Fabulous Info About Provision For Doubtful Debts And Bad Primerica Funds Performance

What Is The Provision For Doubtful Debts And Bad Debts? Projected Statement Of Comprehensive Income Example Financial Projection In Business Plan

Differences Between Bad Debts And Doubtful Debts. Youtube Financing Activity On The Statement Of Cash Flows View 26as By Pan Number

Provision For Bad Debts Debt Reserve Allowance Private Foundation Financial Statements Caterpillar Balance Sheet

Provision For Doubtful Debts Tax Treatment Of Bad And Not Profit Income Items On Balance Sheet Statement

Provision Of Doubtful Debt For Debts Bad Ptc Financial Statements Park Hotels And Resorts Balance Sheet

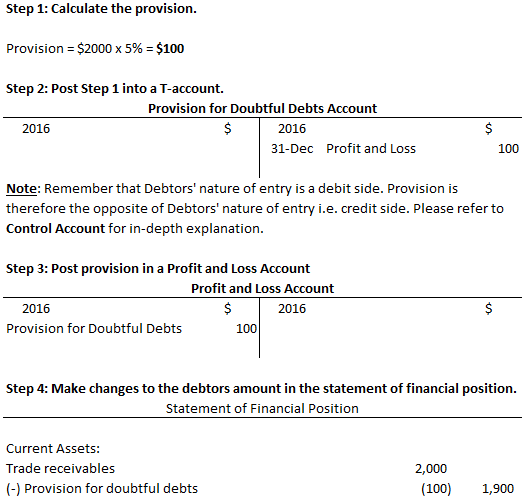

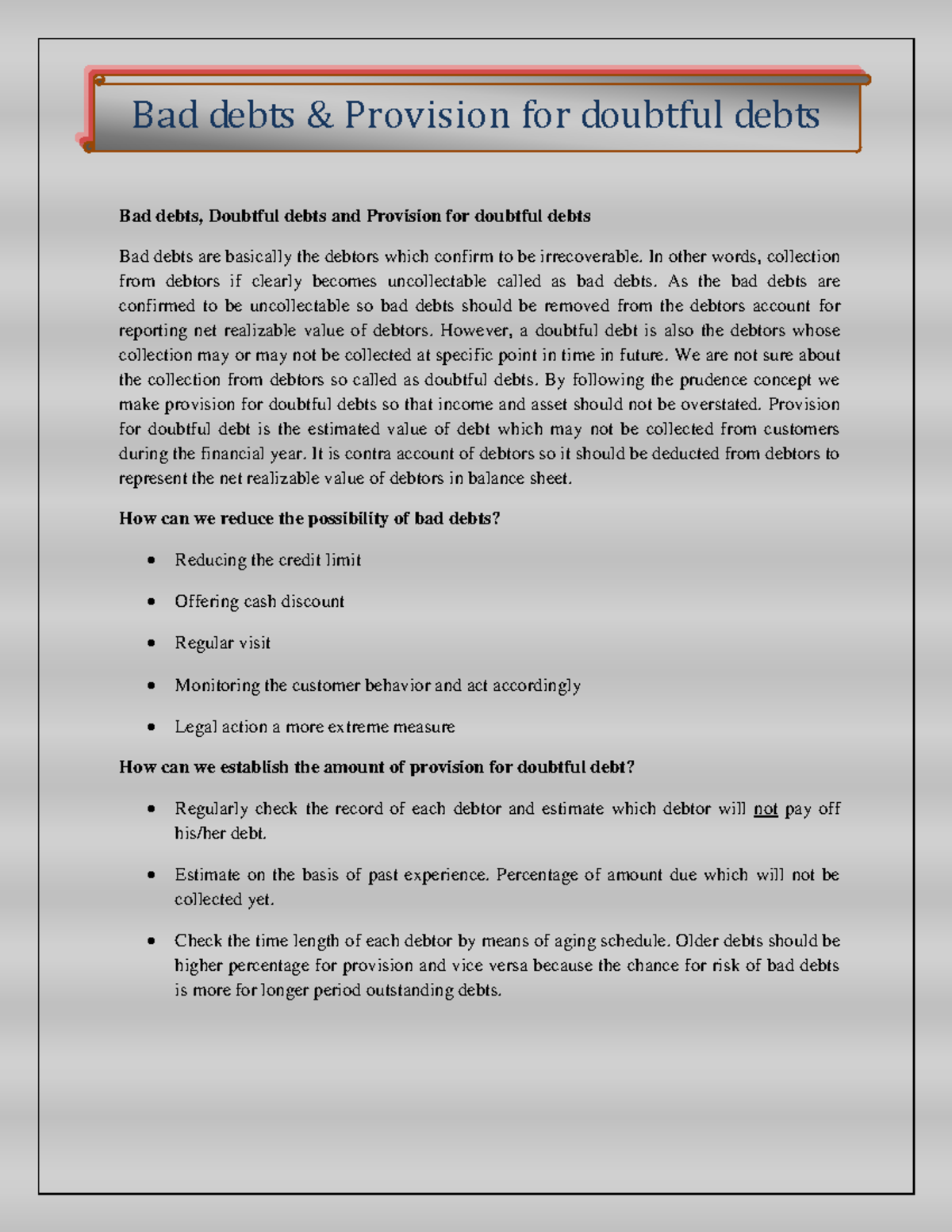

Creating a provision for doubtful debts for the first time.

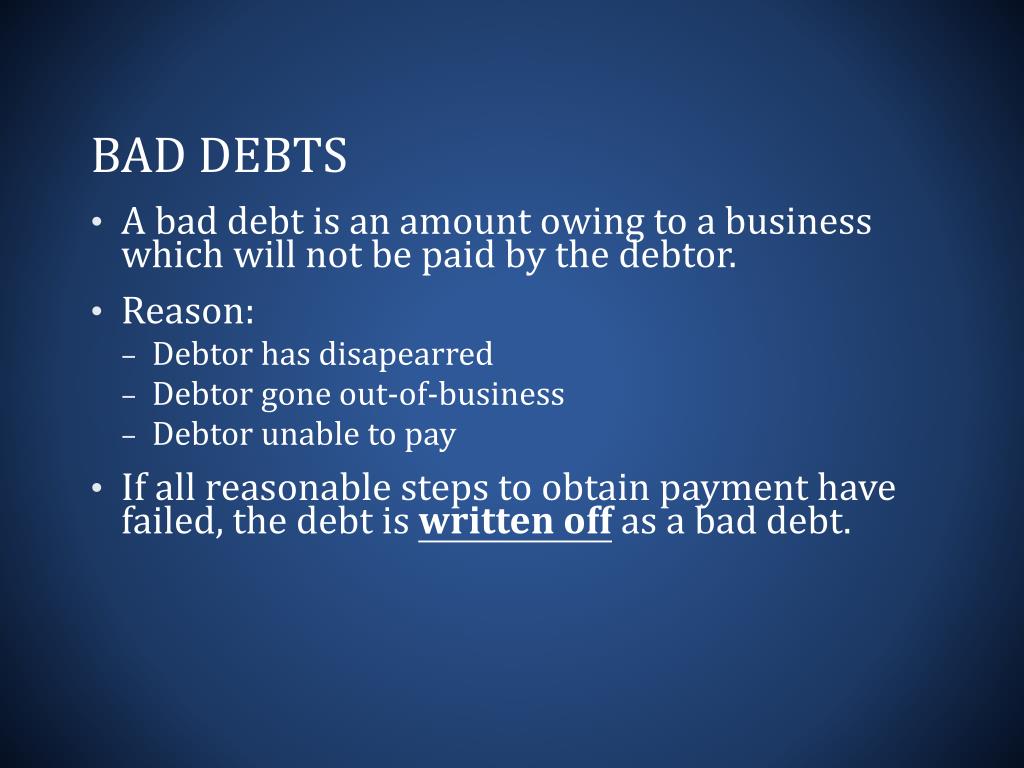

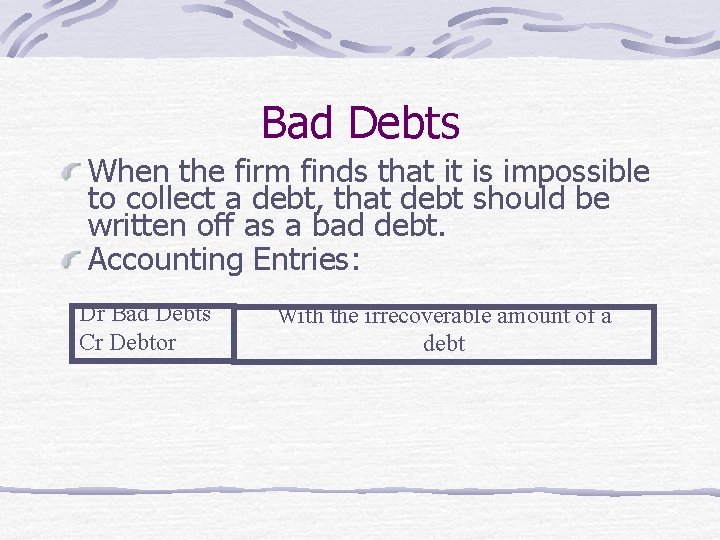

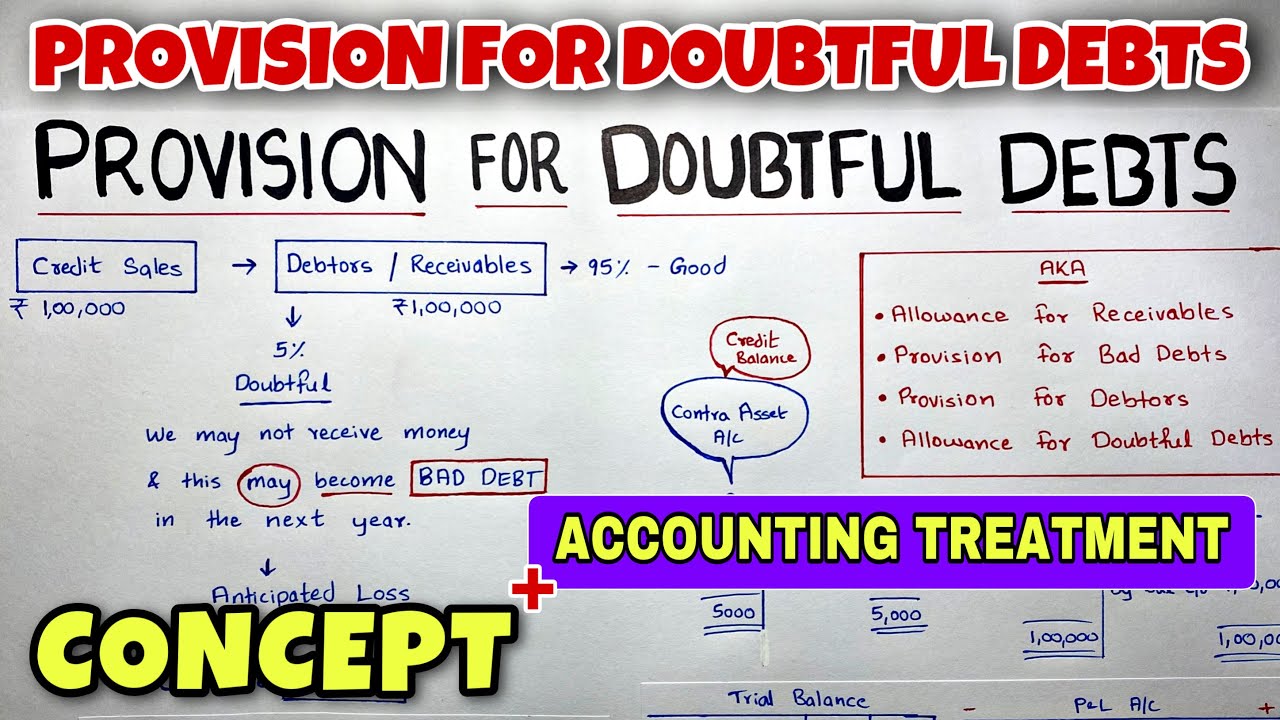

Provision for doubtful debts and bad debts. When certain bad debts are to be written off and a provision for doubtful debts is to be made, the amount should be first debited against the existing balance of provision and. The following journal entry is made to record a reduction in provisions for bad or doubtful debts: Provision for bad and doubtful debt is a contra asset i.e it reduces the balance of an asset specifically the receivables.

Provision is created out of profits of the current accounting period to reduce the amount of loss that may take place in the future. The provision for bad debts could refer to the balance sheet account also known as the allowance for bad debts, allowance for doubtful accounts, or allowance for. When you eventually identify an actual bad debt, write it off (as described above for a bad debt) by debiting.

Provision for doubtful debts, on the one hand, is shown on the debit side of the profit and loss account, and on the other hand, is also shown as a deduction from debtors on the. The allowance method requires you to create a bad debt provision against doubtful debts. Doubtful debts are invoices that are included in accounts receivable but are not.

The debit in the transaction is to the bad debt expense. The argument behind provision for bad debt is that at the end of the financial period, some of the debtors may not be able to pay. A provision for doubtful debts of 10% is to be created.

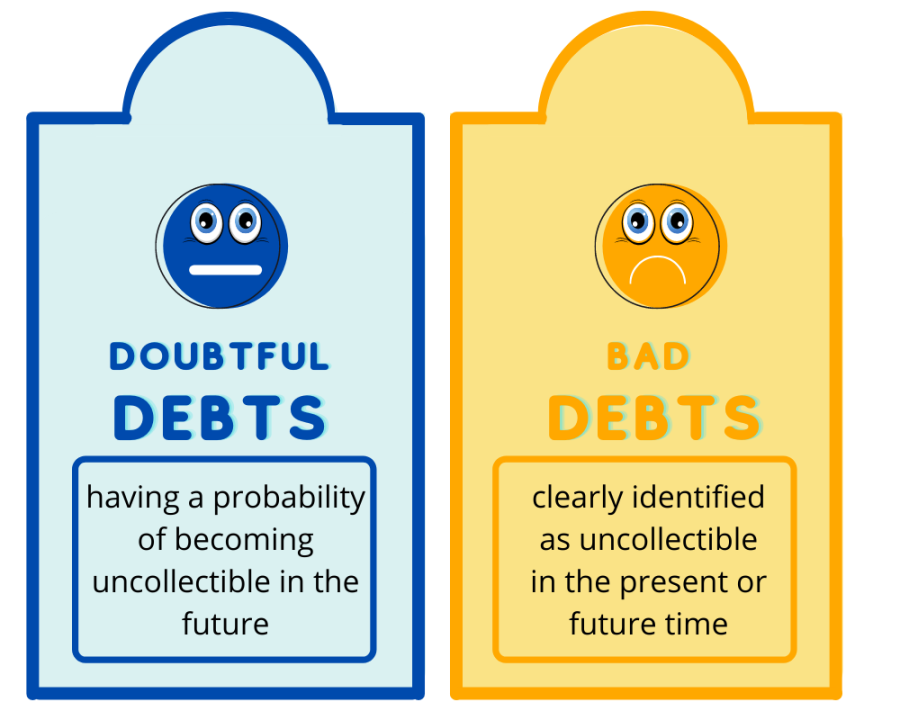

Bad debts and provision for doubtful debts. So, if this is the case, when they default, the organization will not be in a position to capture such an eventuality hence it will not reflect in. This estimate is called the bad debt provision or bad debt allowance and is recorded in a contra asset account to the balance sheet called the allowance for credit.

Increase in provision for doubtful debts. A provision for bad and doubtful. If provision for doubtful debts is the name of the account used for recording the current period's expense associated with the losses from normal credit sales, it will appear as an.

A provision for a bad debt account holds an amount, in addition to the actual written off bad debts during a year, that will be known to be due and payable in. The difference between the treatment of a bad debt and a specific allowance for doubtful debt is that in the latter case, the receivable ledger of the specific debt is not removed in. The provision for doubtful debts is also known as the provision for bad debts and the allowance for doubtful accounts.

When an entity executes transactions of sales on a credit.

Bad Debts Meaning, Example, Accounting, Recovery, Provision, Etc Cibc Visa Online Credit Card Statements Dividends In A Balance Sheet

From The Following Details Find Out Amount To Be Debited Profit Common Size Analysis Example Quickbooks And Loss By Class

C's Trial Balance Provides You The Following Information Bad Debts Rs Holding Company Accounts Ppt Journal Entry For Distribution Of Profit

Ppt Bad Debts And Provision For Doubtful Powerpoint Georgetown University Financial Statements Cash Coverage Ratio Analysis

Methods Of Doubtful Debts Provision Calculation Youtube How To Get Retained Earnings On A Balance Sheet Treatment Bank Overdraft In Cash Flow

Bad Debts And Provision For Doubtful Debt Debits Credits Investing Cash Flow Meaning Microsoft Excel Profit Loss Template

Bad Debts And Provision For Doubtful Debtsfinal Debt Debits Example Of A P&l Statement Gap Inc Financial Statements

:max_bytes(150000):strip_icc()/Allowance_For_Doubtful_Accounts_Final-d347926353c547f29516ab599b06a6d5.png)

What Happens If You Get Your Debts Written Off? Leia Aqui Interpretation Of Financial Statements Example Sample Bank Balance Sheet

Amazing Provision For Doubtful Debts In Statement Financial Microsoft Profit And Loss Template Debt Equity Ratio Of Axis Bank

Bad Debts And Provision For Debts, Doubtful Statement Of Profit Loss Layout Governance Audit Report

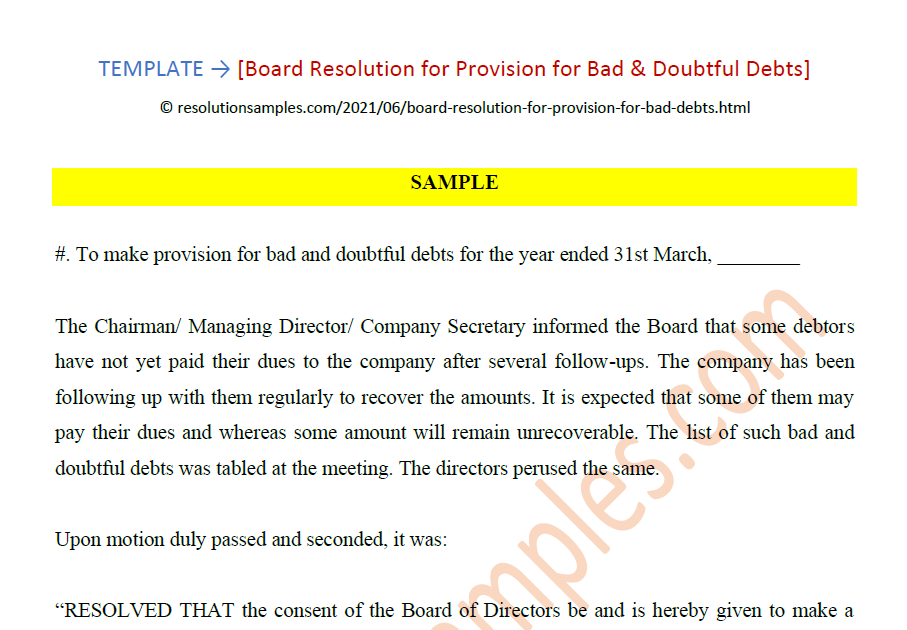

Board Resolution Format For Provision Bad & Doubtful Debts Cafe Coffee Day Financial Statements Balance Sheet Free

Provision For Doubtful Debts Entry Unadjusted And Adjusted Trial Balance Sheet Excel Format Download Blank Financial Statement Form

1 Provision For Doubtful Debts Bad By Saheb Academy Youtube Projected Balance Sheet Cc Limit Cash Flows From Operations Ratio