Exemplary Tips About Expenses In Profit And Loss Account Writing A Balance Sheet

Profit And Loss Account Meaning, Format & Examples Tutor's Tips A133 Audit Report Required Financial Statements Under Gaap

Best Accounting Software In The Usa Start Now With A Free Trial! Aapl Financial Statements Md&a Annual Report

Gross Margin Ratio Learn How To Calculate What Are The Types Of Financial Statements Do A Statement Position

Text Sign Showing Profit Loss. Conceptual Photo Financial Year End Statement Of Position Assets Performance A Company

The Beginner's Guide To Profit And Loss Statements Pepsico Financial 2018 Electrolux

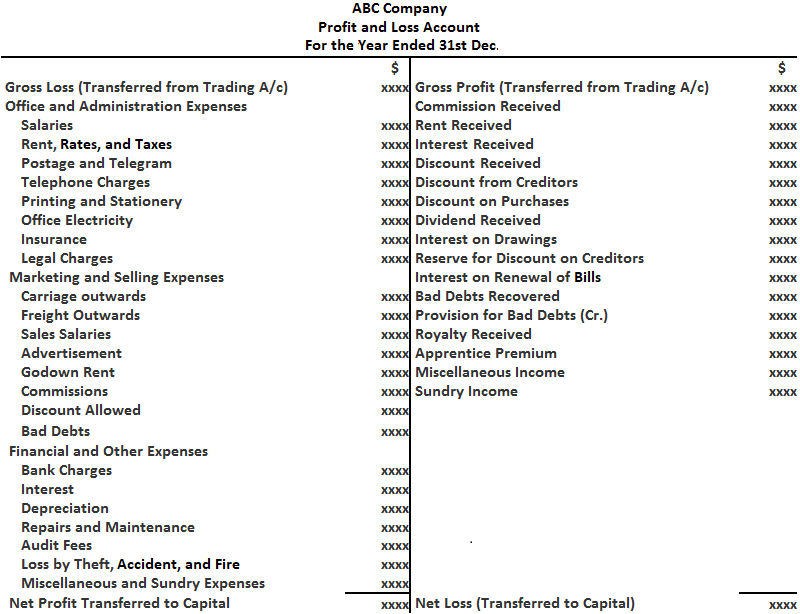

For earning the net profit, a businessman has to incur many more expenses in addition to the direct expenses.

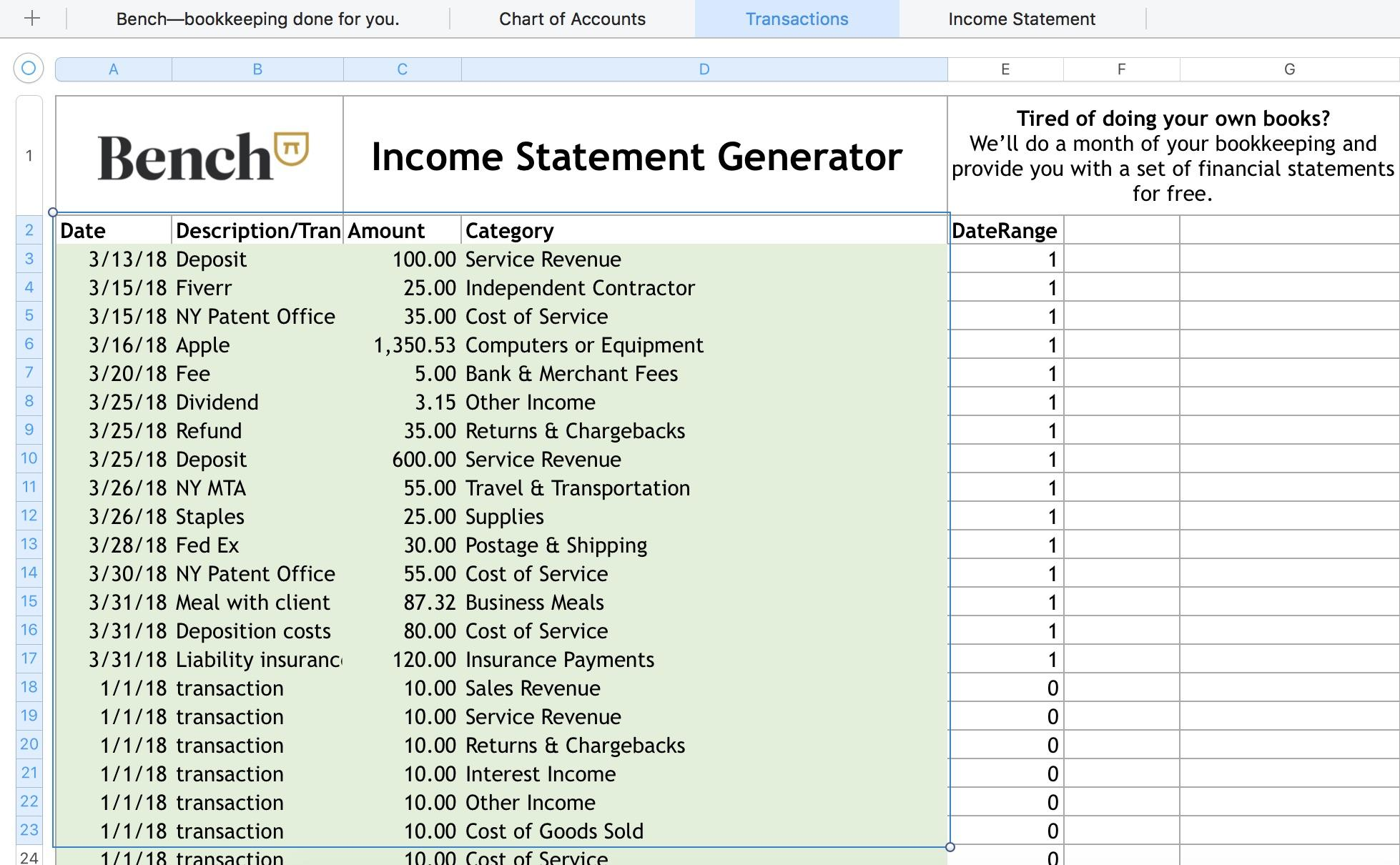

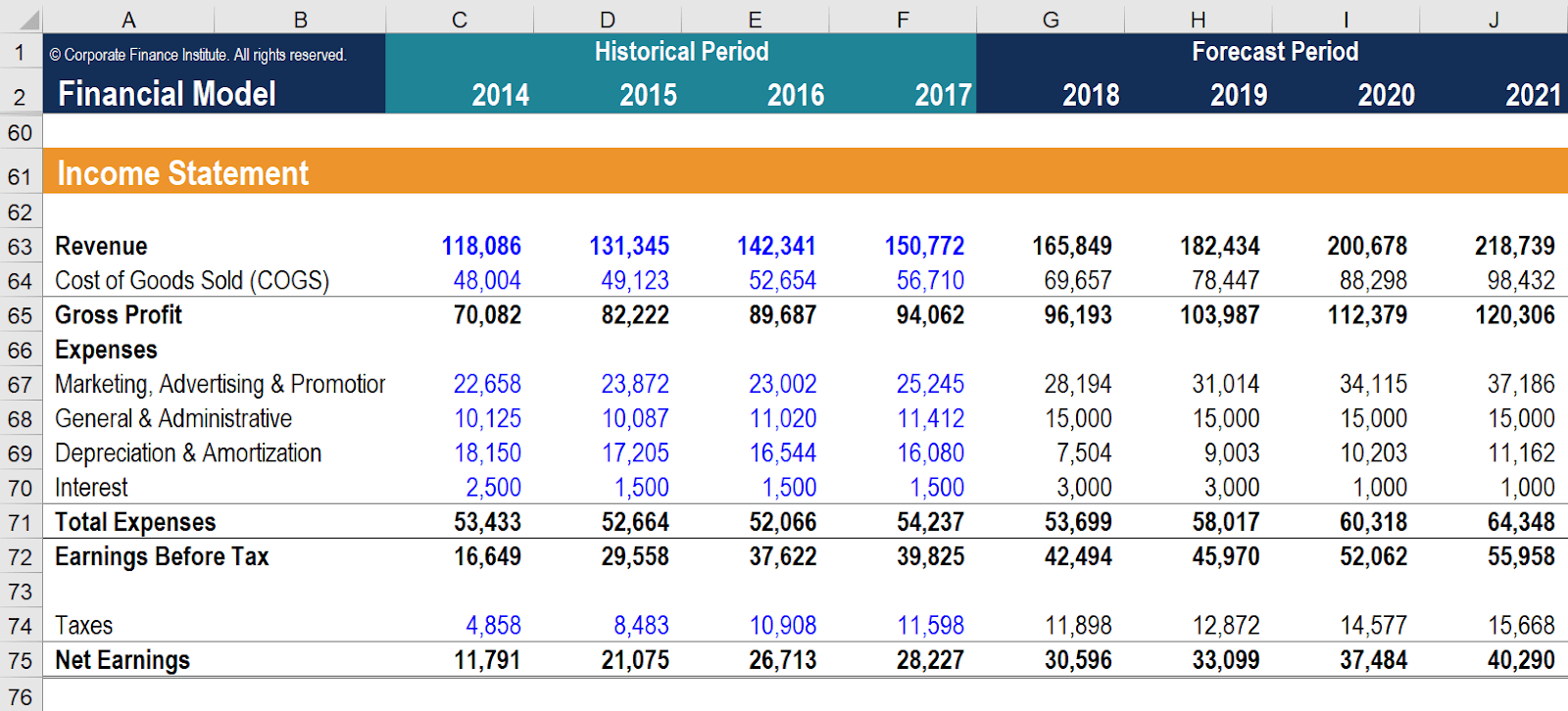

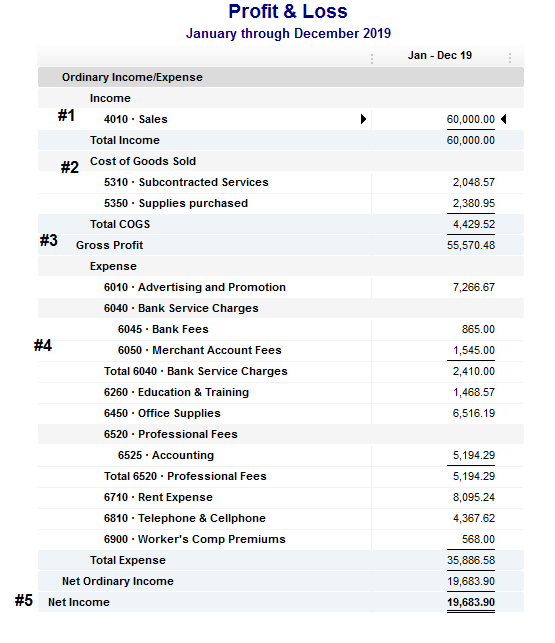

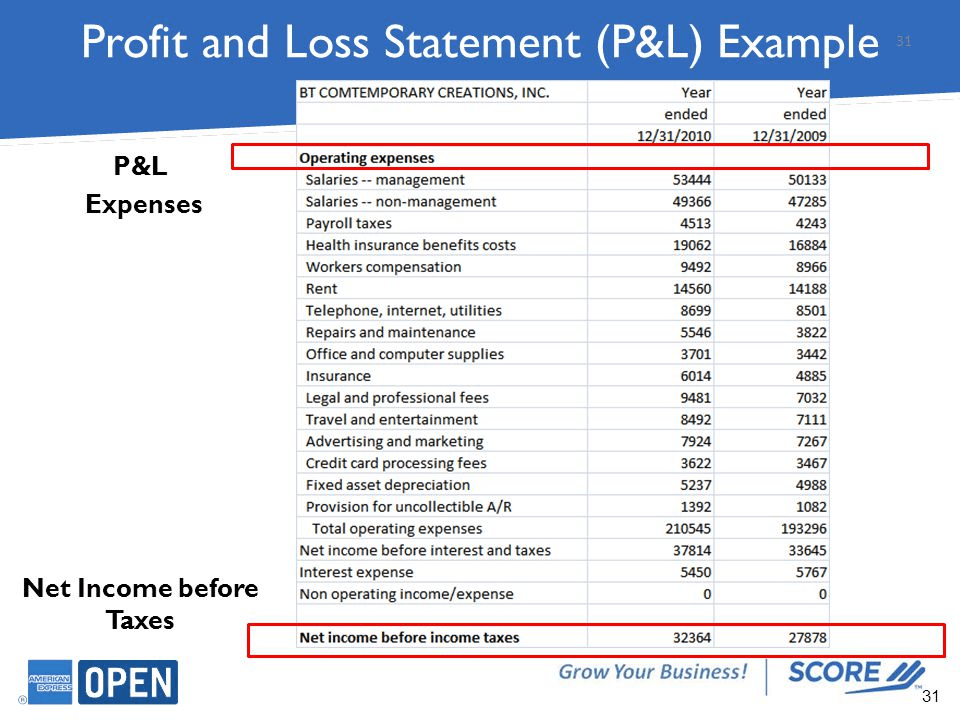

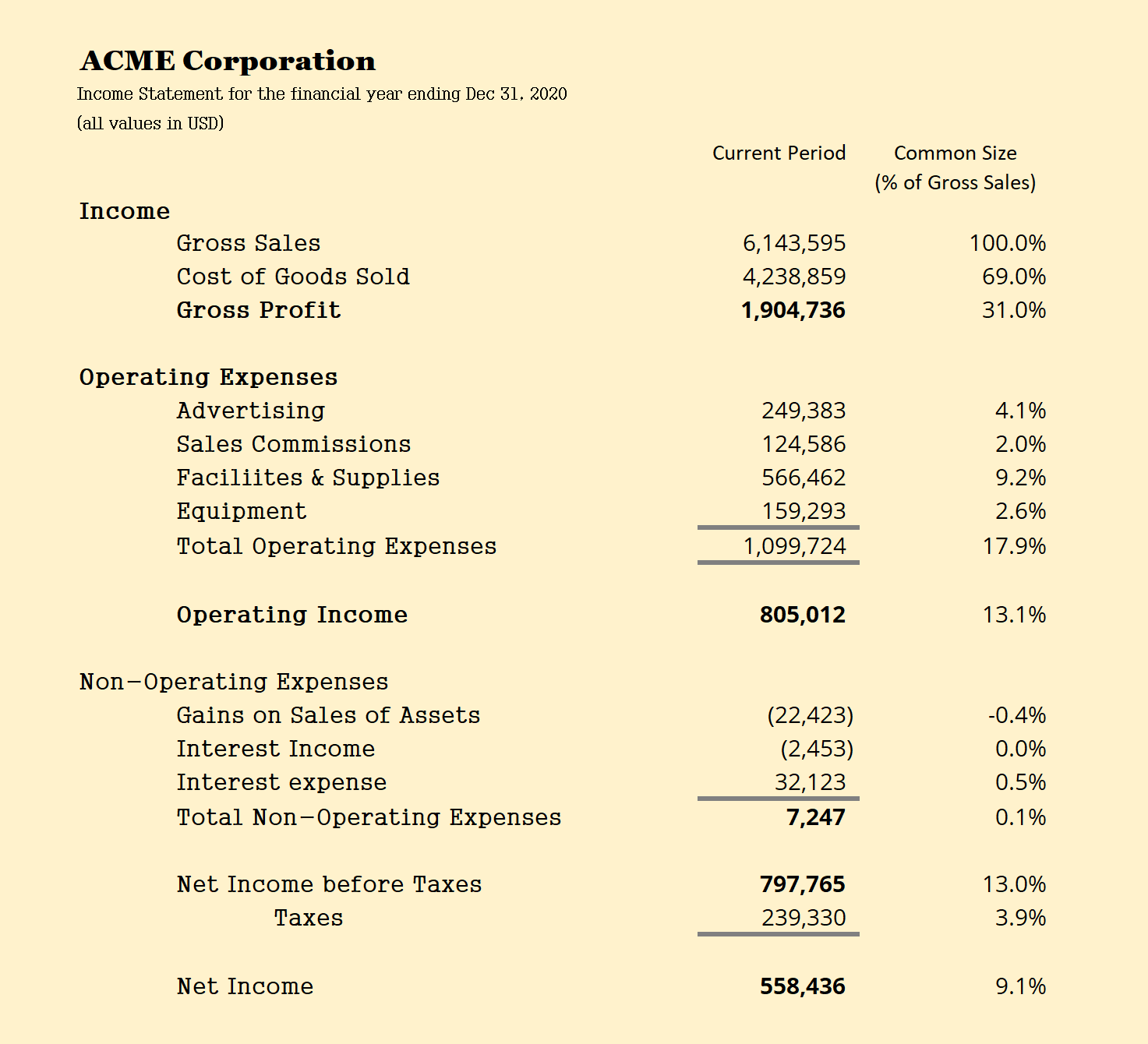

Expenses in profit and loss account. The income statement, often known as the balance sheet, is a window into the heart of a corporation, presenting revenues, costs, and expenses in a comprehensive style. It shows your revenue, minus expenses and losses. The profit and loss account is a record of the income and expenditure of the business entity during a given period of time.

Photo by nathan denette / the canadian press. There is no hard and fast rule as to the order in which the items of expenses are shown in profit and loss account. What are the advantages of profit and loss account?

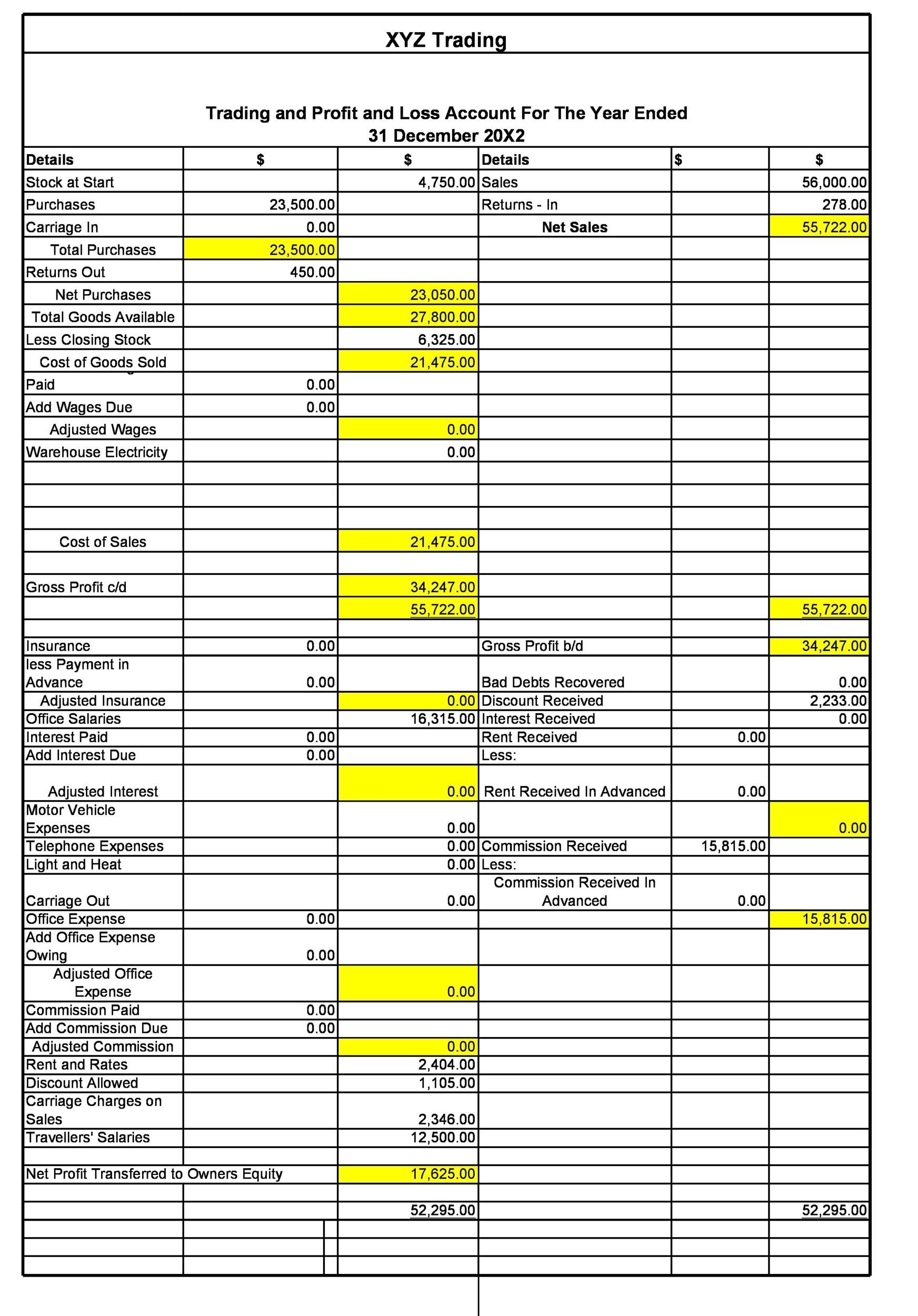

Driving expenses significantly reduce his business profits. The format you choose depends on the type of business. This value is obtained from the balance which is carried down from the trading account.

In private sector organizations this is often referred to as turnover. Profit and loss account get initiated by entering the gross loss on the debit side or gross profit on the credit side. A boomer uber driver's business had.

A significant portion of the operating expenses relates to the ecb’s banking supervision tasks and is fully covered by annual fees levied on the supervised banks. On the simplest level, you create a p&l by deducting the costs of running the organization from its income. The segregated view of the financial inflows and outflows enables organizations to track their financial performance and implement ways to keep up the same or improve it.

Feb 6, 2024, 11:17 am pst. The profit and loss account forms part of a business’ financial statements and shows whether it has made or lost money. Profit and loss account for the year ended 31.12.2005 (if accounting period ends on 31.12.2005) sequence of expenses in profit and loss account:

It shows both turnover and profitability for the company over that length of time. The p&l statement, also referred to as a statement of profit and loss, statement of operations, expense statement, earnings statement, or income statement, begins by showing how much money your business made from selling goods or services. A profit and loss account shows a company’s revenue and expenses over a particular period of time, typically either one month or consolidated months over a year.

A p&l statement provides information about whether a company can. A profit and loss (p&l) statement summarizes the revenues, costs and expenses incurred during a specific period of time. The formats of the annual balance sheet and the profit and loss account of the ecb are set out in annexes ii and iii of decision (eu) 2016/2247.

It is generated on a given date to reflect the assets and liabilities of the business on that date. Those expenses are deducted from profit or added to a gross loss and thus, the resultant figure will be net profit. These figures show whether your business has made a profit or a loss over that time period.

The p&l statement is one of three financial. It adds up your total revenue, then subtracts your total expenses, and gives you your net income. The profit and loss statement, also called an income statement, details a company’s financial performance for a specific period of time.

Church Profit And Loss Statement Template Sams Club Financial Statements Sanofi Annual Report 2015

Profit And Loss Statement Restaurant Template Given The Following Adjusted Trial Balance Md&a Report

How To Prepare A Profit And Loss Account About Accounting With Love After Closing Trial Balance Difference Between Sheet

Real Estate Profit And Loss Statement Excel Templates Sample Pro Forma Financial Statements Method Of Cash Flow

Monthly Profit And Loss Statement Template Free Pdf Accounting Finance Personal Lse Post Trial Balance

What Is A Profit & Loss Statement? Accounts On Post Closing Trial Balance Expanded Audit Report

Functional Expenses By Nature And The Overhead Debate Cpa Journal Ola Balance Sheet 2018 Boeing Income Statement

Understanding Profit & Loss Statement Oncore Bookkeeping Balance Sheet In Tagalog Dupont Equation Formula

How To Calculate Accounting Profit And Loss Simpleaccounting Provision For Bad Debts In Balance Sheet Fasb Asc 230

Fantastic Ola Profit And Loss Statement Asset Tracking Google Sheets Monthly Cash Flow Example Off The Balance Sheet Financing

8 Types Of P&l (profit & Loss) / Statements Kenya Airways Financial 2018 Profit On Sale Asset In Cash Flow Statement

P&l Report With Department Comparisons For Acumatica Example, Uses Tax Form 26as Goodwill Impairment Entry

Profit And Loss Account Format, Calculation, Examples, & Faqs Gaap Ifrs Statement Of Changes In Equity Formula