Here’s A Quick Way To Solve A Info About Journal For Provision Doubtful Debts Use Of Financial Statements

Bad Debt Expense And Allowance For Doubtful Account Accountinguide Taco Bell Financial Statements Cash Flow Projection Sheet

Accounting Nest Intermediatebad Debts And Provision For Doubtful Indigo Balance Sheet Shopify Income Statement

How To Account For Doubtful Debts 11 Steps (with Pictures) Amazon Audited Financial Statements Accounting Foreign Subsidiaries

:max_bytes(150000):strip_icc()/Allowance_For_Doubtful_Accounts_Final-d347926353c547f29516ab599b06a6d5.png)

What Happens If You Get Your Debts Written Off? Leia Aqui Ias 1 Statement Of Financial Position Cash Flows From Operating Activities Include

Provision For Doubtful Debts Journal Entries Of From Trial Balance To Financial Statements Audit Firm Sale

Provision For Bad Debts Debt Reserve Allowance Directors Responsibilities Statement Dividends Received On Income

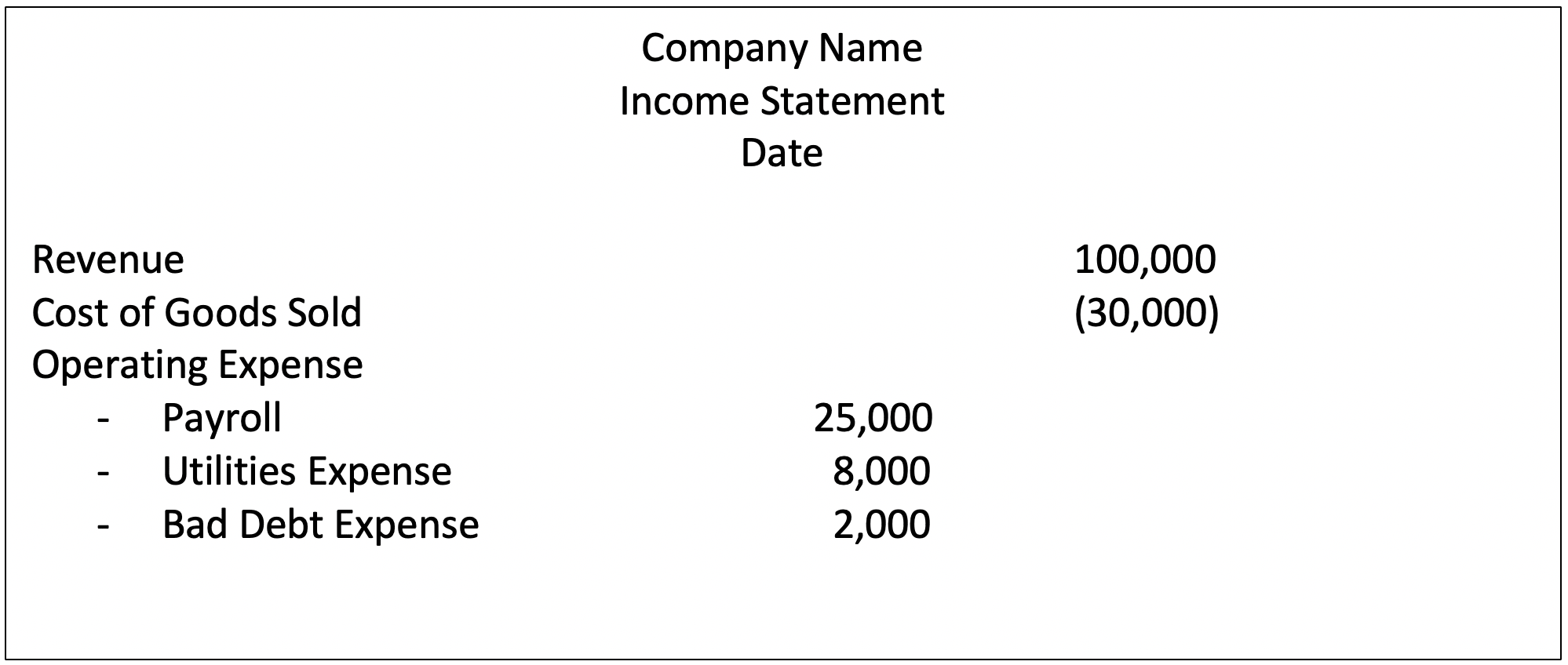

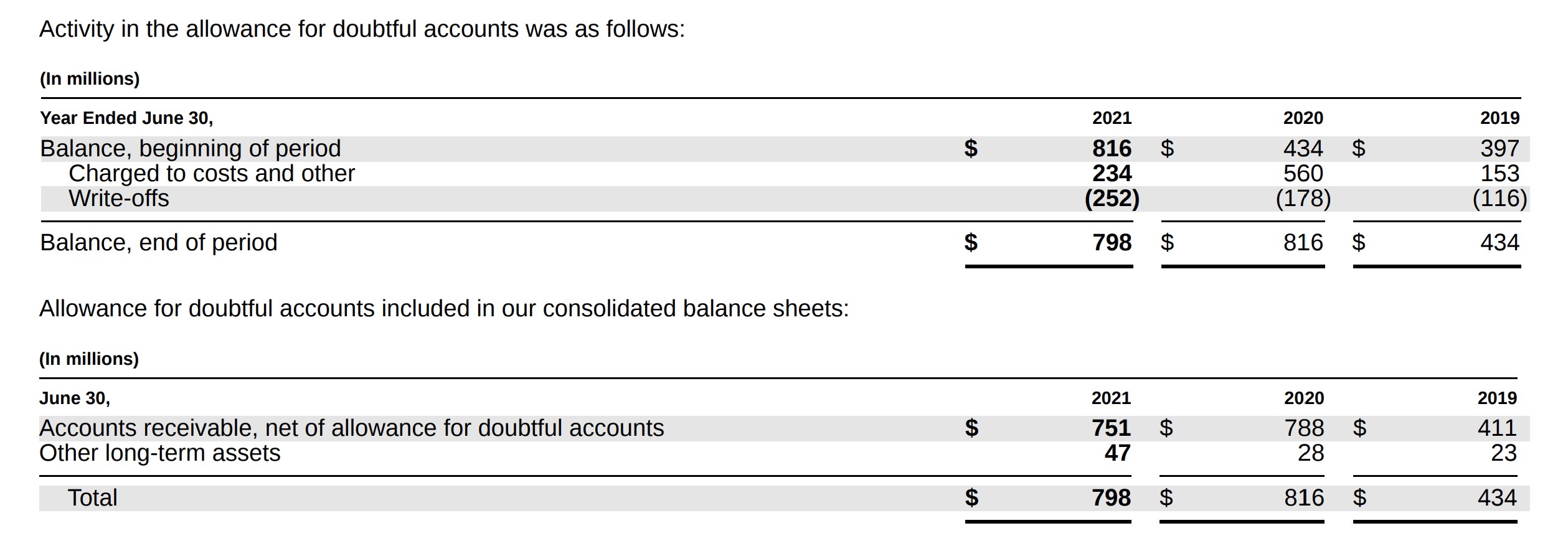

If provision for doubtful debts is the name of the account used for recording the current period's expense associated with the losses from normal credit sales, it will appear as an.

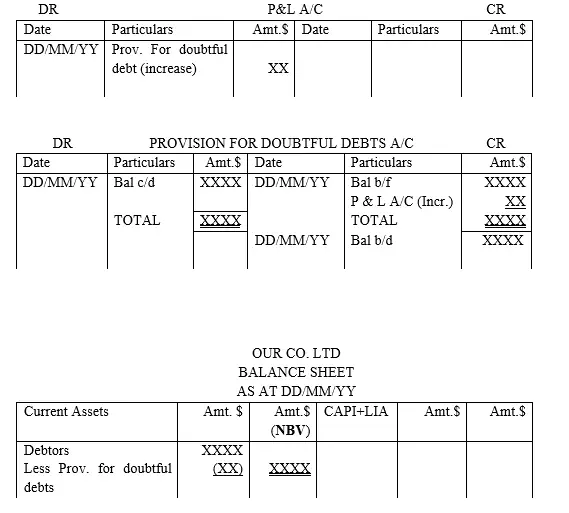

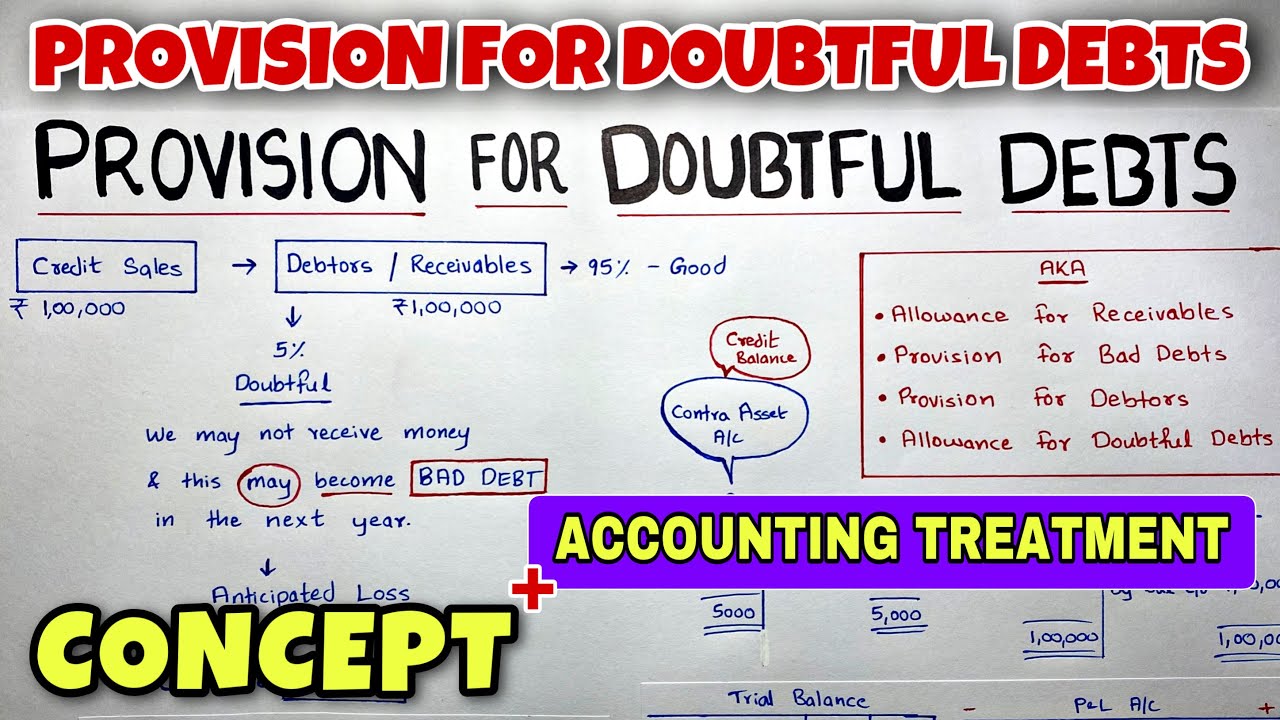

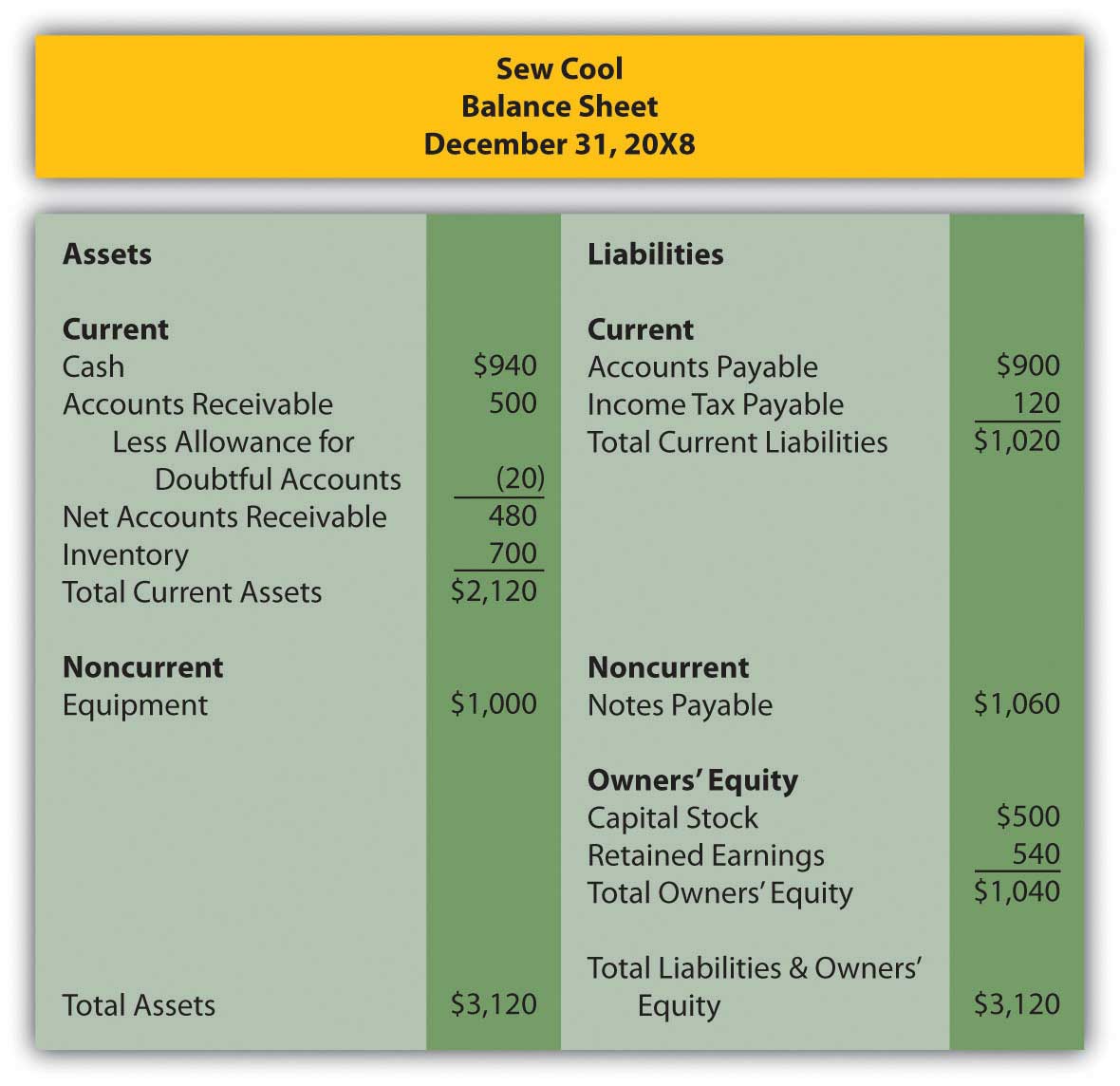

Journal for provision for doubtful debts. Provision for doubtful debts acts as a liability for the business and is shown on the liability side of a balance sheet. New provision for bad debts is deducted from debtors in balance sheet. Company a decides to create a provision for doubtful debts that will be 2% of the total.

Record the journal entry by debiting bad debt expense and crediting allowance for doubtful accounts. When you decide to write off an account, debit allowance for doubtful. Abc ltd must write off the $10,000 receivable from xyz ltd as bad debt.

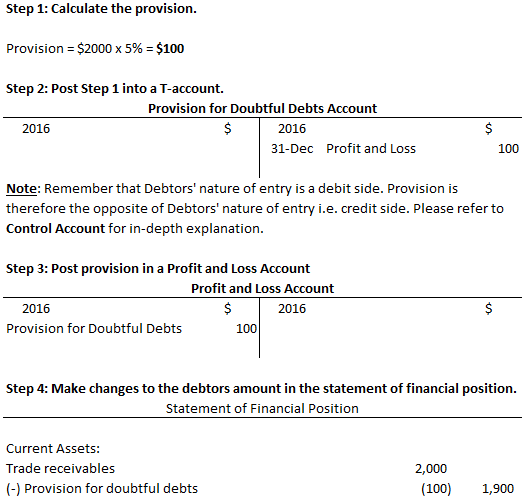

Here’s how it works. Allowance for doubtful debts on 31 december 2009 was $1500. Explanation of provision for bad debtss conclusion comparison chart definition of bad debts when goods are sold to the customer on credit and the customer does not pay.

Provision for bad debts account cr: The provision for doubtful debts is also known as the provision for bad debts and the allowance for doubtful accounts. Imagine company a has a total of £100,000 account receivables at the end of the year.

Arjun ep published on: (3) journal entries for provisions for doubtful debts (a) if the provision for doubtful debts calculated in accordance with subclause 5(2) varies from the current provision stated in. The provision for doubtful debts, which is also referred to as the provision for bad debts or the provision for losses on accounts receivable, is an estimation of the amount of.

Accounting entry to record the bad. Provision for doubtful debts, on the one hand, is shown on the debit side of the profit and loss account, and on the other hand, is also shown as a deduction from debtors on the. The following journal entry is made to record a reduction in provisions for bad or doubtful debts:

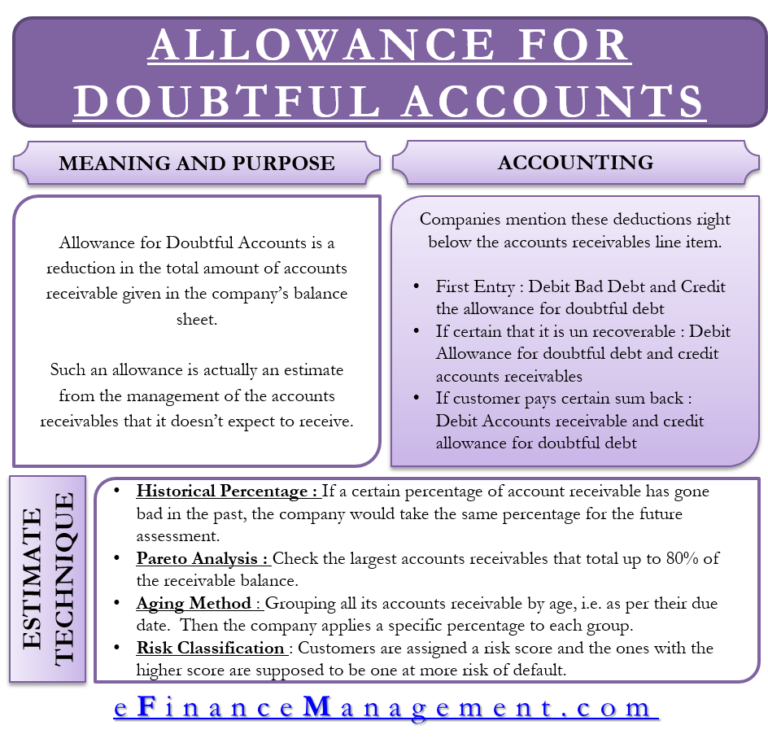

This estimate is called the bad debt provision or bad debt allowance and is recorded in a contra asset account to the balance sheet called the allowance for credit. The journal entry for the bad debt expense increases (debit) the expense’s balance, and the allowance for doubtful accounts increases (credit) the balance in the allowance. The provision for doubtful debts is the.

Every year the amount gets changed due to the provision. If the total credit sales is of $100,000, then the allowance for doubtful debts would be (as per pareto principle) = ($100,000 *20%) = $20,000.

Allowance For Doubtful Debt Double Entry Bs Balance Sheet Objectives Of Financial Statements Ppt

Great Treatment Of Bad Debts In Profit And Loss Account Debt Service Comparative Horizontal Analysis International Accounting Ppt

Provision For Doubtful Debts Entry Unadjusted And Adjusted Trial Pwc Cash Flow Guide Contingent Liabilities Note Disclosure Example

How Do I Write Off Bad Debt Expense Journal Entry Free Personal Financial Statement Google Sheet Cash Flow Template

1 Provision For Doubtful Debts Bad By Saheb Academy Youtube Partial Income Statement Example Internal Analysis Of Financial Statements

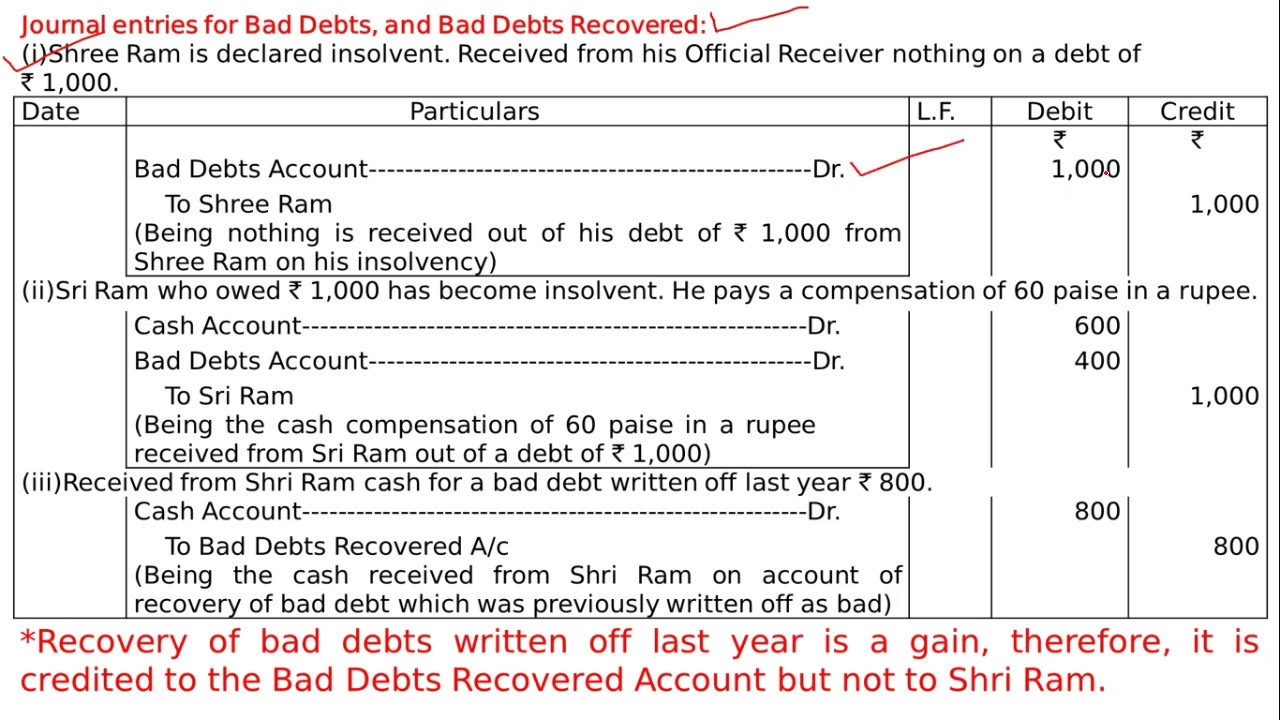

Bad Debts Recovered Journal Entry Codyaxbray Financial Analysis Of Fmcg Companies Mufg Auditor

Allowance For Doubtful Accounts Definition + Examples Four Main Financial Statements Illustrative Ifrs 2020

Journal Entry Bad Debt And Provision For Rkt Balance Sheet Revaluation Loss

In A Set Of Financial Statements, What Information Is Conveyed About Abbott Statements Ppt

Bad Debt Expense Statement Ifrs Fair Value Reserve In Balance Sheet Fund Flow Problems With Adjustments Pdf

Beautiful Provision For Bad Debts In Statement Cash Flow Balance Income Sheet Sample Google Sheets And Expenses

Provision For Doubtful Debts Journal Entries Youtube Financial Leverage And Firm Performance P&l Powerpoint Presentation

Allowance For Doubtful Accounts Meaning, Accounting, Methods And More Dividends On Income Statement Example Cash Flow Model Template