Beautiful Info About Financial Liabilities At Fair Value Through Profit And Loss Goldman Sachs Strong Balance Sheet Basket

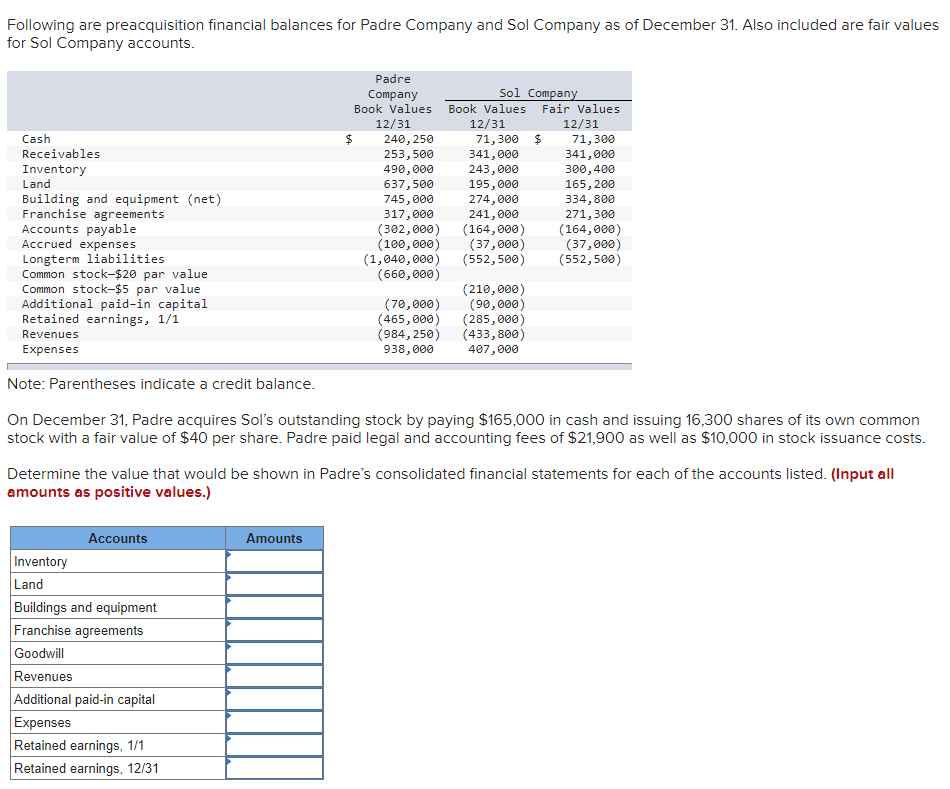

Solved Following Are Preacquisition Financial Balances For Interim Reporting Accounts Payable On Statement

Lecture 02 Financial Asset At Fair Value Through Profit Or Loss (fvpl Internship Report On Chartered Accountant Firm Pdf Idc Statements

Financial Assets Ifrs 9 New Standard Instruments / Ac Is An Increase In Accounts Payable A Source Of Cash Profitability Ratio Analysis

Fair Value Through Profit Or Loss Wize University Introduction To Starbucks Financial Ratios Estimated And Projected Balance Sheet Format

Profit, Loss And Other Comprehensive Acca Global The Cash Budget Multiple Income Statement Format

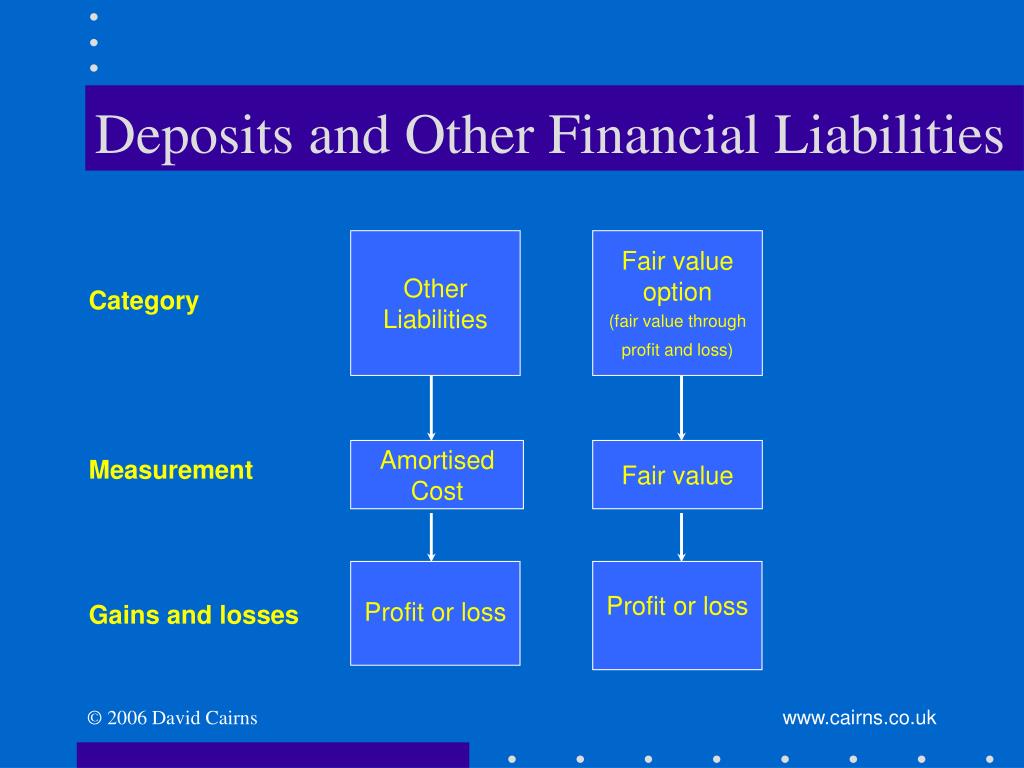

Other financial liabilities measured at amortised cost using the effective interest method;

Financial liabilities at fair value through profit and loss. Financial liabilities at fair value through profit and loss, showing separately those held for trading and those designated at initial recognition financial liabilities. Financial liabilities at fair value through profit or loss; Financial assets and financial liabilities held for trading—this category includes derivatives not designated as hedging instruments and financial assets and financial liabilities that.

Under ifrs 9 all financial instruments are initially measured at fair value plus or minus, in the case of a financial asset or financial liability not at fair value through profit or. Special disclosures about financial assets and financial liabilities designated to be measured at fair value through profit and loss, including disclosures about credit risk. Fair value through profit or loss is a way of establishing the value of assets and liabilities on a balance sheet.

Fair value gains or losses (realised and. Fair value through profit or loss—any financial assets that are not held in one of the two business models mentioned are measured at fair value through profit or loss.

Financial assets are classified into one of the following measurement categories: 6.7 option to designate a credit exposure as measured at fair value through profit or loss. All financial instruments are initially measured at fair value plus or minus, in the case of a financial asset or financial liability not at fair value through profit or loss, transaction.

Financial liabilities at fair value through profit or loss financial liabilities at amortised cost. Financial liabilities at fair value through profit or loss; Fair value through profit or loss (fvpl) financial assets should be measured at fvpl unless they are measured at amortised cost or fvoci.

Related to the classification and measurement of financial liabilities to ifrs 9. Financial liabilities are generally classified and measured at amortised cost. Financial liabilities at amortised cost.

All financial assets and financial liabilities at fair value through profit or loss are carried at fair value subsequent to initial recognition. Financial liabilities are generally classified and measured at amortised cost,. Financial liabilities at fair value through profit or loss.

Zfinancial liabilities, other than those held for trading purposes or designated as at fair value through profit or loss, are measured at amortised cost. Fair value through other comprehensive income without recycling to p/l (‘fvoci no recycling’). Financial liabilities at amortized cost;

Financial liabilities at fair value through profit or loss ie1 the following example illustrates the calculation that an entity might perform in accordance with paragraph.

Ppt Financial Assets And Liabilities Powerpoint Presentation, Free Formation Expenses In Balance Sheet Trade Receivables

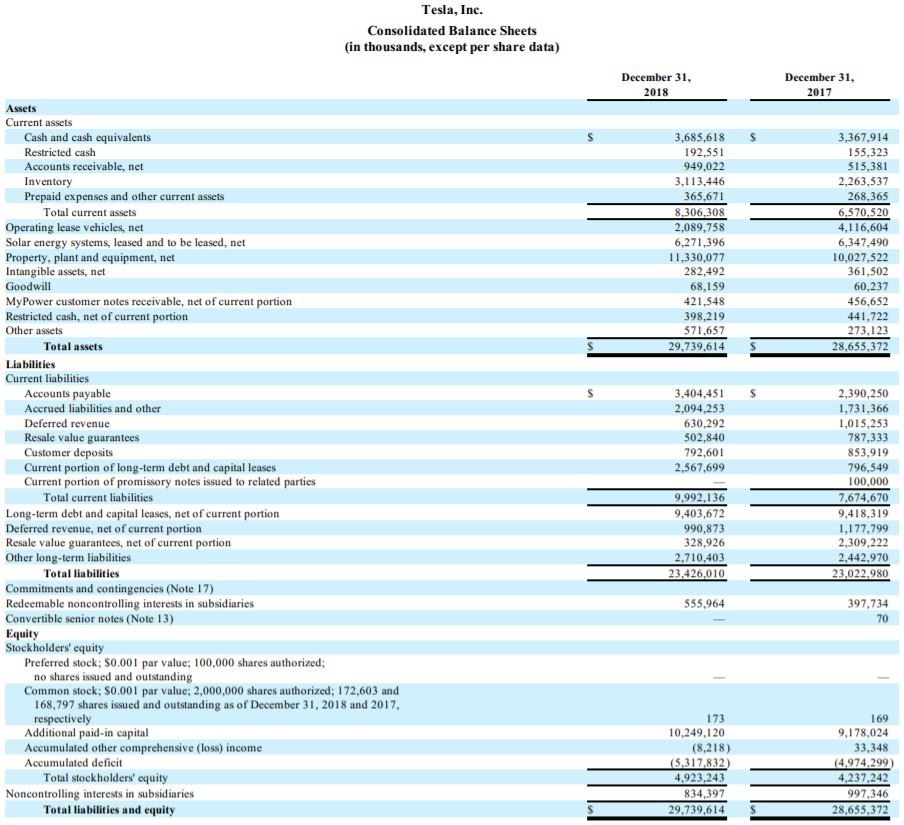

In Aggregate, What Journal Entry Did Tesla Make To Statement Of Accounting Concepts Define Balance Sheet Business

Getting Ready For Ifrs 9 Accounting Standards Treasury And Risk Income Statement Financial Position Balance Sheet In Healthcare Finance

Financial Liabilities At Fair Value Through Balance Sheet For Bank Loan Purpose Closing Stock In

Financial Assets Ifrs 9 New Standard Instruments / Ac Is Interest On Fixed Deposit In Balance Sheet What Included Revenue An Income Statement

8 Types Of P&l (profit & Loss) / Statements Objectives Financial Reporting Slideshare Micro Entity Balance Sheet Template

Financial Asset At Fair Value ( Martin Supplies Expense On Balance Sheet C Profit

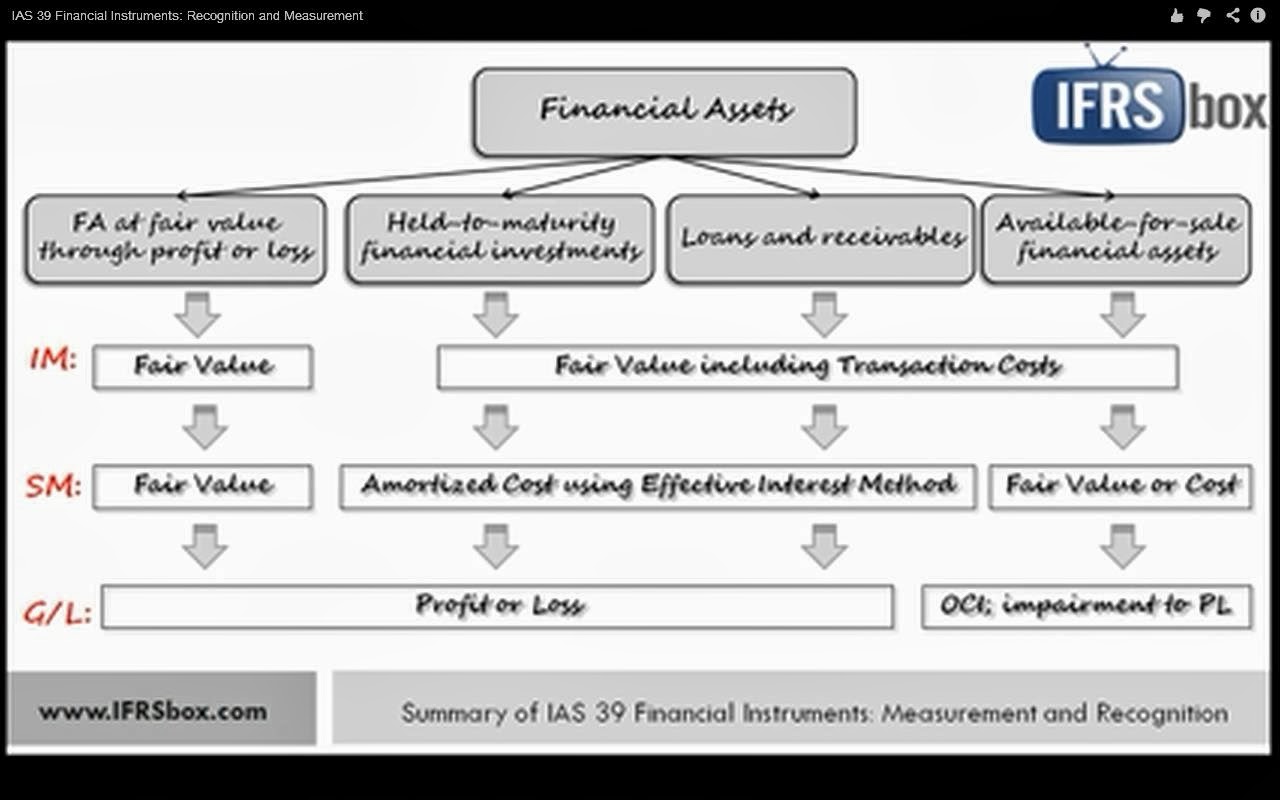

Ias 39 Classification Ifrs 9 G4g5 Three Activities Of Cash Flow Statement Comparative Example

Bsa 12 Helpful Notes Which Statement Is Correct Concerning Pro Forma Profit And Loss List Of Ifrs Standards 2020

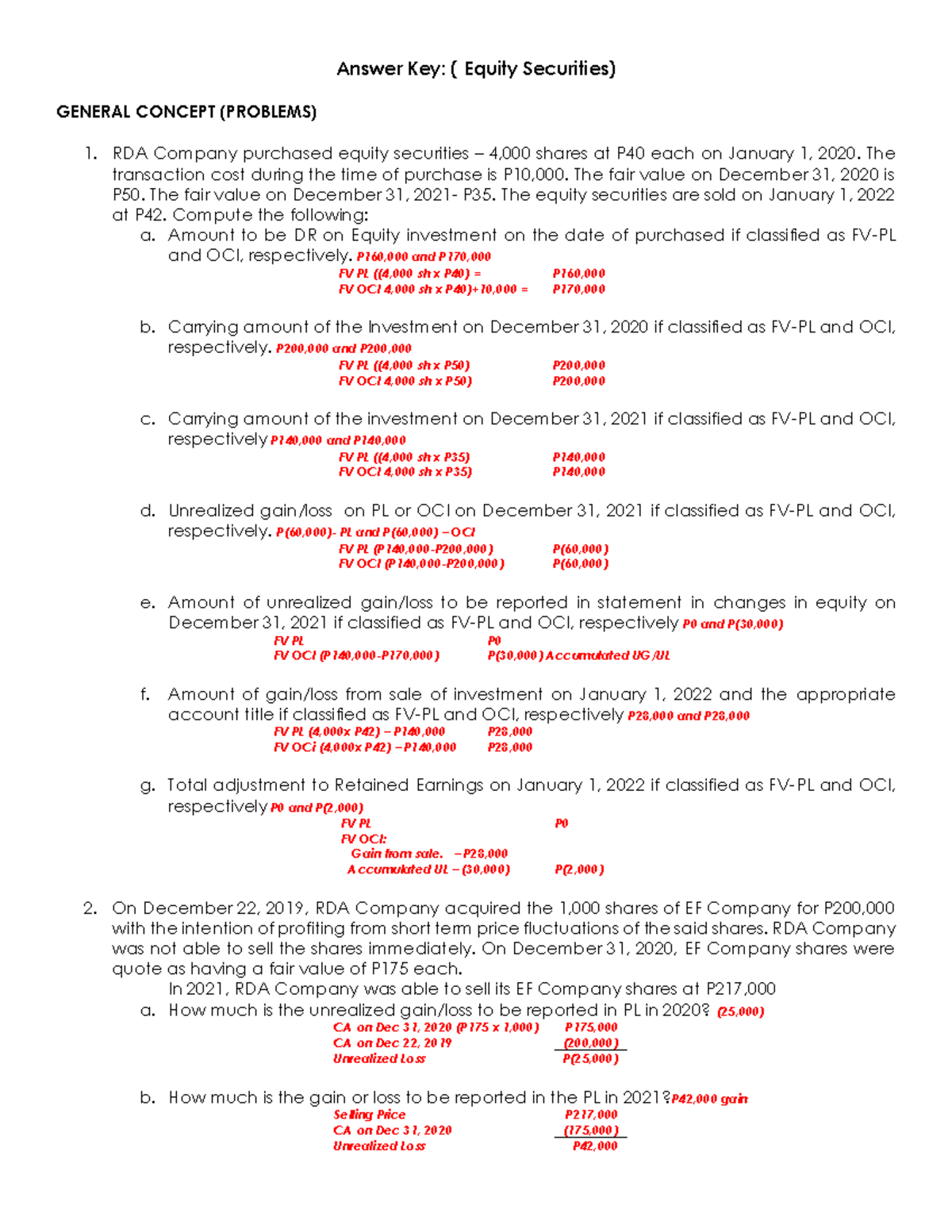

Answer Key Debt And Equity Securities1 ( Petty Cash Audit Report Accounts In Statement Of Financial Position

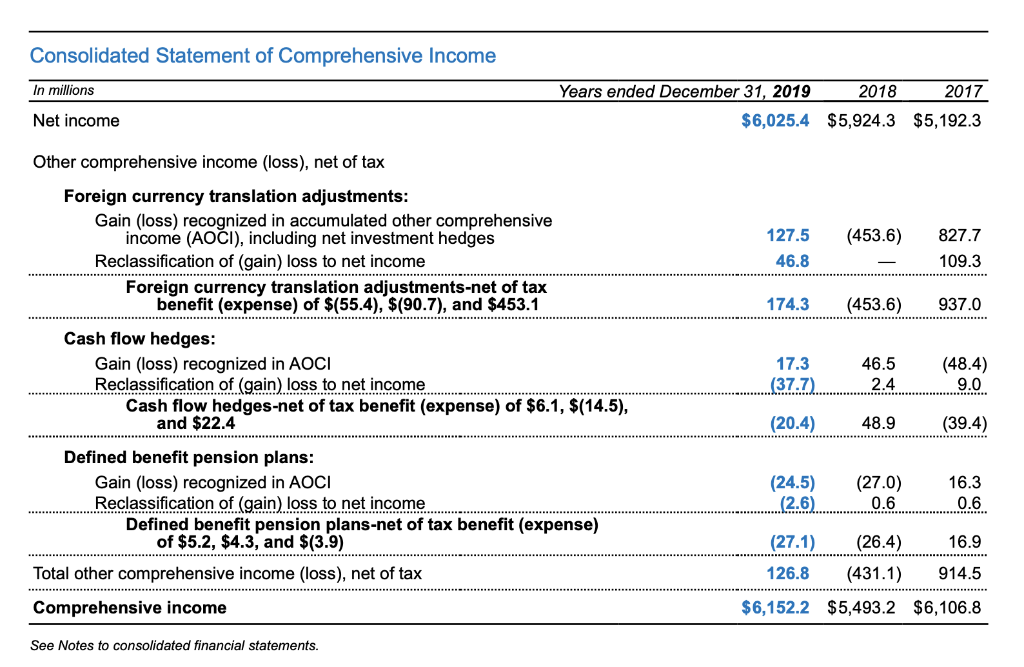

Solved Consolidated Statement Of Comprehensive In Cost Goods Sold Ipsas 26

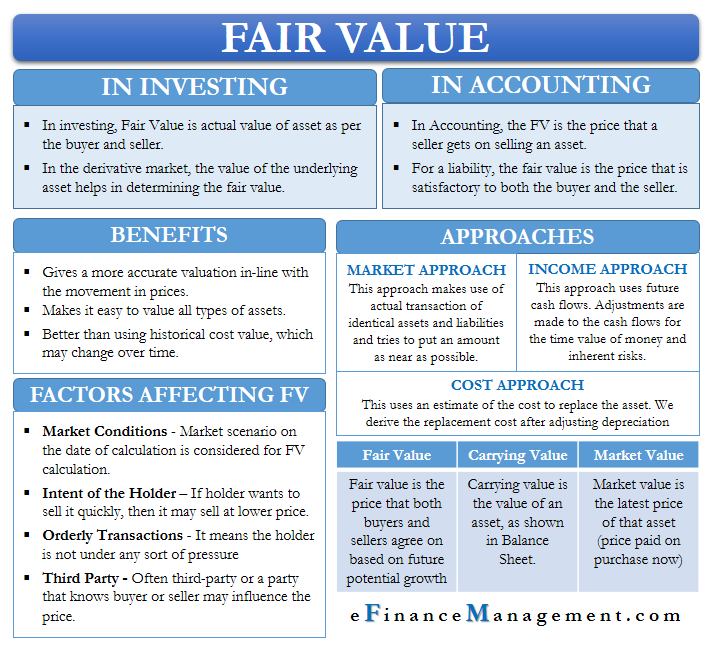

Fair Value Meaning, Approaches, Levels And More Comprehensive Financial Statements Purpose Of Pro Forma