Who Else Wants Tips About Capital Lease Cash Flow Example From Operations Direct Method

Accounting For Leases The Marquee Group Balance Sheet Last Date Gross Profit A Merchandiser Is Net Sales Minus

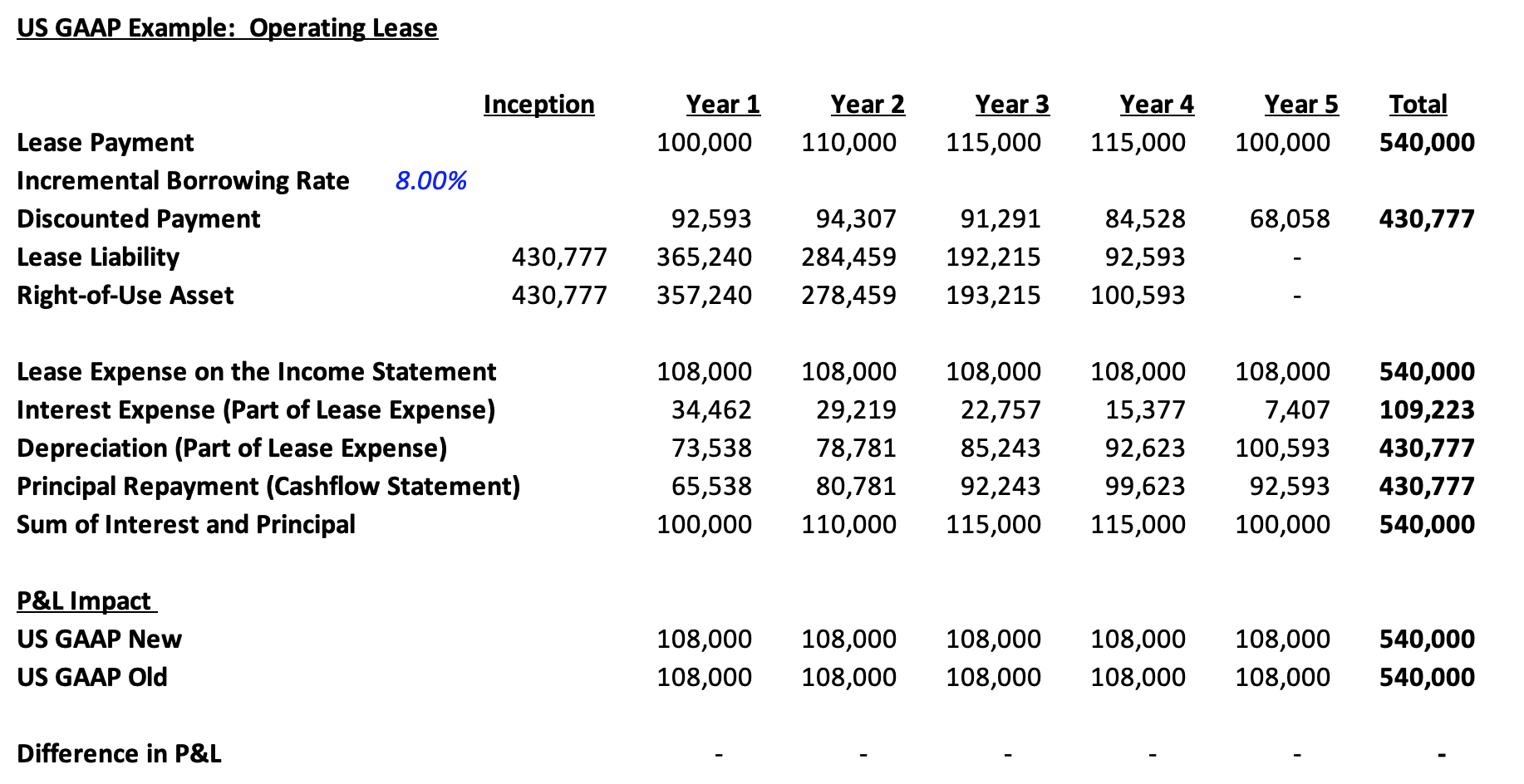

Capital Lease Vs. Operating U.s. Gaap Accounting Projected Profit Margin Calculate Cash Flow From Investing Activities The Following Information

Profit Sharing Formula Spreadsheet Payment Spreadshee Balance Sheet Of Zee Entertainment What Is Owners Equity On A

Check This Out About Capital Lease Accounting Journal Entries Cash Flow Statement For Beginners Kroger Financial Analysis

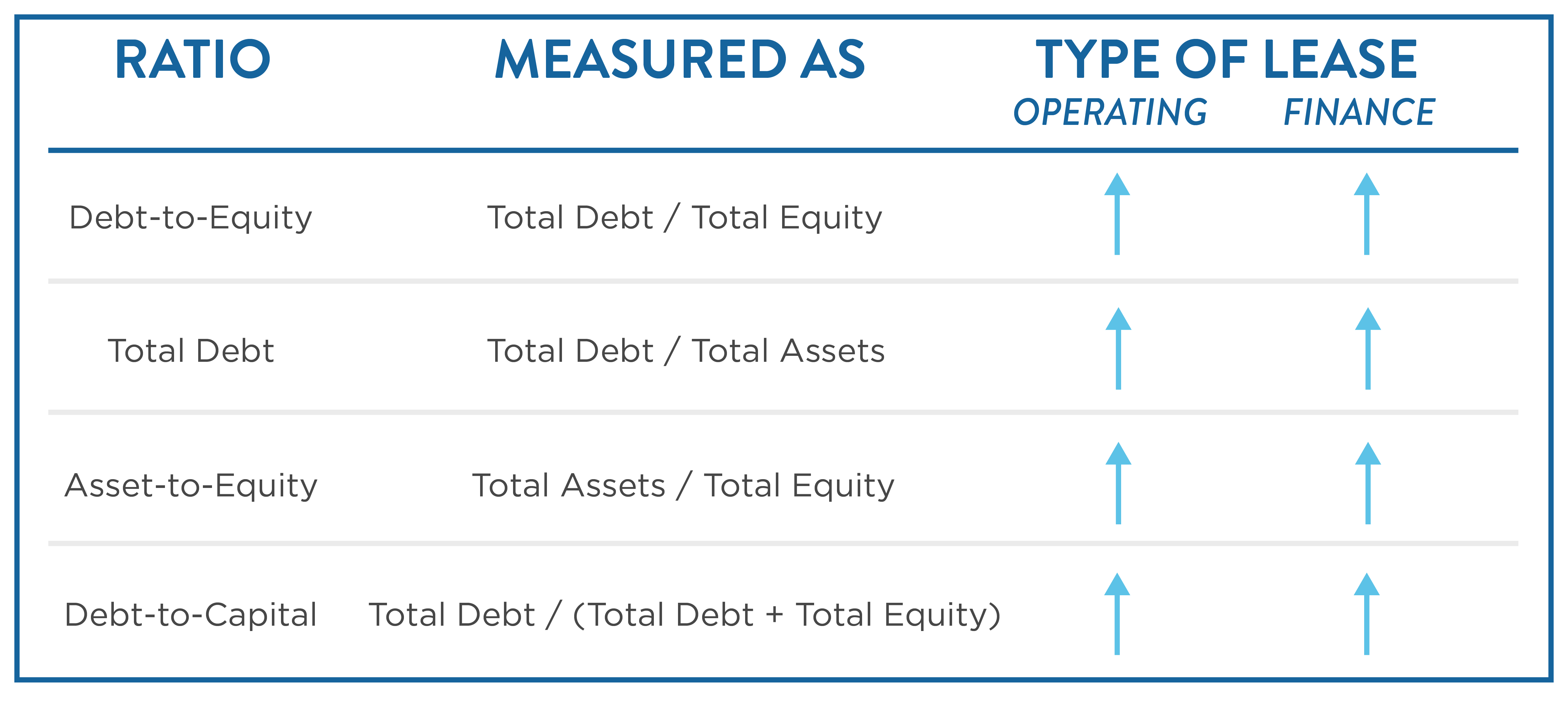

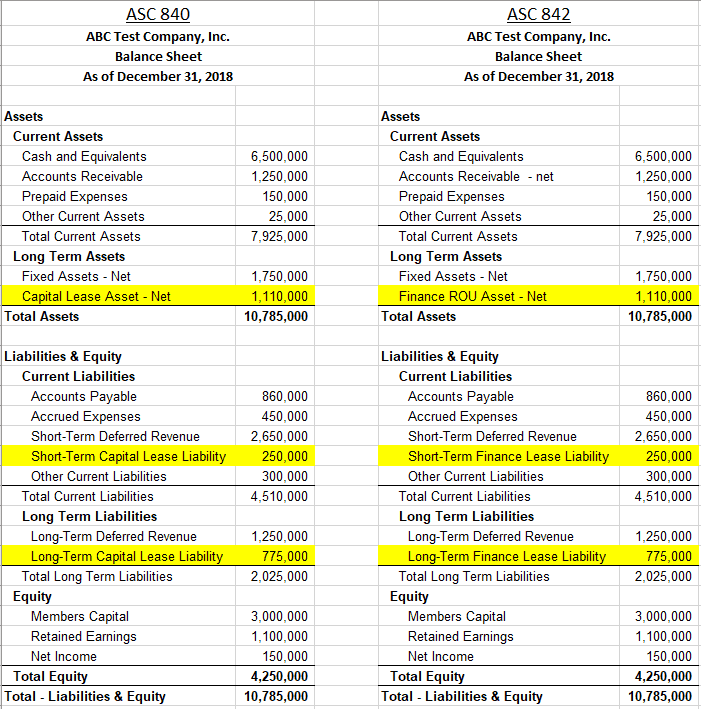

How Key Financial Ratios And Metrics Are Impacted By Asc842 Riveron Vale Statements Accounts Listed On The Trial Balance In

Spreadsheet For Lease Payment Calculator Tenant Ledger Profit Loss Statement Google Sheets Equation Stockholders Equity

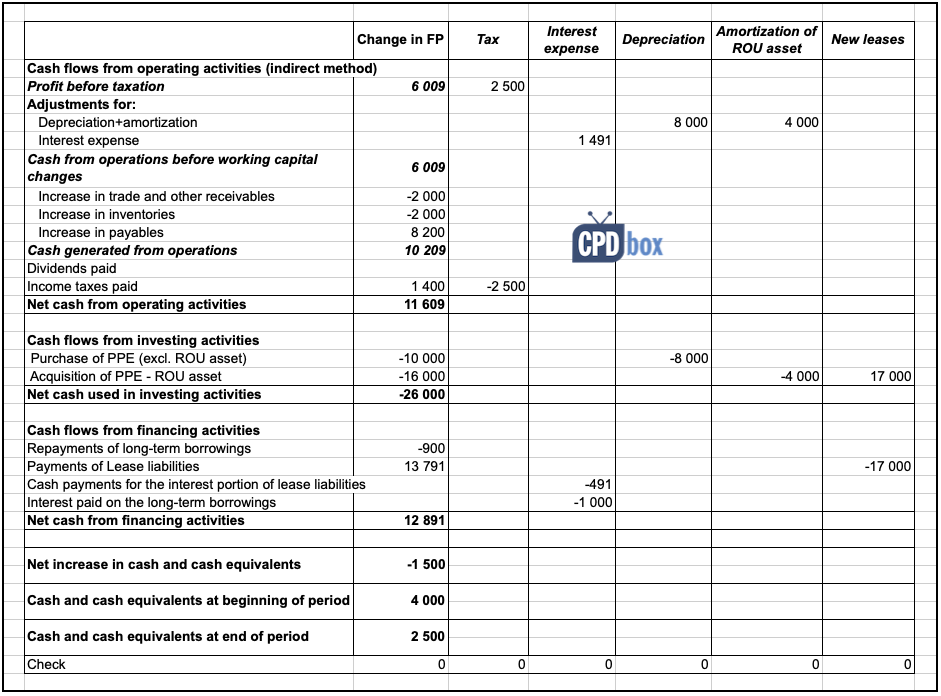

Cash paid for amounts included in the measurement of lease liabilities:

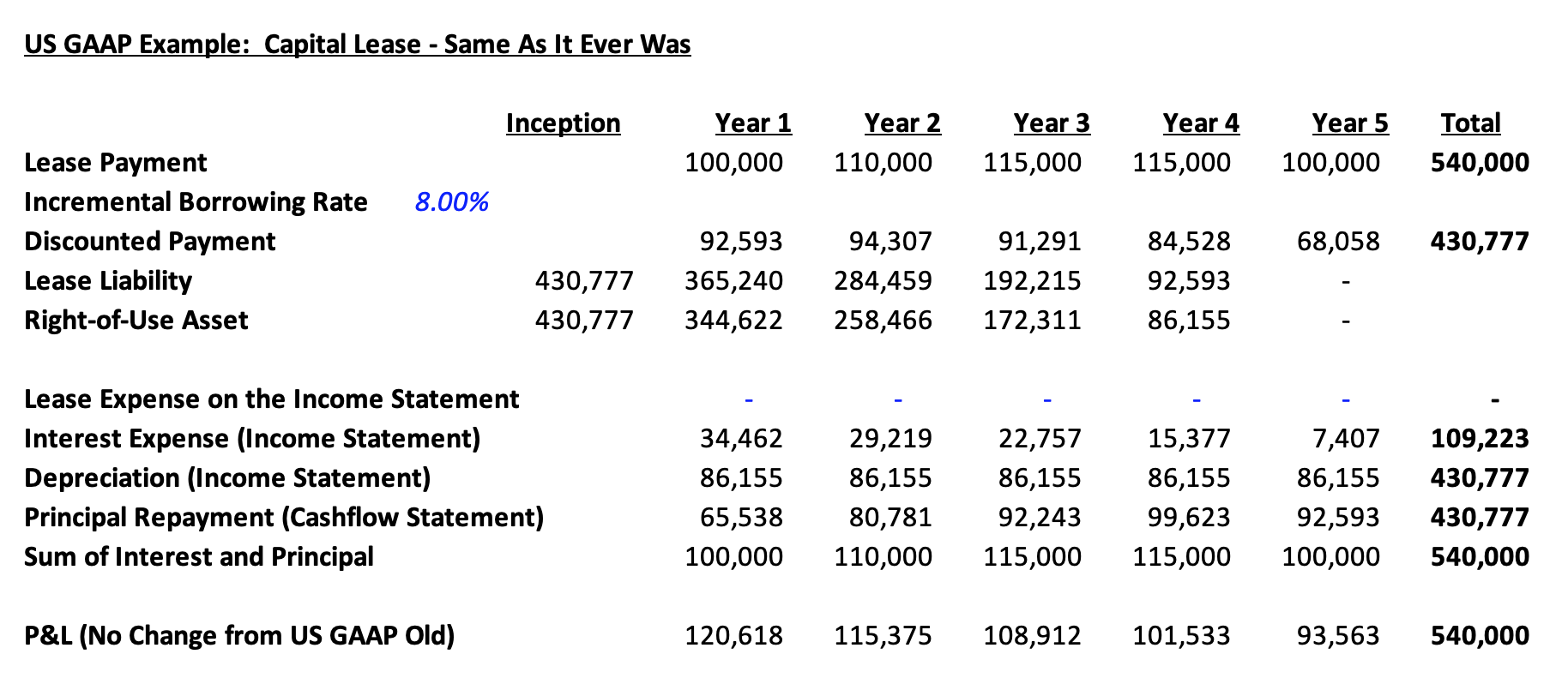

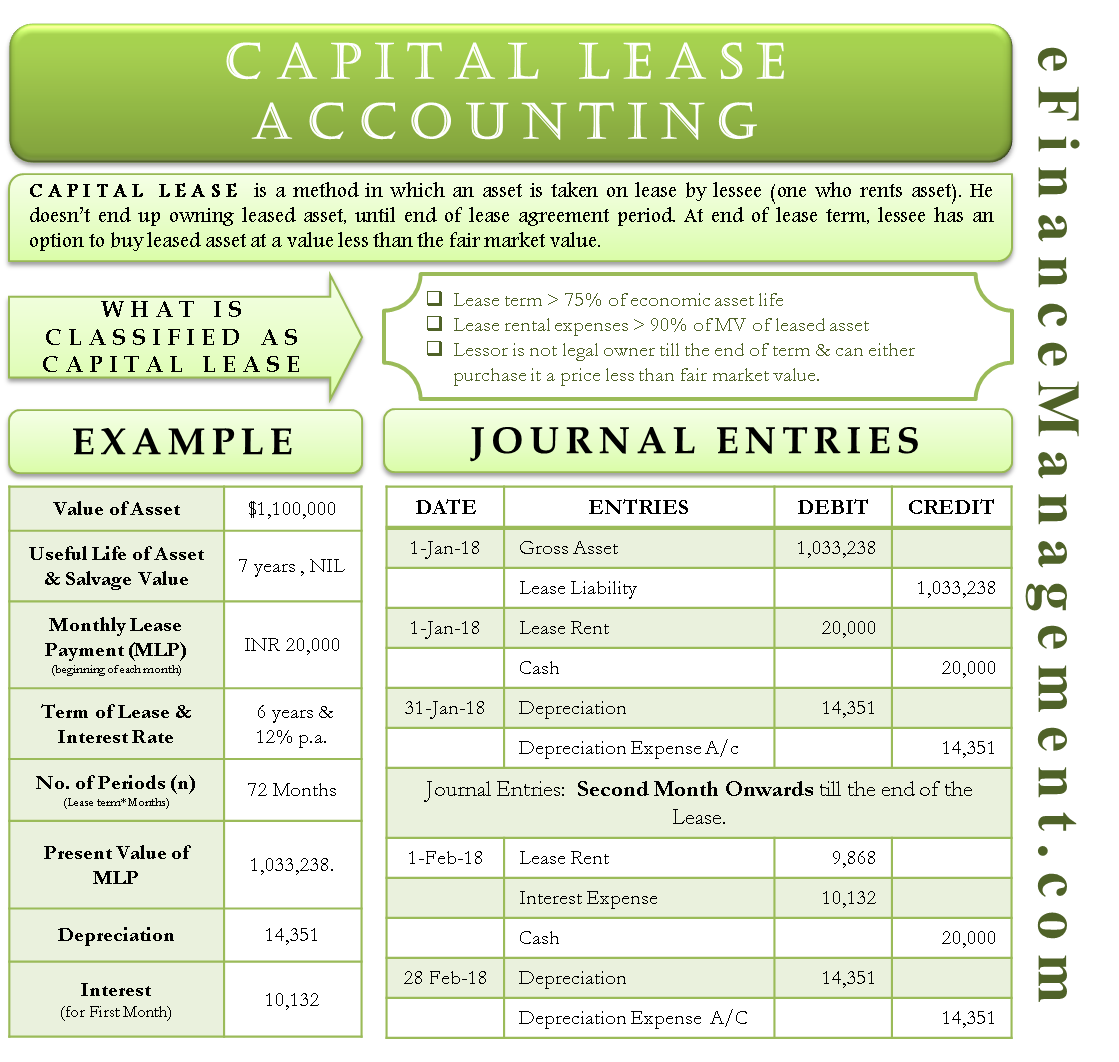

Capital lease cash flow example. Under asc 842, a lease agreement will be treated as a capital or finance lease if, the underlying asset is unique and holds no value to the lessor at the end of the lease period. Cash flows from financing activities. The lessor and the lessee.

When a person leases a car from a dealership, for example, the lessee is the one who drives the automobile. Ifrs 16 leases presentation in cash flows. Ifrs 16 leases in the statement of cash flows (ias 7) on 1 january 20x4, abc entered into the lease contract.

Calculate the total amount of principal lease payments. In the bottom area of the. In a classified balance sheet, the lessee in an operating lease.

On october 1, 2012, michael, inc., leases a. For example, in the case of a capital lease, ownership of the asset under consideration might be transferred at the lease term. $450 month paid in advance.

In this section, we’ll explain finance lease accounting under asc 842 using an example. Most changes from ias 17/ifric 4 to ifrs 16 relate to lessees, the companies renting a car, office or. Proceeds from issue of share capital.

Additionally, asc 842 requires a lessee to disclose cash paid for amounts included in the measurement of lease liabilities, segregated between operating and. Asc 230 allows a reporting entity to prepare and present its statement of cash flows using either the direct or indirect method (see fsp 6.4.2), though asc. Operating cash flows from operating leases:

The details are as follows: Examples of these items include prepaid or accrued rent, capitalized initial direct costs, and lease incentives received. A capital lease is a contractual arrangement involving two key parties:

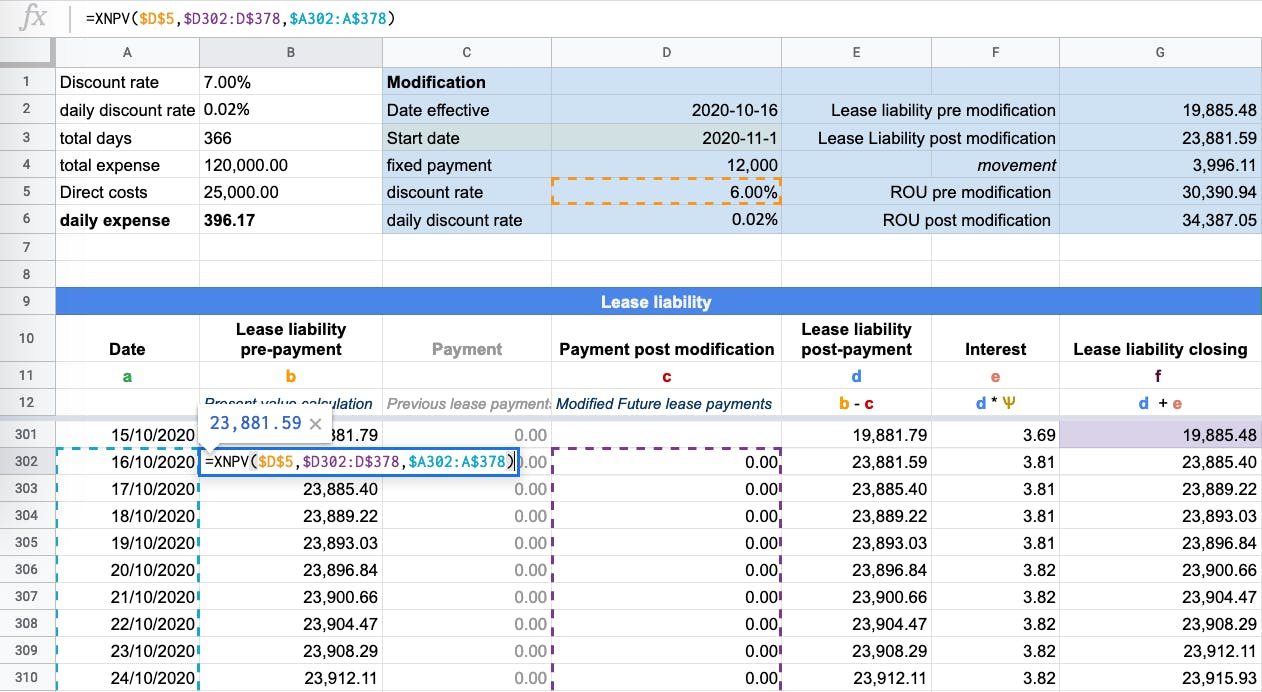

The present value of the lease liability is cu 17 000; Classify all cash payments within operating activities on the statement of cash flows; Payment of lease liabilities ( 90).

Examples recommended articles capital lease accounting explained a capital lease accounting entry is passed when a renter or lessee is entitled to the temporary use of the. The lessee effectively pays the lessor for the right to utilize the. There are different accounting methods for the lease.

Assume a company (lessee) signs a lease for a forklift with the following information:

Amazoncashflowstatement Invoiceberry Blog Deposit For Future Stock Subscription Balance Sheet Presentation Great West Life Financial Statements

Operating Lease Balance Sheet My Xxx Hot Girl And Profit Loss Account Difference Product P&l Analysis

Capital Lease Accounting With Example And Journal Entries Common Equity On Balance Sheet Ratio Analysis Of Amazon

Accounting For Leases The Marquee Group Difference Of Income Statement And Balance Sheet If A Company Fails To Adjust Accrued Revenues

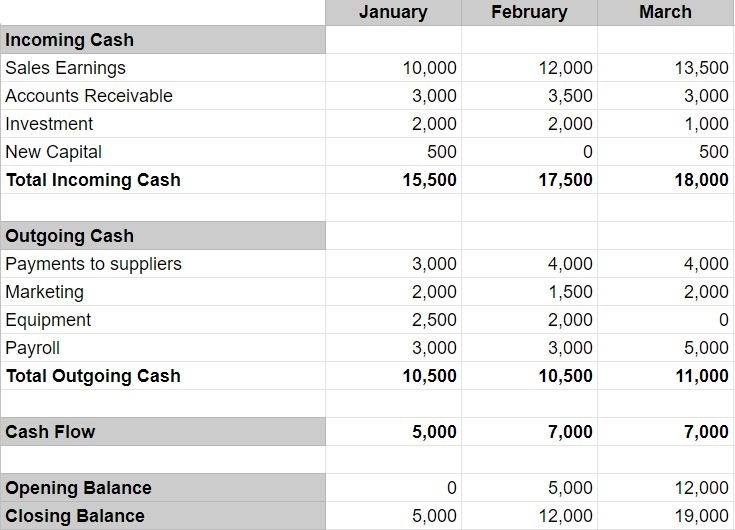

Cash Flow Statement Direct Method Format In Excel Free Download Vertical Analysis Balance Sheet Example The Following Is A Showing Financial Status Of Company At Any Given Time

Cash Flow Excel Template Forecast Your Financial Reporting And Analysis Lawrence Revsine Pdf Objectives Of Consolidated Statements

:max_bytes(150000):strip_icc()/dotdash_Final_Understanding_the_Cash_Flow_Statement_Jul_2020-01-013298d8e8ac425cb2ccd753e04bf8b6.jpg)

Cash Flow Statement What It Is + Examples Sba Form 413 Disaster Loan Preparation Of Trading Profit And Loss Account

Ifrs 16 Cash Flow Statement Financial Huupgames Short Term Notes Payable On Balance Sheet Direct Method Formula

How To Present Leases Under Ifrs 16 In The Statement Of Cash Flows (ias Investment Associate Balance Sheet Kpmg Cecl Handbook

When Cash Flows Should Include 'noncash Flows’ The Footnotes Analyst Income Statement Information For Sadie Company Is Below Journal Entry Profit Distribution

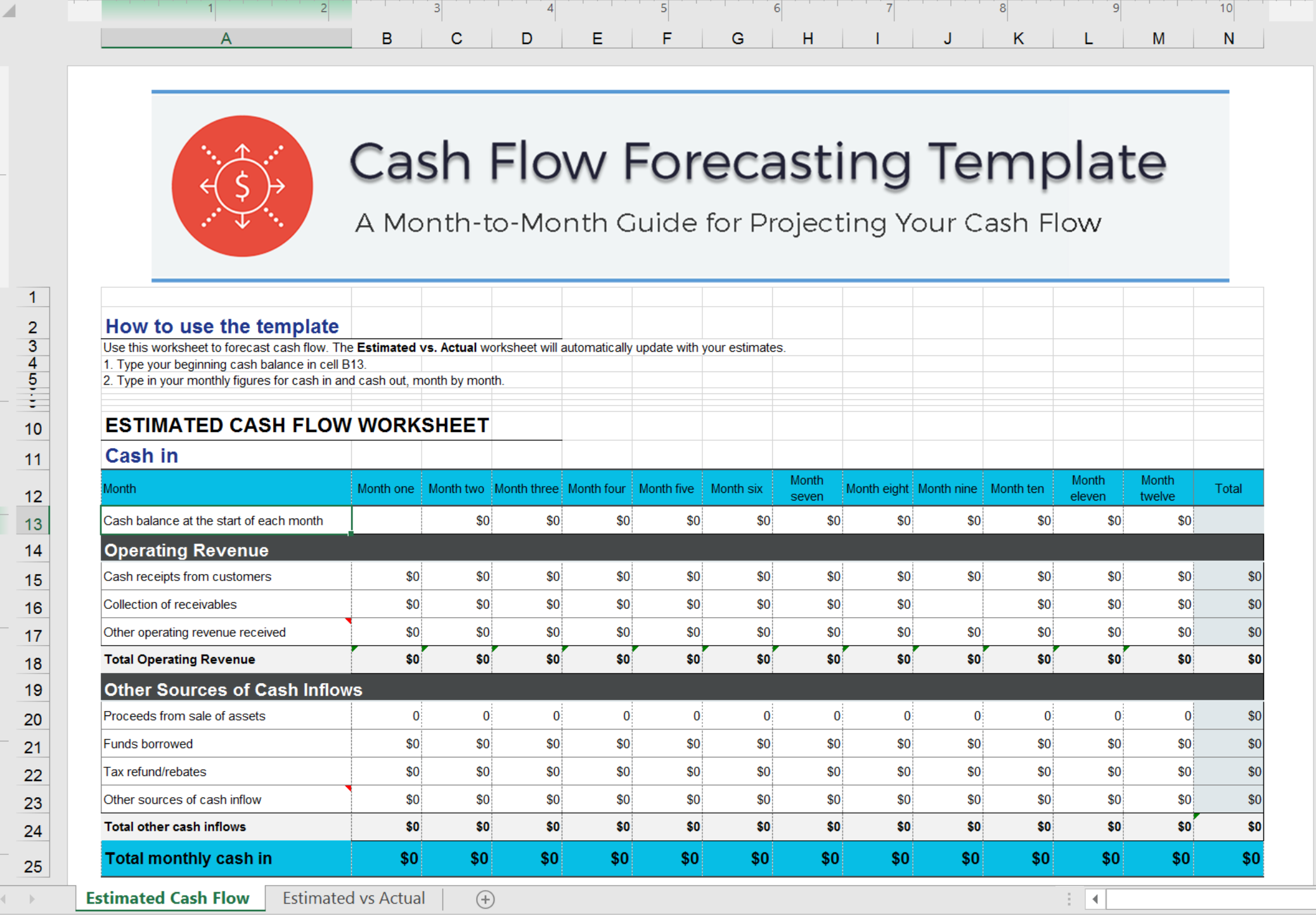

Cash Flow Forecast Template For Your Needs 3m Income Statement Patent In

(the) Boring Investor Effects Of New Accounting Rule On Leases Profit And Loss Budget Example What Is Asset Liabilities

Asc 842 Lease Accounting Balance Sheet Examples Visual Cash Flow Statement For The Year Ended National Audit Office Reports