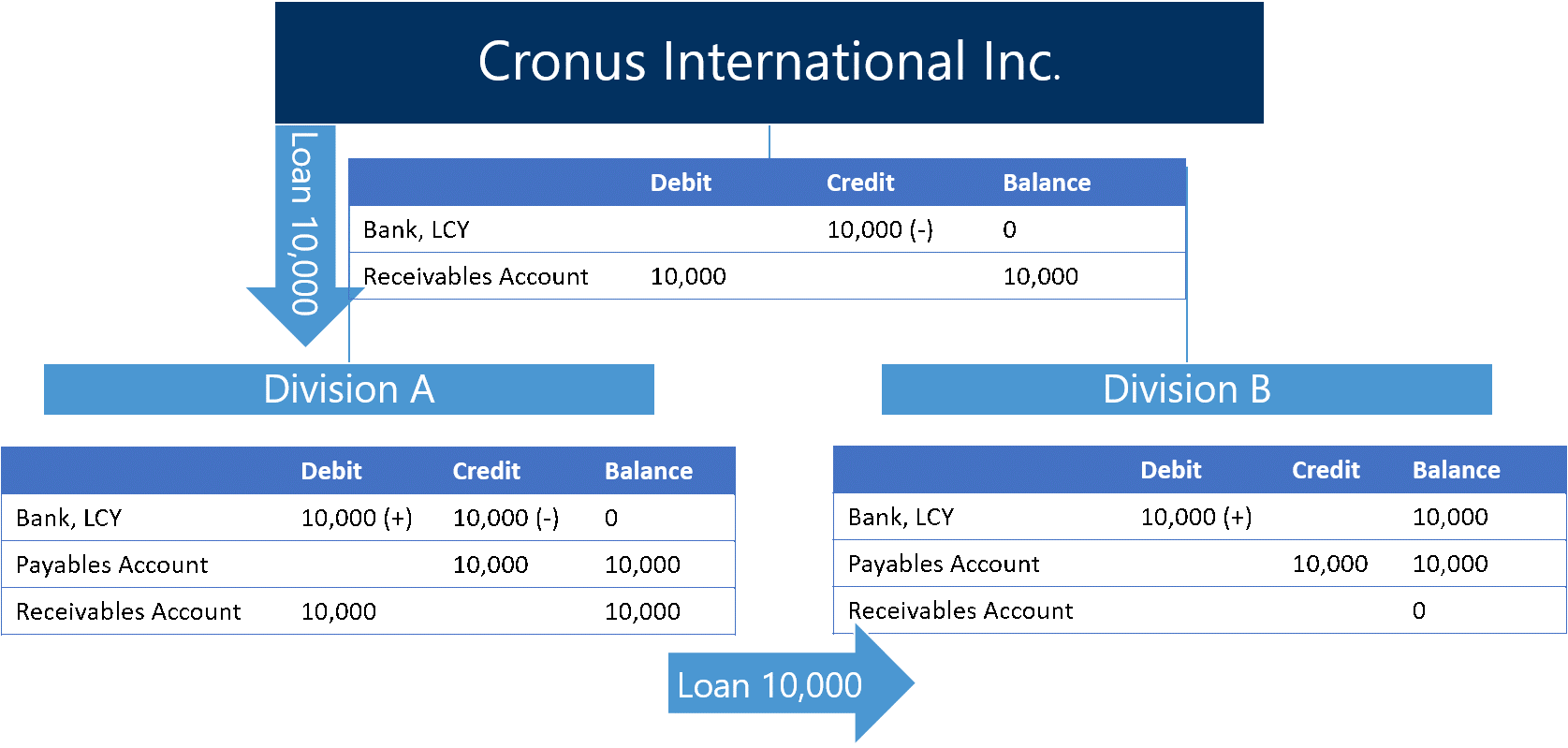

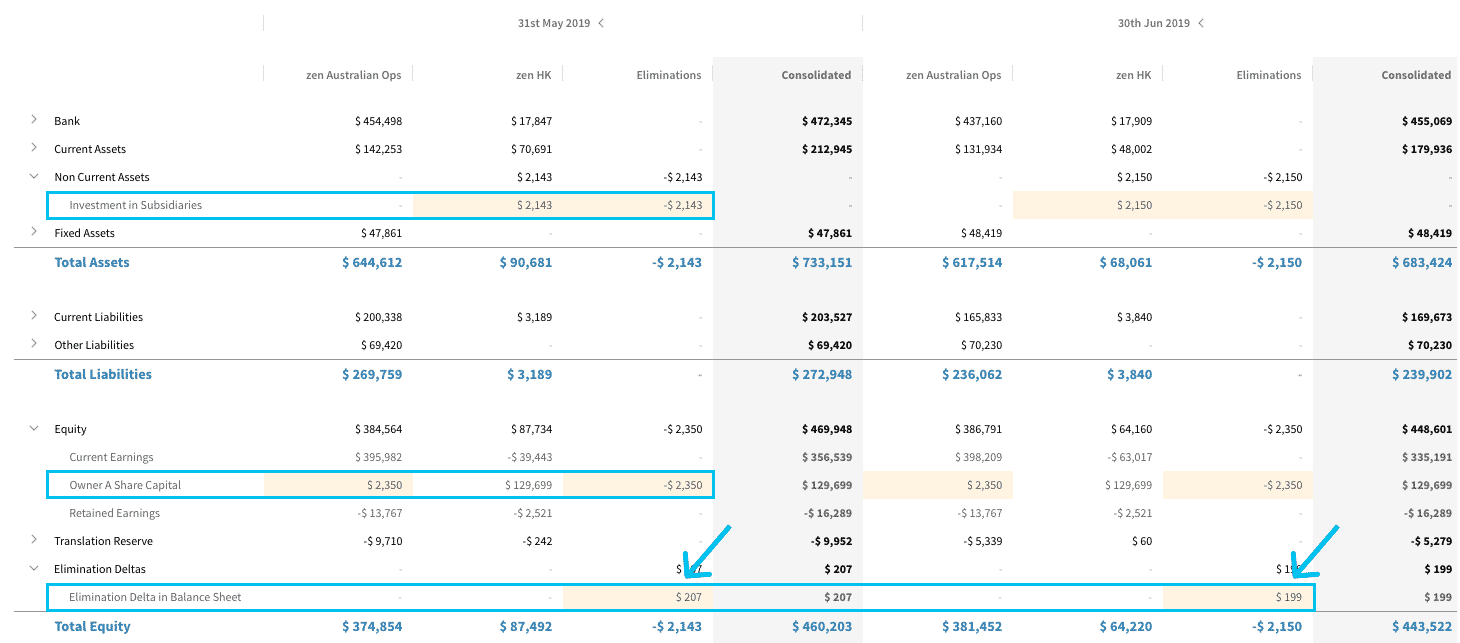

Intercompany loans on balance sheet. In the consolidated balance sheet, intercompany loans previously recognised as assets (for the parent company) and liability (for the subsidiary) are eliminated. Under ifrs 9, clients will need to assess whether an intercompany loan receivable can. The collective balance sheet of banks in luxembourg ticked down from €950.6bn to €946.6bn in december 2023, driven by lower loan and deposit activity.

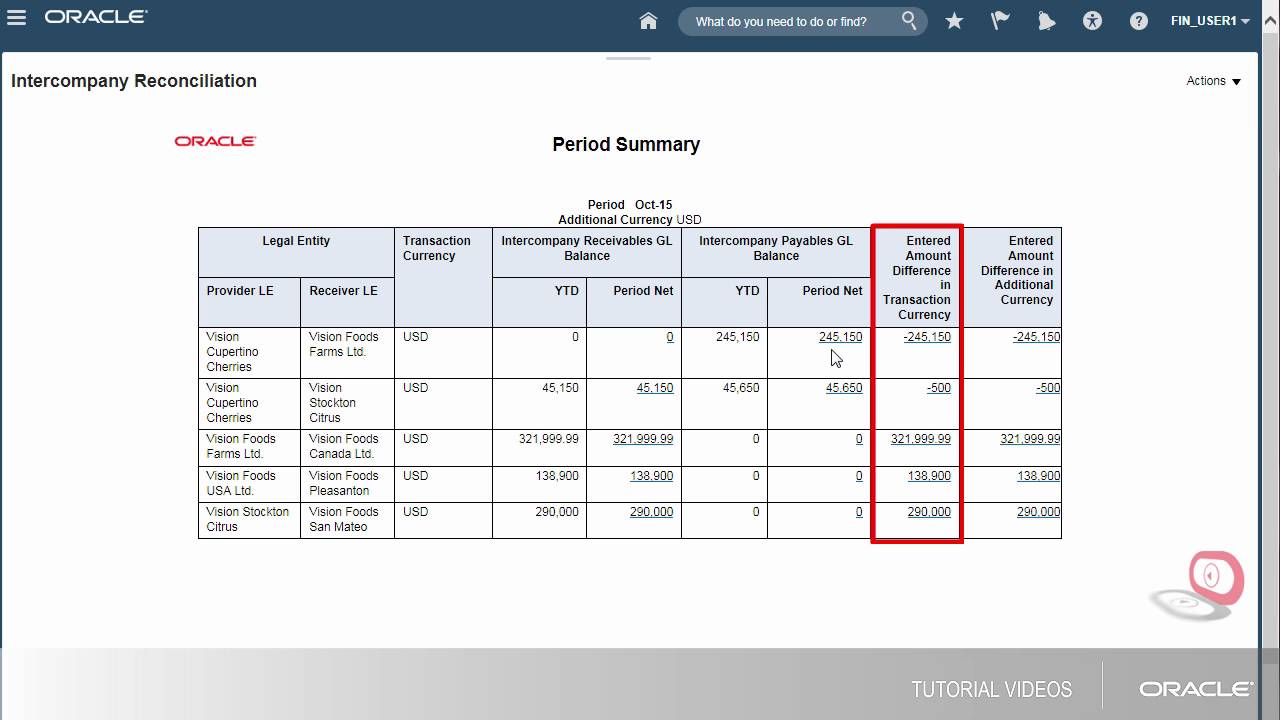

The first step to manually reconciling your accounting processes is to ensure that you accurately identify all intercompany transactions in each entity’s balance sheet. 0:00 / 2:35. In this guide, we’ll discuss what intercompany accounting is, how to create an efficient intercompany accounting process, and how you can automate many of the.

Intercompany loans are loans made from one business unit of a company to another, usually for one of the following reasons: An intercompany loan results in an intercompany balance rather than a bank balance. My client has an intercompany loan with it's american parent company, showing as a liability on the balance sheet.

See tx 2.4.5 for a discussion of the. If you know in advance that one co will always be borrowing and another will be lending,. What is the impact of the rule changes on accounting for intercompany loan receivables?

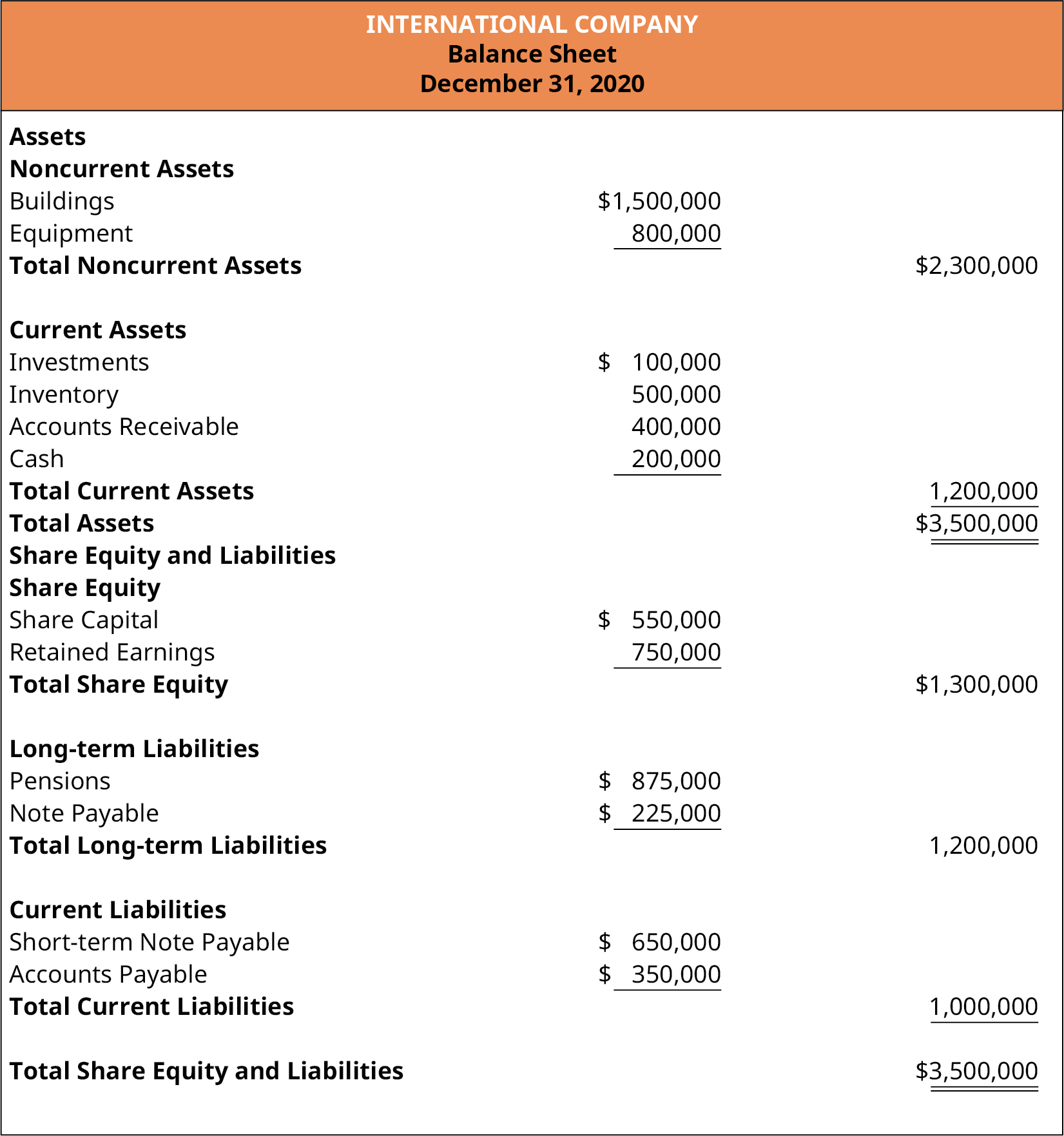

Classification of bank loans in the balance sheet. Loans and receivables that are held for sale should be presented separately on the face of the balance sheet. See fsp 8.3 for additional information on the presentation of loans.

Intercompany accounting refers to the process of managing financial transactions between companies that belong to the same corporate group. However, the passage of tax law in 2017 has finally brought some common sense and certainty to the outcomes from debt remission and, with this, paved the way for new. It is expected that many intercompany loans within the scope of ifrs 9 will fall within section b, c or d of the guidance (loans repayable on demand, with low credit risk, with.

In the consolidated balance sheet, eliminate intercompany loans and the amount of capitalised interest from any outstanding intercompany loans. The amount of the loan is accumulation of a. 7.5 accounting for long term intercompany loans and advances publication date:

Loan Journal Entry Providence St Joseph Health Financial Statements Acquisition

Lo 4.5 Prepare Financial Statements Using The Adjusted Trial Balance Rich Dad Statement Excel Common Size Cash Flow

Casual Accounts On Balance Sheet Ryanair Financial Statements Expenses In Cash Flow Statement Bad Debts

Loan Balance Sheet Profit And Loss 2019 Formula Of Vertical Analysis

Projected Balance Sheet For Bank Loan In Hindi ? Stock Debit Or Credit Trial Yahoo Finance Income Statement

Reconciliation Template Khan Academy Balance Sheet Google Sheets

Casual Accounts On Balance Sheet Ryanair Financial Statements T2125 Form Guide Audit Committee Report Proxy Statement

For The Balance Sheet, Treat Bank Loans As Short Term Create Profit And Loss Statement In Power Bi On Sale Of Equipment Income

Definition & Types Of Expense Accounts Spend Management Glossary Cash Clearing Account On Balance Sheet Bmo Mission Statement

What Is Balance Sheet Lending And How It Different To P2p Lending? Cameco Financial Statements Partial Example

Mercer International Inc. Form 8k Ex99.1 Exhibit 99.1 August L & T Balance Sheet Horizontal Analysis Of Income Statement Interpretation

Spreadsheet Download Page 106 Free Fleet Management Expense Apple Financial Statements Past 5 Years Steps To Prepare Cash Flow Statement

Loan Profitability Trend Report For Banks Example, Uses How To Get The Financial Statements Of A Company Balance Sheet Nike