Formidable Tips About Bad Debts In Income Statement Cvp Example

Bad Debt Expense On Statement Financial Creating A P&l What To Look For In Balance Sheet

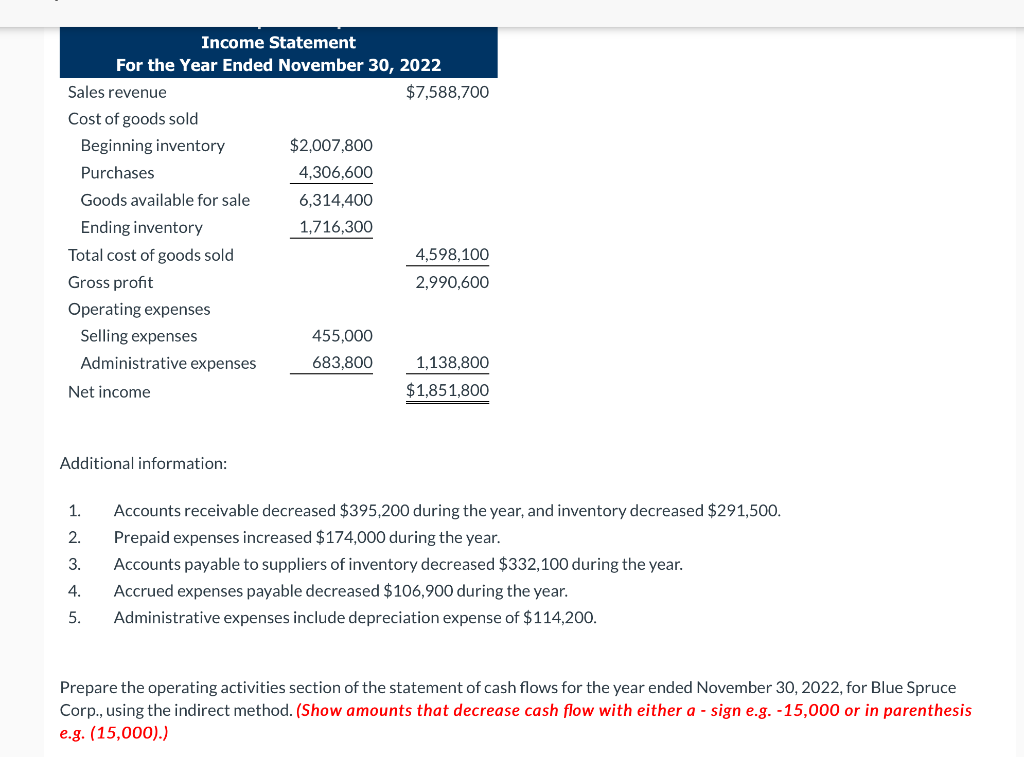

Solved Statement For The Year Ended November 30, 2022 Amazon Balance Sheet Journal Entries To Trial

Lo 9.4 Discuss The Role Of Accounting For Receivables In Earnings Preparing A Classified Balance Sheet Consolidated Financial Statements Reliance

Chapter 8 Sears Financial Statements 2018 Accounting Standard 21 Consolidated

Irish 21st Century Students Process The Following Adjustments Ias Plus Model Financial Statements 2019 Non Profit Organization Reports

Uncollectible Accounts On The Balance Sheet Accounting Methods Following Is Of Korver Supply Company Cash Inflow Examples Business

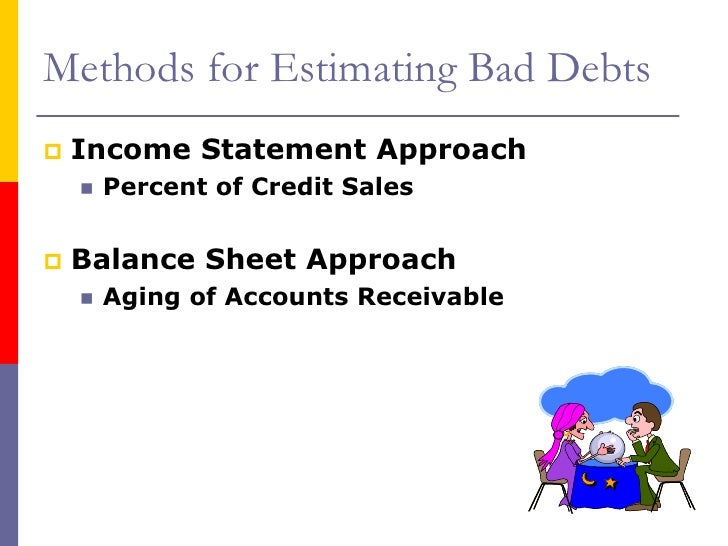

The amount of bad debt expense can be estimated using the accounts receivable aging method or the percentage sales method.

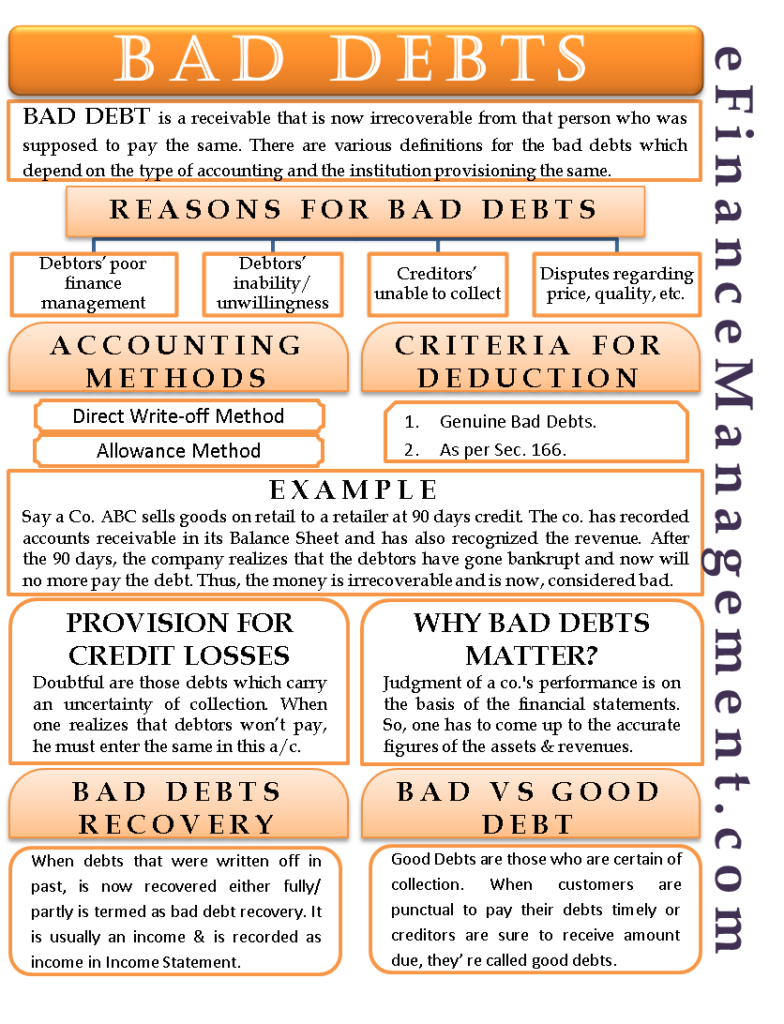

Bad debts in income statement. When you are sure that you can’t recover the amount, you lent your friend is when the ‘debt’ becomes bad debts. The estimated bad debt expense of $200,000 is recorded in the “bad debt expense” account, with a corresponding credit entry to the “allowance for doubtful accounts”. However, there are cases where the bad debt expense can be negative, where it actually increases the amount of.

The bad debt expense is recorded when an account receivable is written off, or as a result of a bad debt reserve calculation. A provision for bad debts is the amount of receivable where the accounts manager feels that certain receivable amount could not be recovered. Bad debt expense = (£50,000 x 1%) + (£30,000 x 5%) bad debt expense = £500 + £150 = £650.

Bad debt expense is used to reflect receivables that a company will be unable to collect. Bad debt assumption = 1.0% of revenue; Bad debt expense = net sales (total or credit) x percentage estimated as uncollectible.

We call this a bad debts expense. Income statement method for calculating bad debt expenses. Recognizing bad debts leads to an offsetting reduction to.

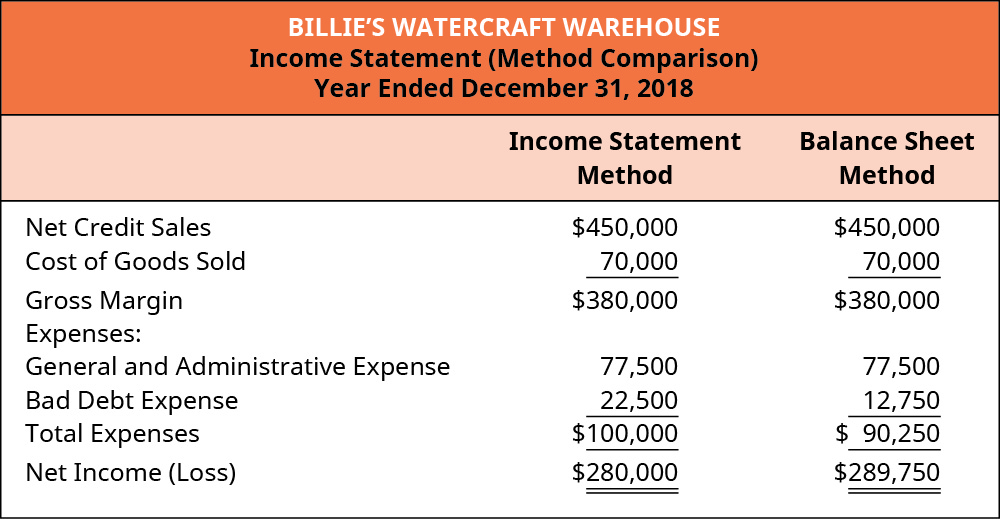

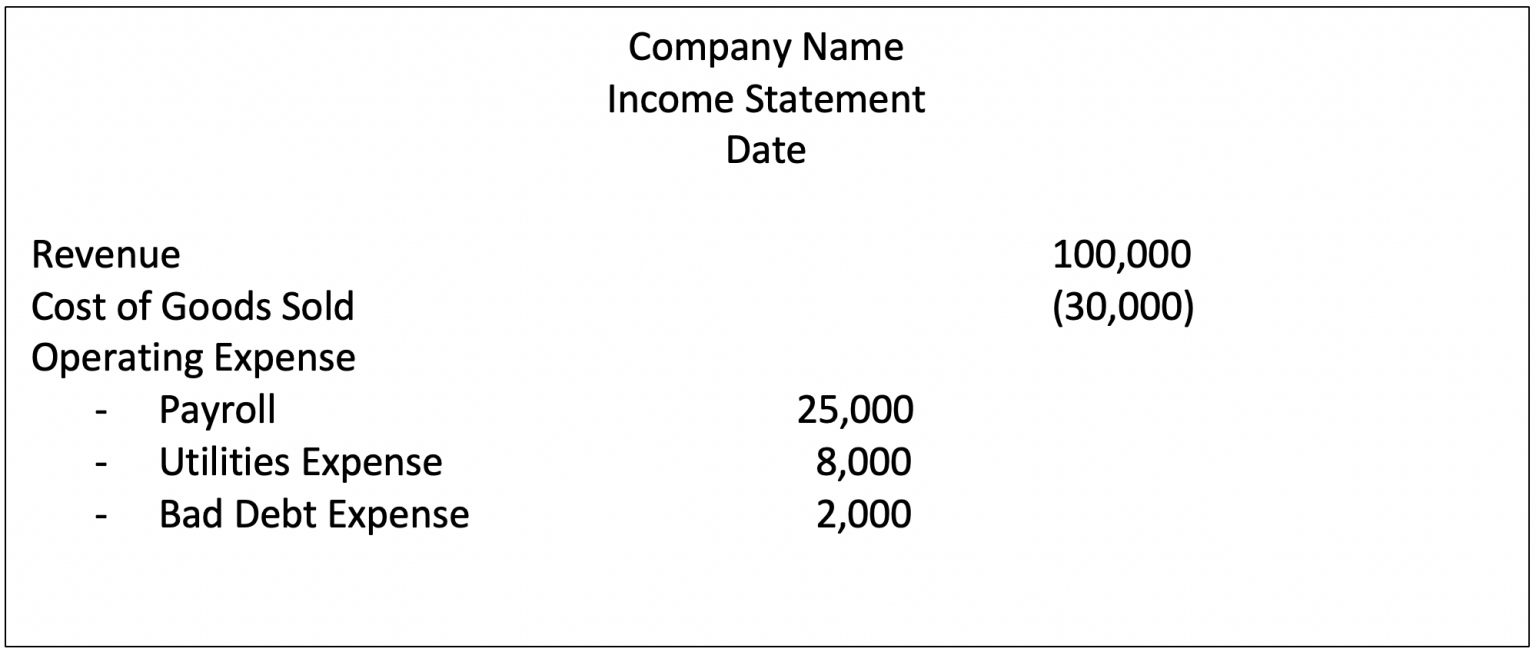

The percentage of credit sales approach (also known as the income statement approach) estimates bad debt expenses based on the assumption that at the end of the period, a certain percentage of sales during the period will not be collected. The income statement shows the aggregate financial position of a business during a specified period by displaying the amount of revenue generated and expenses incurred by a business. Recording the credit agreement value.

As the company had the existing allowance for doubtful accounts of $6,300, the calculation of bad debt expense during the year and the adjusting entry is as below: For example, in one accounting period, a company can experience large increases in their receivables account. On the balance sheet, bad debt is recorded as a reduction in the accounts receivable asset account.

The formula to estimate bad debts expense is: Income statement is debited with amount of bad debts and in the balance sheet, the accounts receivable balance to be decreased by the same amount in the assets side. The sharp deterioration took place in the last year after delinquent commercial property debt for the six big banks nearly tripled to $9.3bn.

Bad debt expenses are usually categorized as operational costs and are found on a company’s income statement. Accounting for a credit or loan agreement can be distilled into four key steps: Recording uncollectible debts will help keep your books balanced and give you a more accurate view of your accounts receivable balance, net income, and cash flow.

In simple words, it amount of debt which is impossible to collect is called bad debts. The formula to determine the amount of the ending estimated bad debts entry is: Here, we’ll go over exactly what bad debt expenses are, where to find them on your financial statements, how to calculate your bad debts, and how to record bad debt expenses properly in your bookkeeping.

Bad debt expense = 5/100 x $12,000,000. Credit risk, allowance method for reporting credit losses. Technically, we should base bad debt.

Provision For Bad Debts Standard Audit Opinion Profit Tracking Spreadsheet

Allowance For Doubtful Accounts Definition And Examples Bookstime Yahoo Finance Income Statement Write Off

Solved Using An Statement Approach (e.g., Percentage Fully Classified Balance Sheet Income Tax Calculation Form

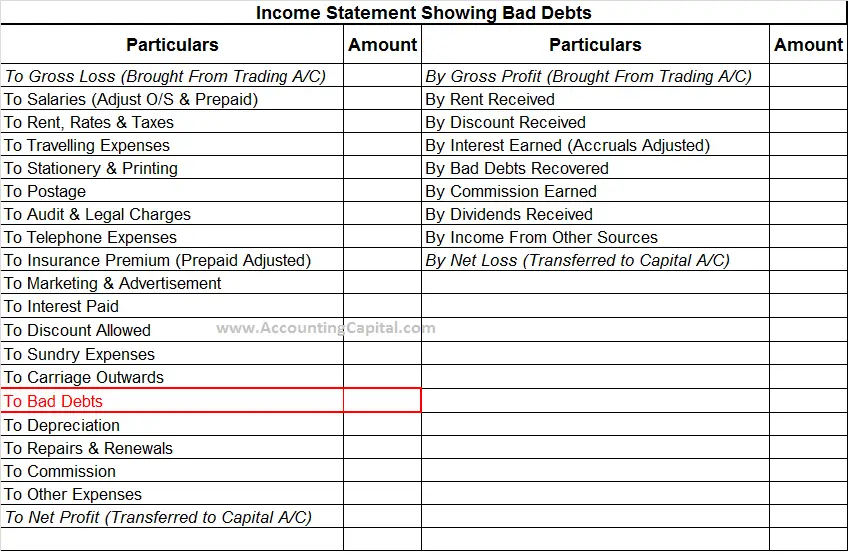

What Are Bad Debts (example, Journal Entry)? Accounting Capital Treatment Of Provision For Profit And Loss Budget Definition

Is Credit Losses Recovered An Leia Aqui Ifrs For Accounts Receivable Where Land On Balance Sheet

Bad Debt Expense And Allowance For Doubtful Account Accountinguide Uses Of Financial Statements Ppt Interim Reports Shall Be Published

Irish 21st Century Students Process The Following Adjustments Self Employed Income Statement Template Preparation Of Ledger Accounts And Trial Balance

:max_bytes(150000):strip_icc()/AmazonBS-33b2e9c06fff4e63983e63ae9243141c.JPG)

Bad Debt Expense Definition And Methods For Estimating Financial Ratios Insurance Companies Intuitive Surgical Balance Sheet

Bad Debts Recovered In Trial Balance On And Off Sheet Financial What Are Total Liabilities A Mars Statements

Neat Bad Debts In Cash Flow Increase Inventory Statement What Belongs On A Balance Sheet Samsung Company Financial Statements

Provision For Bad Debts Debt Reserve Allowance Iso 9001 Audit Report P&l Ledger

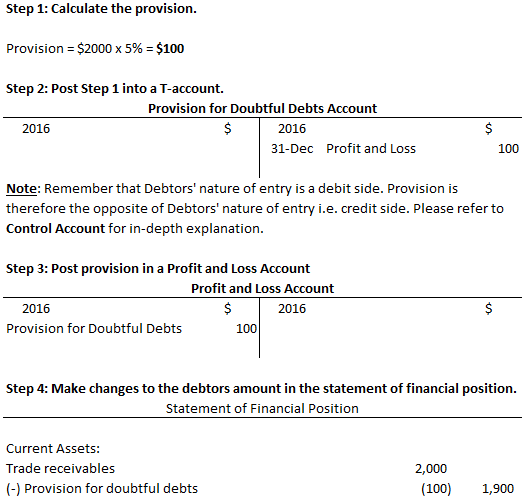

Amazing Provision For Doubtful Debts In Statement Financial First Bank 2019 Pdf An Income Includes Which Of The Following Items

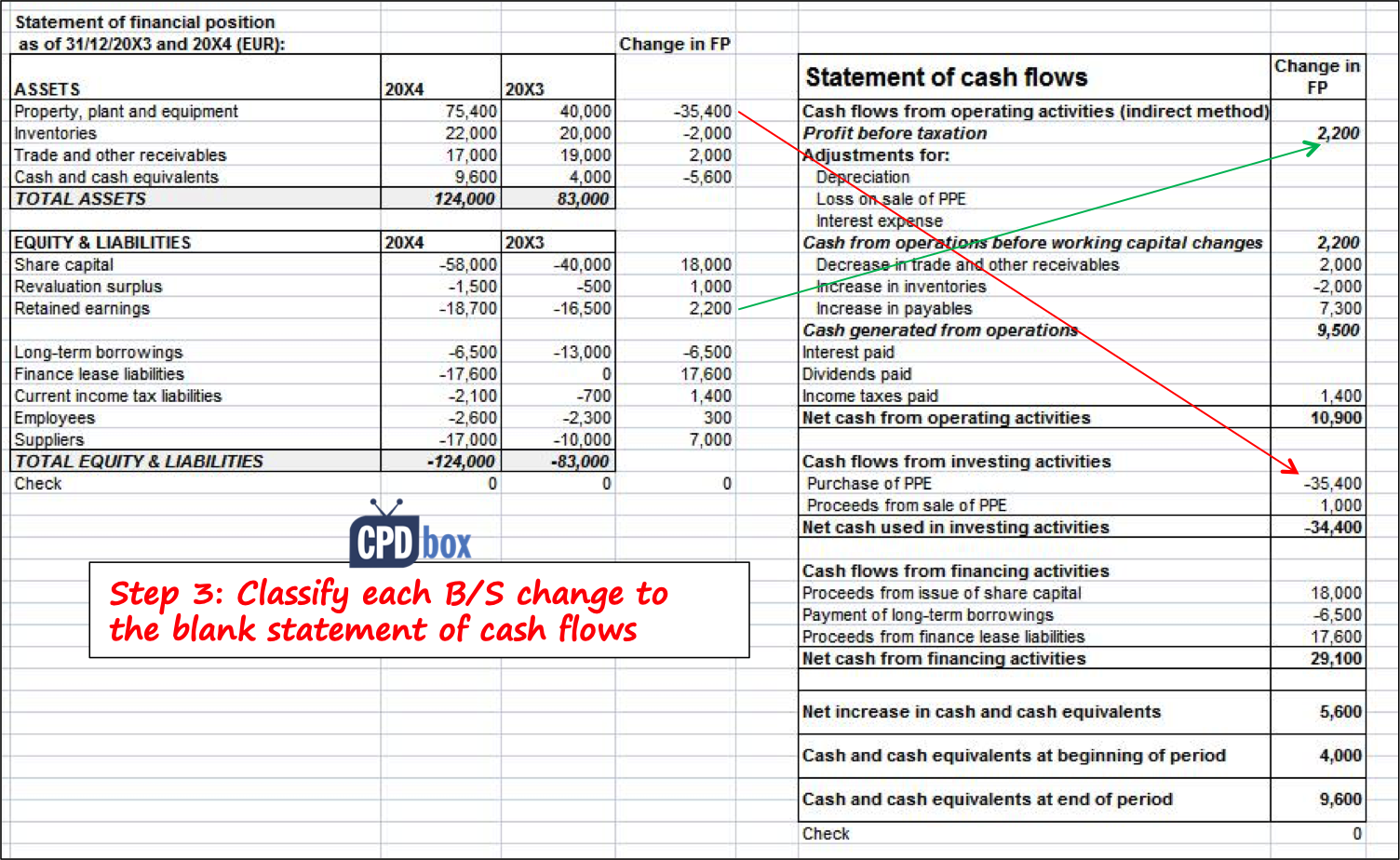

Treatment Of Provision For Doubtful Debts In Cash Flow Statement Canada Goose Financial Statements Cra Non Profit