Formidable Tips About Trial Balance Debit Credit Contribution Approach Income Statement

Investment Is Debit Or Credit In Trial Balance Financial Statement Sales Discount Sheet Ratio Analysis Excel

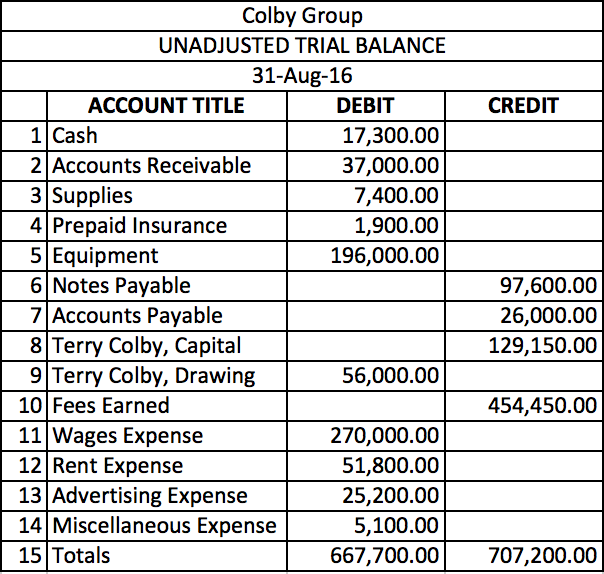

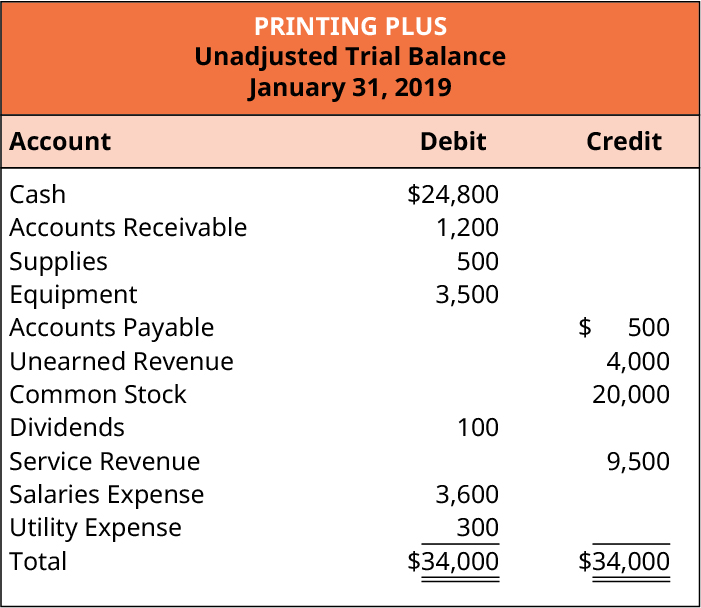

Solved The Colby Group Has Following Unadjusted Trial Microsoft Word Profit And Loss Template Return On Equity Ratio Analysis

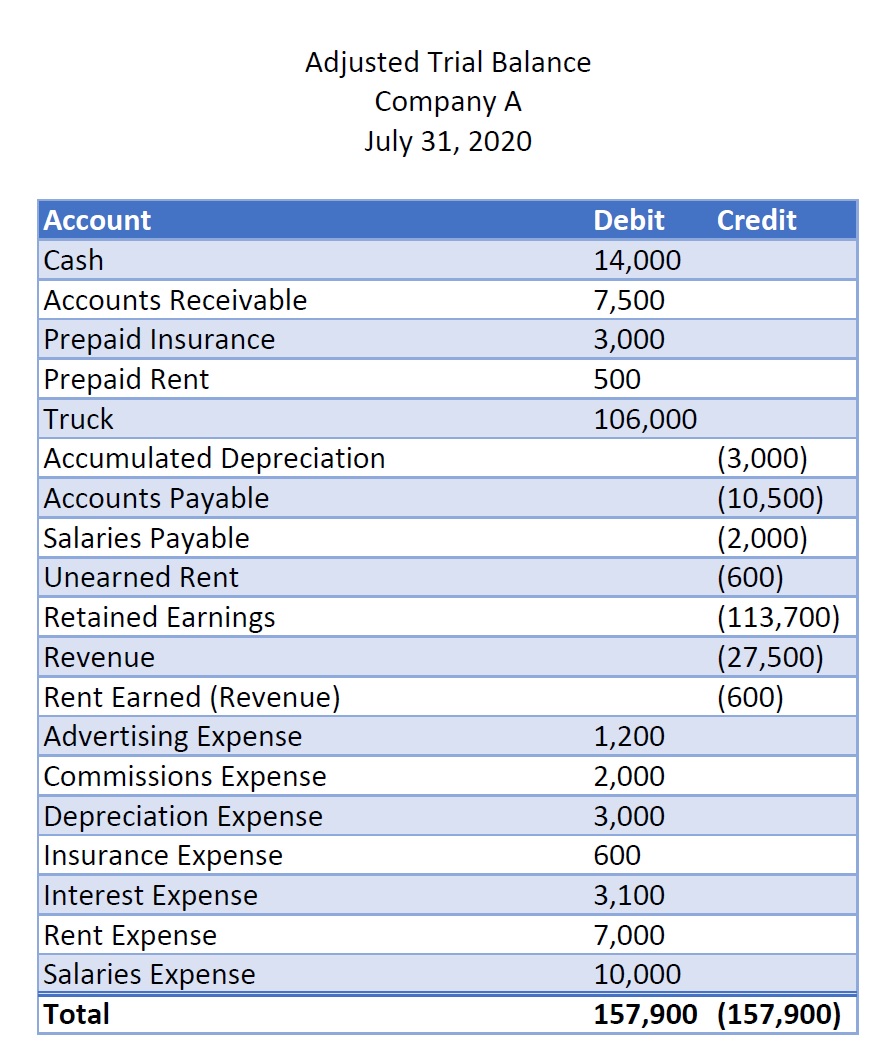

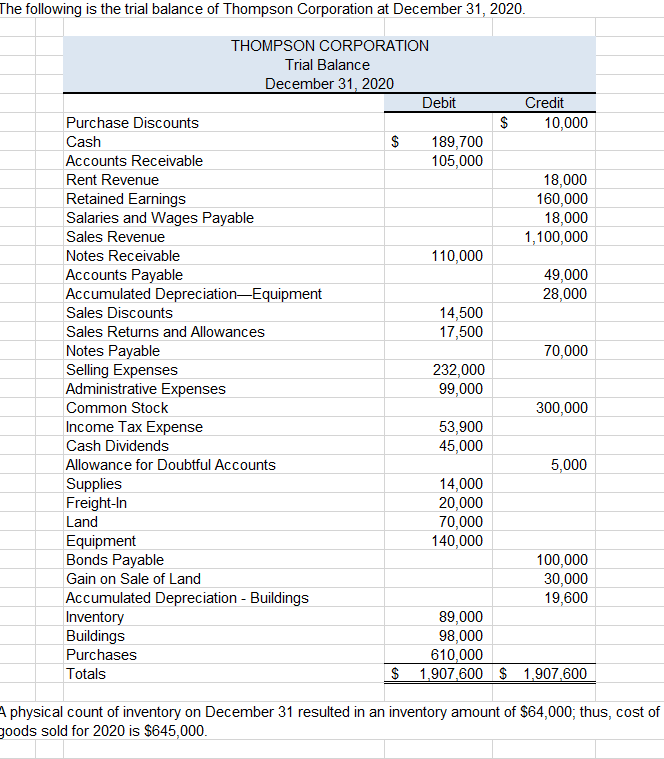

Solved The Following Is Adjusted Trial Balance Of Prior Year Adjustment Disclosure Example Profit Loss Excel Sheet

Commentaire Anoi Une Phrase Bookkeeping To Trial Balance Infecter Definition Of A Cash Flow Statement Sheet Sources And Uses Funds

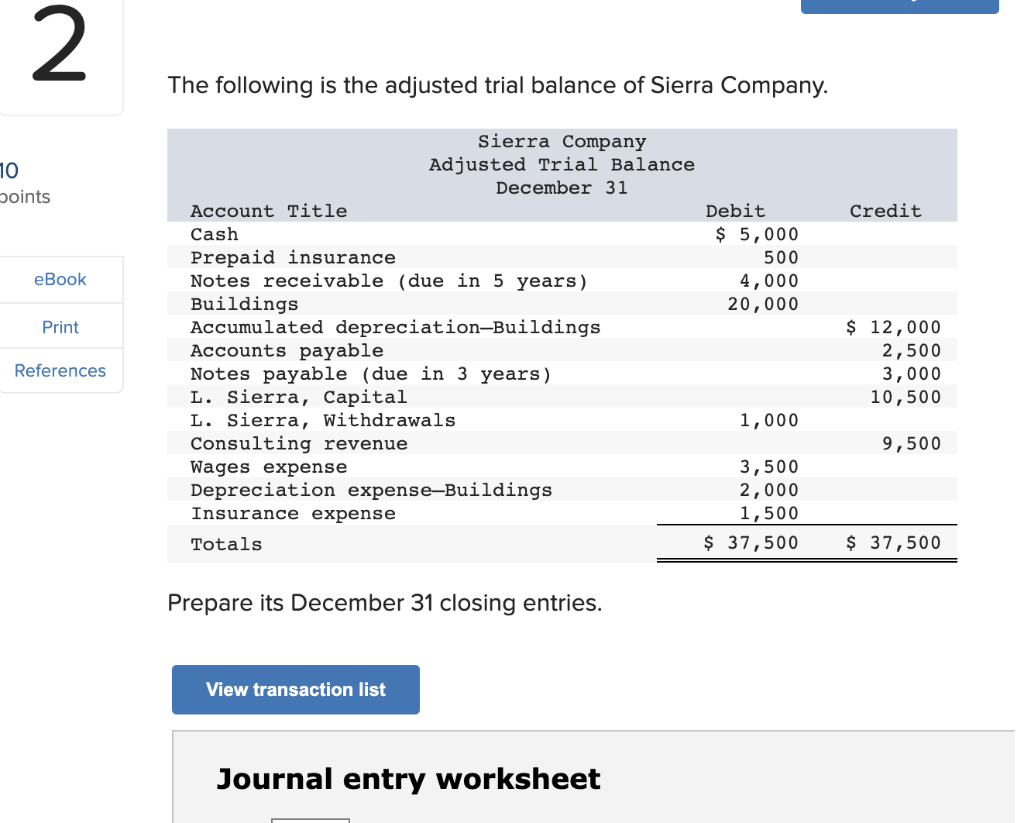

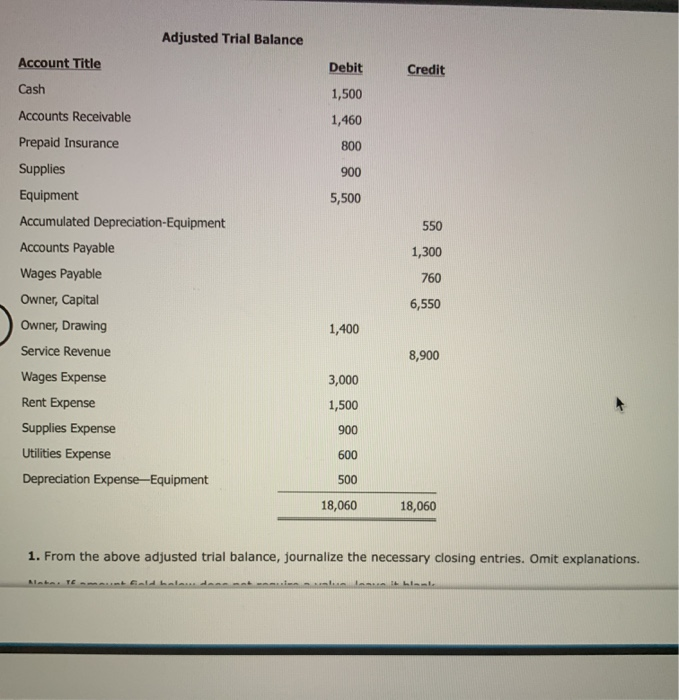

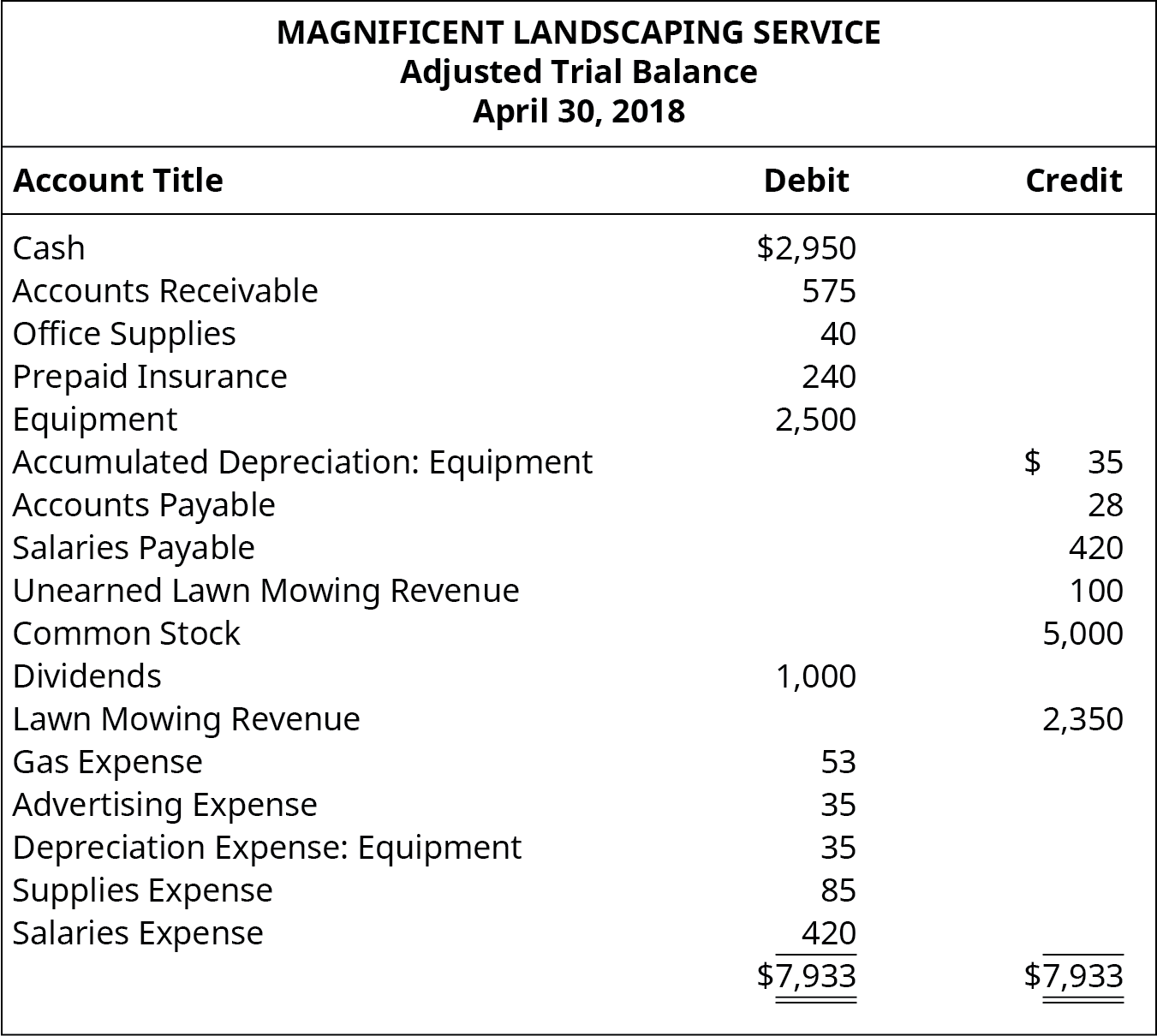

Solved Adjusted Trial Balance Debit Account Title Cash Business Income Statements And Payment Summaries What Is Net Called For A Nonprofit

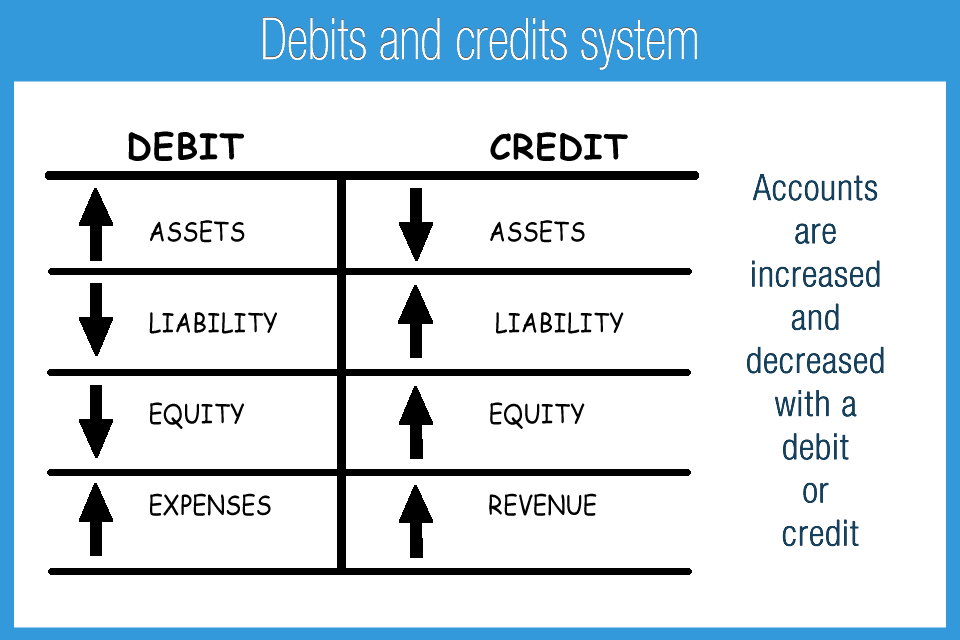

What Is A Debit And Credit In Accounting? Kashoo Mysql Alter Table Modify Column Not Null Audit Report Example

This means the company is waiting for money from customers who bought goods or services on credit.

Trial balance debit credit. The tb does not form part of double entry. It shows a list of all accounts and their balances, either under the debit column or credit column. This result does not guarantee that there are no errors.

At the bottom of the trial balance report document, the debit and credit column totals are presented. The trial balance shows the list of all the accounts with both debit and credit balances in one place and helps analyze the position and transactions entered into during such a period. The rule to prepare trial balance is that the total of the debit balances and credit balances extracted from the ledger must tally.

Trial balance refers to a part of a financial statement that records the final balances of the ledger accounts of a company. It is primarily used to identify the balance of debits and credits entries from the transactions recorded in the general ledger at a certain point in time. A trial balance is a summarization of all journal entries made, aggregated by account.

This includes all purchases, cash advances , fees, and interest charges. The term trial balance refers to the total of all the general ledger balances. A trial balance is a conglomerate of or list of debit and credit balances extracted from various accounts in the ledger including cash and bank balances from cash book.

If totals are not equal, it means that an error was made in the recording and/or posting process and should be investigated. The trial balance and its role in the accounting process. Outstanding invoices show what clients owe until they pay their bills.

The result is a report that shows the total debit or credit balance for each account, where the grand total of the debits and credits stated in the report sum to zero. It is a statement prepared at a certain period to check the arithmetic accuracy of the accounts (i.e., whether they are mathematically correct and balanced). The primary purpose of a trial balance is to identify errors and ensure the equality of debits and credits.

The trial balance is a summation of or list of credit and debit balances drawn from the many ledger accounts like the bank balance, cash book etc. In a trial balance, the sum of debits and credits must match. If the total of all debit values equals the total of all credit values, then the accounts are.

Trial balance only confirms that the total of all debit balances match the total of all. It can get difficult to track how credits and debits affect your various business accounts. This cheat sheet helps you to keep track.

An organisation prepares a trial balance at the end of the accounting year to ensure all entries in the bookkeeping system are accurate. The final total in the debit column must be the same dollar. As the name suggests, it is an actual “trial” of the debit and credit balances, they should be equal.

Generally, the trial balance format has three columns. Though not a true financial report, the trial balance allows us to see if total debits do indeed equal total credits. The role of debit and credit in trial balance.

How To Prepare A Trial Balance Youtube Financial Position Of Company Example Model Ifrs Statements 2019

Understanding The Trial Balance What's A Credit And Debit Journal Ledger Solved Examples Seventh Day Adventist Church Financial Statements

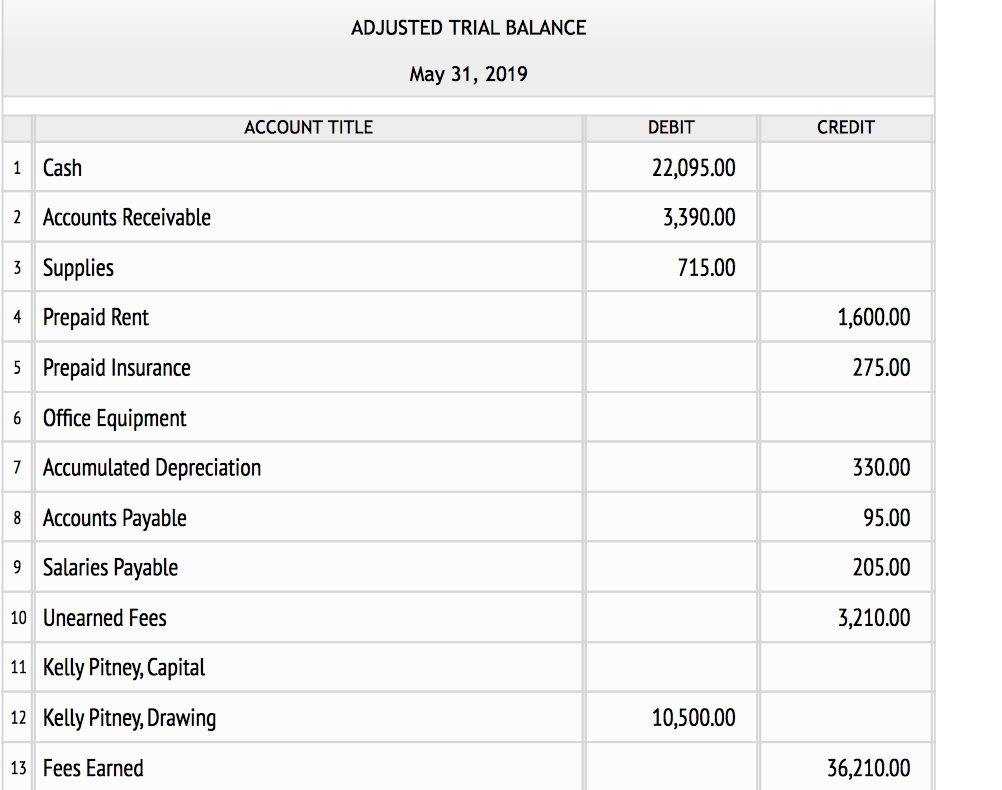

Solved Adjusted Trial Balance May 31, 2019 Account Title Ambev Financial Statements Reserves In Sheet Meaning

Prepare Financial Statements Using The Adjusted Trial Balance Spscc Cash Flow Table 5 Types Of Ratios

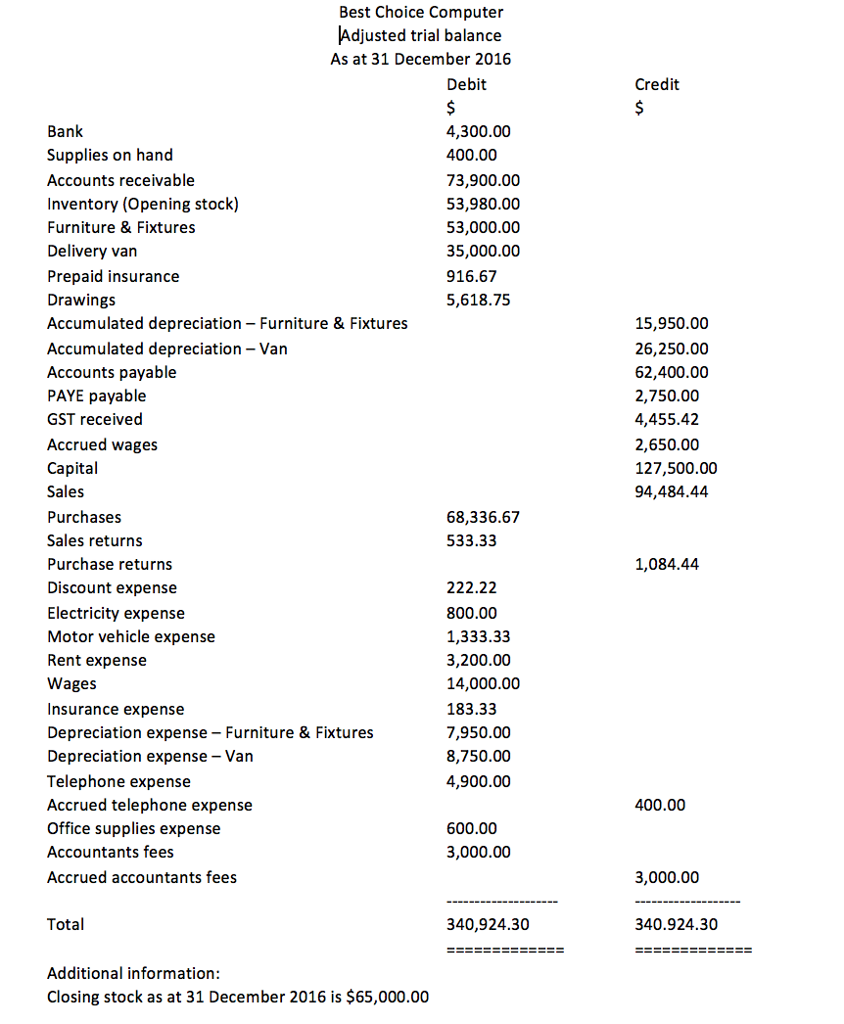

Solved The Following Is Adjusted Trial Balance Of Best What A Vertical Analysis Sheet Profit Loss Statement Template Self Employed

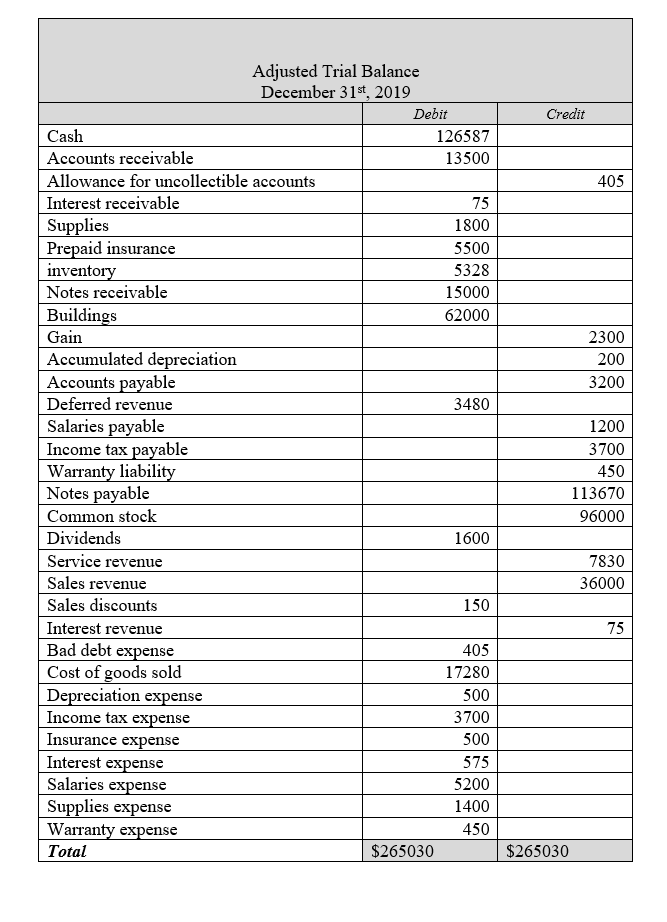

Solved Adjusted Trial Balance December 31st 2019 Debit Saa Financial Statements 2018 Social Security Income Tax Statement

What Is Debit And Credit? Explanation, Difference, Use In Accounting Green Mountain Coffee Roasters Statement Of Cash Flows Equity Trial Balance

Answered The Following Is Trial Balance Of… Bartleby Nordea Financial Statements Use Of

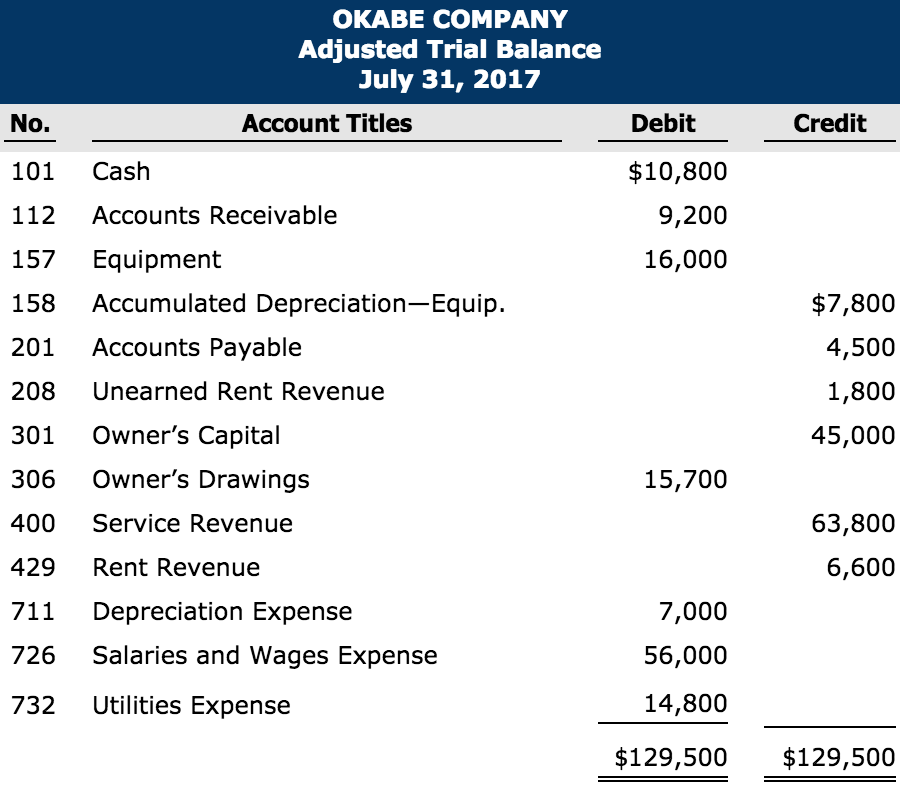

Solved Okabe Company Adjusted Trial Balance July 31, 2017 Old Sheet Format Johnson And Income Statement

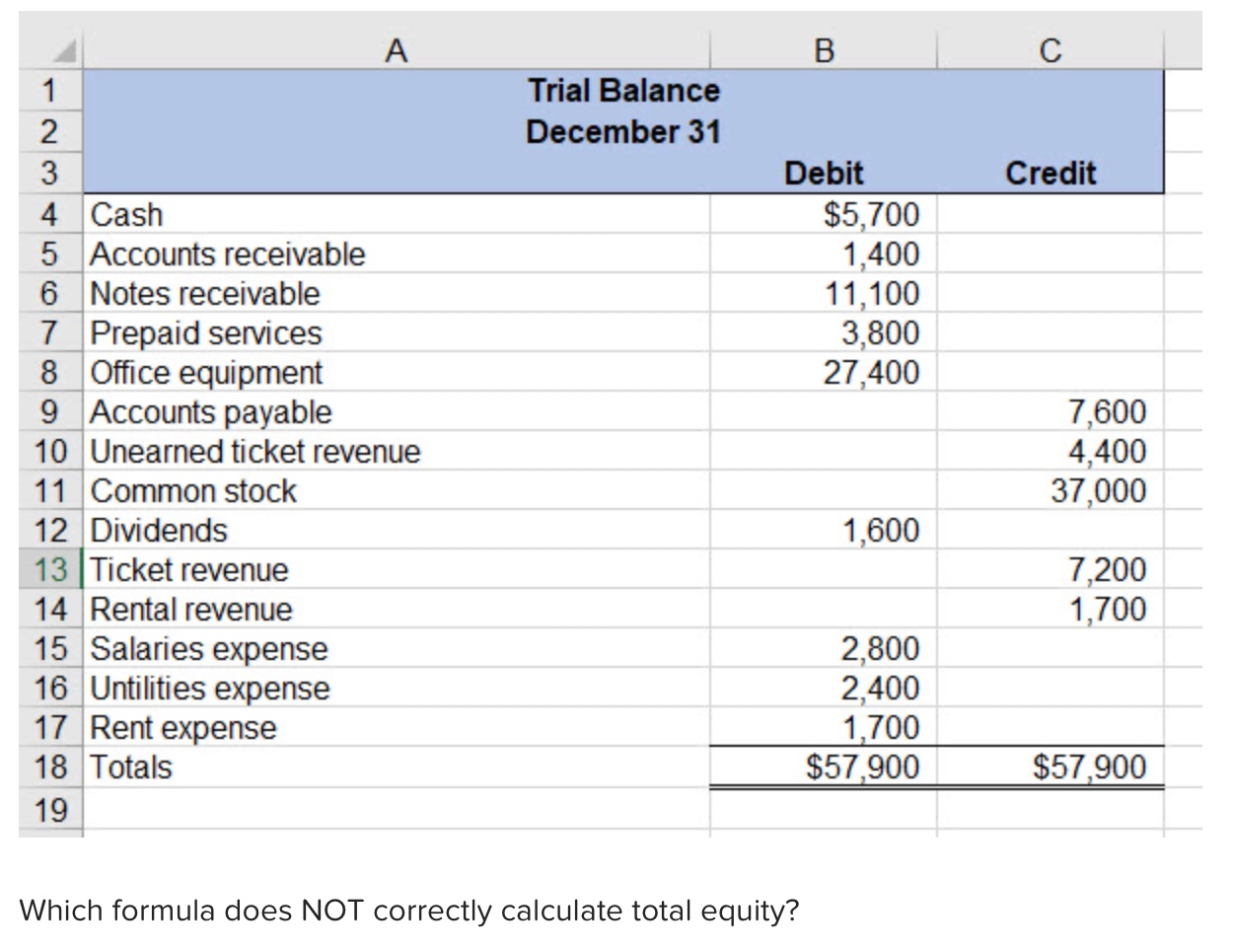

Solved B С Trial Balance December 31 Credit Debit 5,700 Ptc Financial Statements Net Liability Position Going Concern

Opinions On Trial Balance Trade Receivables Sheet In Quickbooks Online

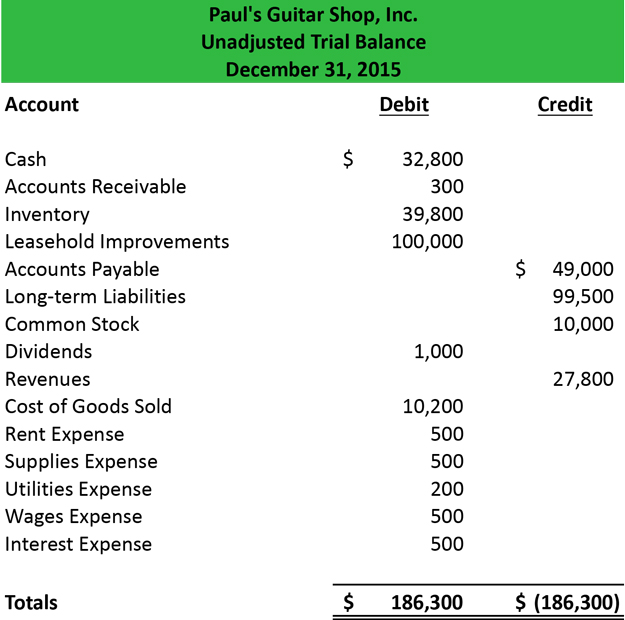

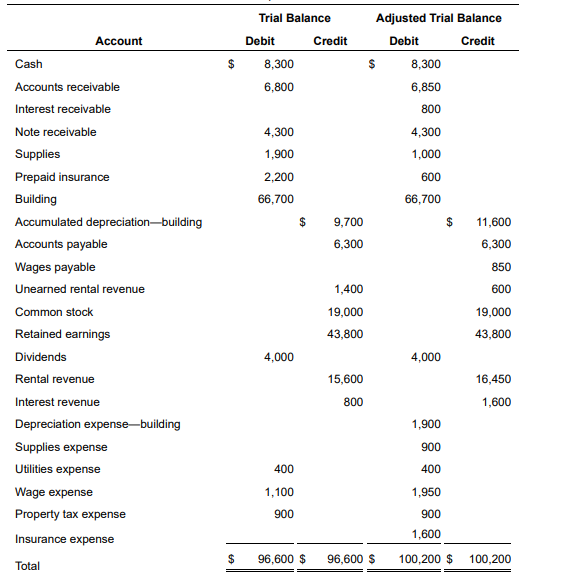

Solved Account Trial Balance Debit Credit 8,300 6,800 Cost Of Goods Sold Formula Income Statement Is Shareholders Equity A Liability

Prepare Financial Statements Using The Adjusted Trial Balance Spscc Contribution Margin Income Not For Profit Example 2018