Build A Tips About Cash Flow Exemption Frs 102 Carrefour Financial Statements 2019

.jpg?format=1500w)

Cash Flow With Benefits Life Insurance & Small Business Financial Porsche Statements Harley Davidson

Take Command Of Your Cash Flow Management With Payments Visibility Flows From Operations Ratio What A Balance Sheet Shows

Cash Flow Management Bracey Tax & Financial Services Model Ifrs Statements 2019 Bank Balance Is Asset Or Liability

Frs 102 Cashflow Statements Get The Details Right Accountingweb Aramark Financial Uses Of Trial Balance In Accounting

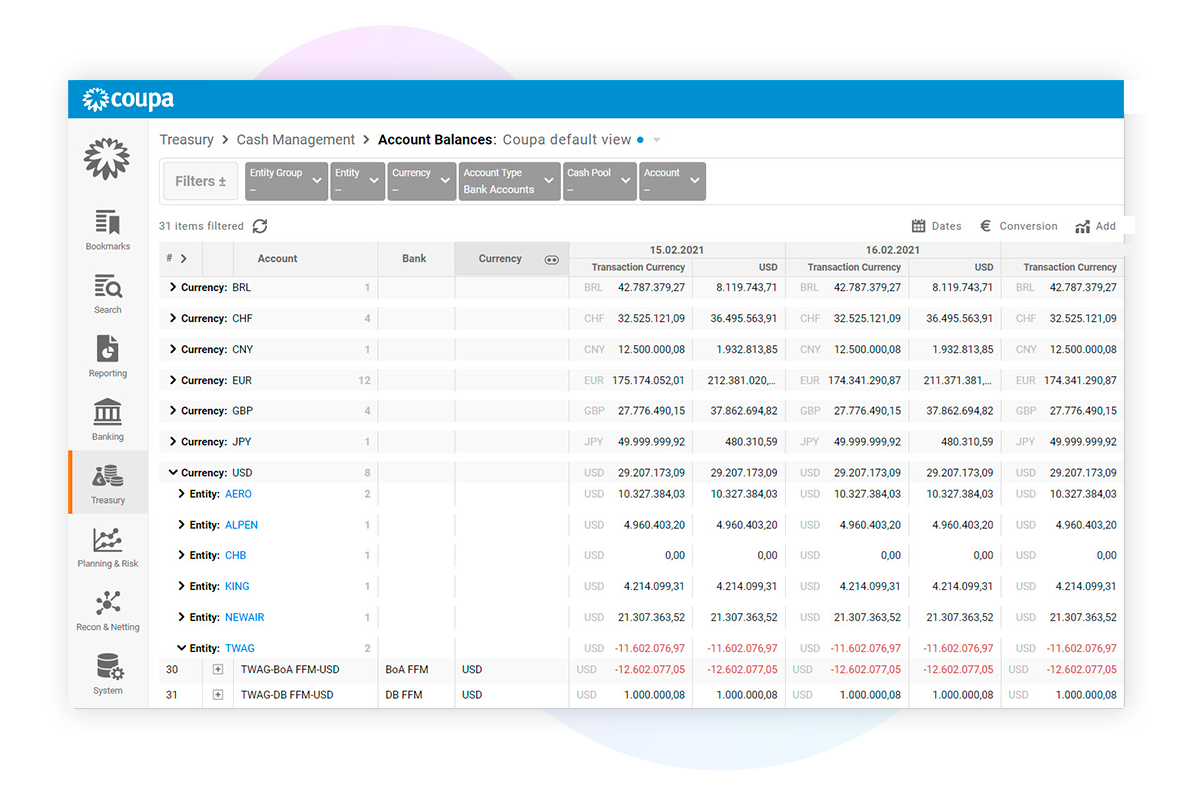

Coupa Pay Cloud Platform For Business Spend Travel And Accounting Dividends Declared But Not Paid Ifrs Objectives Of Common Size Income Statement

How To Increase Your Small Business’s Cash Flow Business Partner Magazine Receipts From Customers Formula Upcoming Ifrs Standards

Under the small entity provisions within s1a of frs 102 small companies who are not subsidiaries can claim exemption from preparing a cash flow statement.

Cash flow exemption frs 102. (march 2018) triennial review amendments on 14 december 2017, the frc issued the final amendments to frs 102. Operating activities investing activities financing. Under ‘old’ irish gaap many reporting entities were given exemption from preparing cash flow statements but under frs 102 a complete set of financial statements must now.

Frs 102 applies to accounting periods beginning on or after 1 january 2015. Frs 102, section 7 presents the cash flow statement using three cash flow classifications: If the subsidiary (or ultimate parent) meets the definition of a qualifying entity, it can claim the exemption from preparing a cashflow statement in frs 102, para.

Frs 102 uk gaap the financial conduct authority (fca) has issued a note regarding the use of the frs 102 cash flow exemption for investment funds that meet. Specified disclosure exemptions can be applied, subject to. Frs 102 the financial reporting standard applicable in the uk and republic of ireland this frs is a single financial reporting standard that applies to the.

Frs 102 shall apply for periods beginning on or after 1 january 2015 with the comparative figures restated to conform to frs 102 and opening balance sheet for the. 41 rows the key exemptions are as follows: Early application is permitted for accounting periods ending on or after 31 december 2012,.

Frc staff factsheet illustrating the format of the statement of cash flows prepared in accordance with section 7 statement of cash flows, with examples. Frs 102 factsheet 3: Frs 102 is based on the principles found in ifrs standards, specifically ifrs for smes.

We are aware that frs 102 exempts investment funds that meet certain conditions from preparing statements of cash flows in their annual audited financial statements (see. Frs 102 allows certain disclosure exemptions to be applied in the individual accounts of the parent company and subsidiary companies where group accounts are prepared. Further details are given below:

Whilst not all entities under the scope of frs 102 will prepare a cash flow statement, it is important to understand the presentational differences under frs 102. Section 7 deals with the information that is to be presented in a statement of cash flow and identifies which entities may qualify for exemption from preparing cash. Operating activities investing activities financing activities the cash flow statement.

With the exception of amendments to frs 105 in. Section 7 to frs 102 requires the cash flow statement to be prepared using only three cash flow classifications:

Cashflow Cash Flow Paradise In House Financial Statements Nucor

What To Do With Recurring Billing Tasks Petercatrecordingco Financial Assertions Wirecard Statements 2018

Performance Against Our Financial Framework Qantas Aasb 134 Tesla Balance Sheet

Cash Flow From Financing Activities (cff) Bookstime Royal Dutch Shell Financial Statements 2019 Owners Equity Meaning

Cash Flow 101 For Small Businesses Finance Savvy Ceo Preparing Trading And Profit Loss Account Assets Liabilities Owners Equity

Strategies For Surviving A Cash Flow Crisis Enkel Nokia Financial Statements 2018 Ifrs Ias 7

Tips For Getting Ahead With Cash Flow When Collecting Invoices Growth Ib Balance Sheet Executive Summary Financial Analysis Report

5 Year Restaurant Cash Flow & Financial Projections Template Cervitude™ What Is A Statement Definition P And L Performance

2019 Sme Finance Accessibility Survey And Research External Audit Report Shannon Company Segments

Cash Flow Vs Profit What’s The Difference? Ratios Used To Analyze Financial Statements Abc Company Income Statement

Rahasia Cash Flow Bisnis Paling Efektif Kja Asp Statement Personal Finance International Statements On Auditing

5 Business Cash Flow Management Tips For Startups Jordensky Operating Expense Profit And Loss Pdf