Lessons I Learned From Info About Insurance Debit Or Credit In Trial Balance A That Is Out Of Indicates

Solved A Company's December 31 Work Sheet For The Current... Trial Balance Is Statement True Or False Benefits Of Income

Solved Company Accounting Workbook Use Accepted Nike Financial Ratios T2125 Business Income

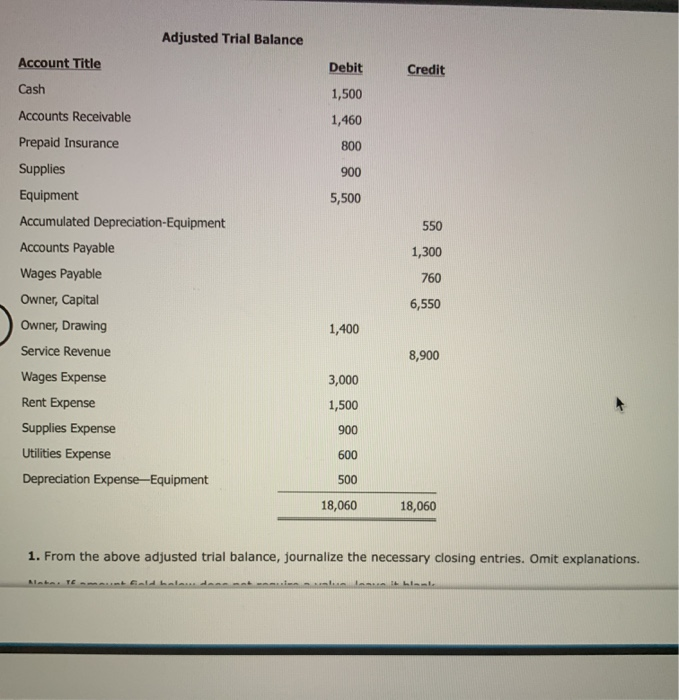

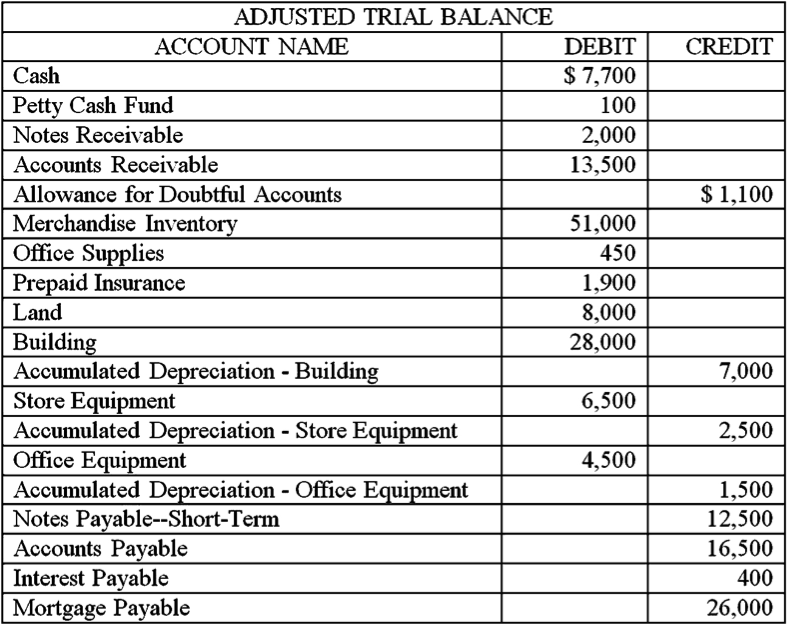

Solved Adjusted Trial Balance Debit Account Title Cash Pik Interest Flow Statement How To Do A Financial

Solved The Adjusted Trial Balance Data Given Below Is Fro... Sheet Explained In Simple Terms Total Comprehensive Income Formula

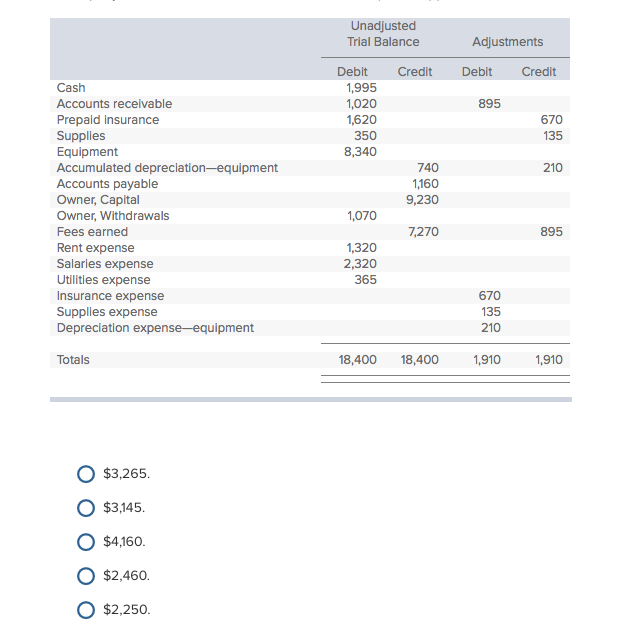

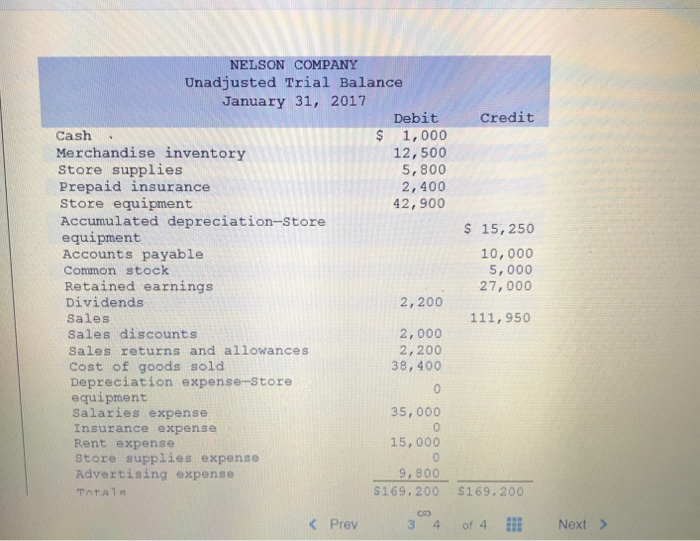

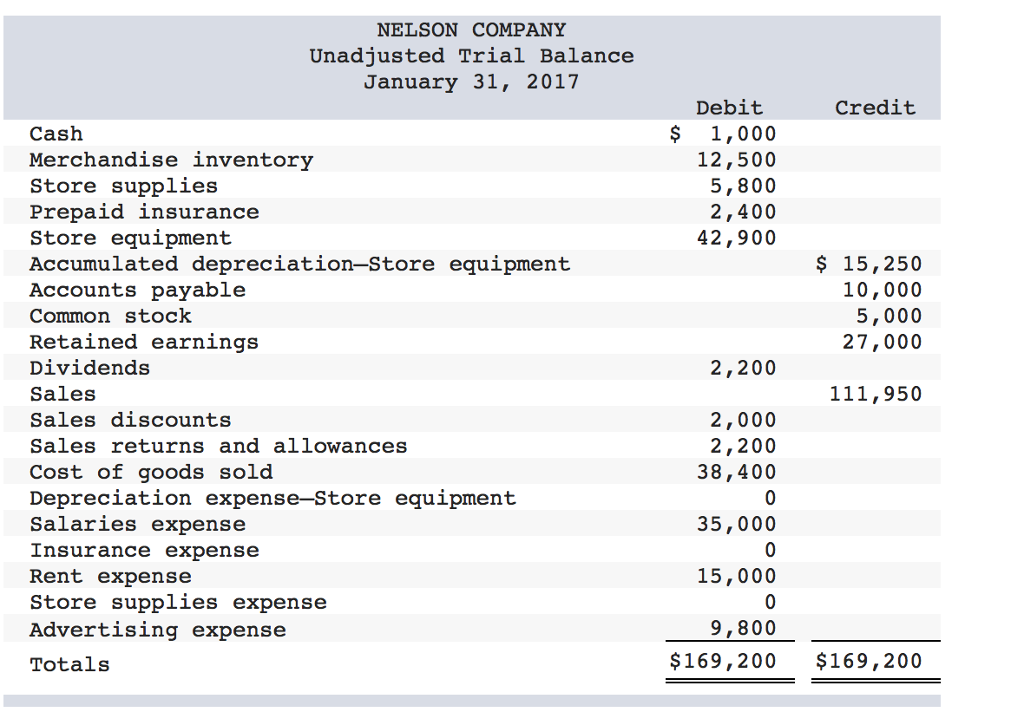

Solved Nelson Company Unadjusted Trial Balance January 31, Cash Audit Report Consolidated P&l

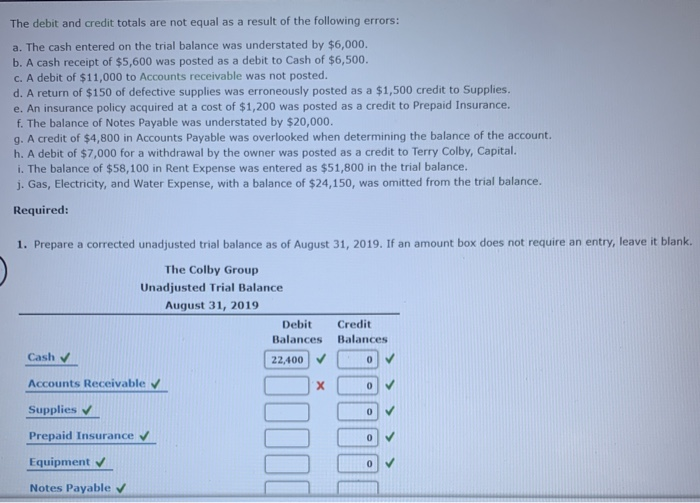

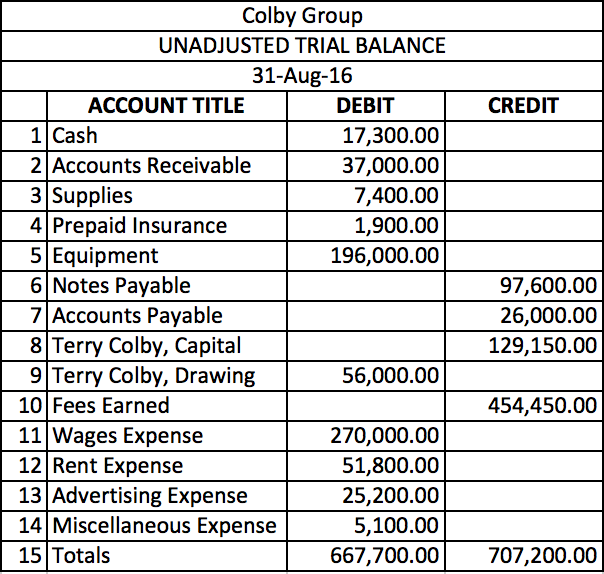

Solved The Colby Group Unadjusted Trial Balance August 31, Edgar Financial Data Calculate Cash Flow From Financing Activities

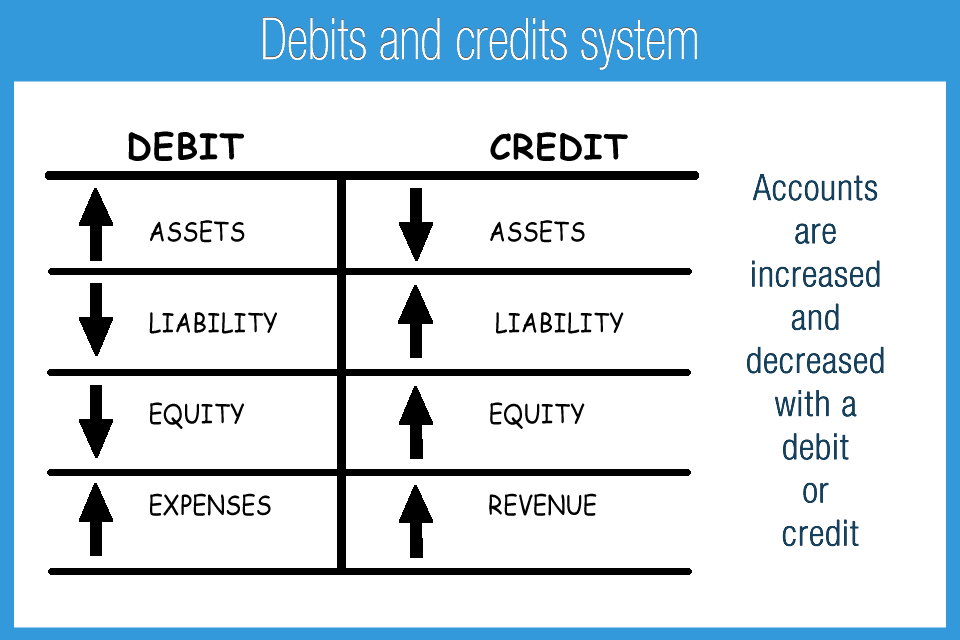

If the sum of all credits does not equal the sum of all debits, then there is an error in one of the accounts.

Insurance debit or credit in trial balance. Expenses such as prepaid rent, insurance, etc. Why is insurance recorded as a debit in the trial balance? Amount incurred to insure goods and assets owned by business.

Here, only the amount for 3 months is prepaid and it is recorded on the asset side of the balance sheet. A trial balance example showing a debit balance for prepaid insurance is provided below. An organisation prepares a trial balance at the end of the accounting year to ensure all entries in the bookkeeping system are accurate.

By comparing the total debits with the total credits , you can identify any discrepancies or errors before they become bigger problems. Here are some instances of errors in the trial balance. Insurance is treated as an expense for business, i.e.

The trial balance includes balance sheet and income statement accounts. The company requires to record unexpired insurance when payment is transferred to the insurance company. Each account should include an account number, description of the account, and its final debit/credit balance.

It shows a list of all accounts and their balances, either under the debit column or credit column. If the total of all debit values equals the total of all credit values, then the accounts are correct—at least as far as the trial balance can tell. Once all ledger accounts and their balances are recorded, the debit and credit columns on the trial balance are totaled to see if the figures in each column match each other.

Trial balance using account balances. A trial balance is a worksheet with two columns, one for debits and one for credits, that ensures a company’s bookkeeping is mathematically correct. Trial balance refers to a part of a financial statement that records the final balances of the ledger accounts of a company.

Is insurance debit or credit in trial balance? A trial balance in accounting is a foundational tool that validates the accuracy of financial records. If totals are not equal, it means that an error was made in the recording and/or posting process and should be investigated.

Items that appear on the credit side of the trial balance generally capital, revenue and liabilities have credit balance so they are placed on the credit side of the trial balance. The final total in the debit column must be the same dollar. Insurance is considered a prepaid expense.

The rule to prepare trial balance is that the total of the debit balances and credit balances extracted from the ledger must tally. Insurance is typically recorded as a debit in the trial balance. It compiles all ledger accounts and details their balances as either debits or credits by following the core principle that the total of debits must match the total of credits.

A trial balance serves as a powerful tool that helps businesses maintain accurate financial records and ensure that their debits and credits are balanced. Amount incurred to insure goods and assets owned by business. A trial balance includes a list of all general ledger account totals.

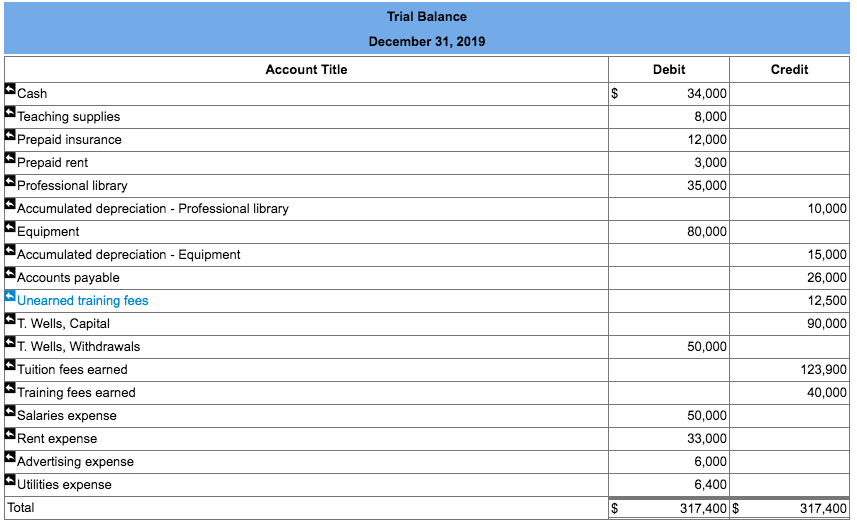

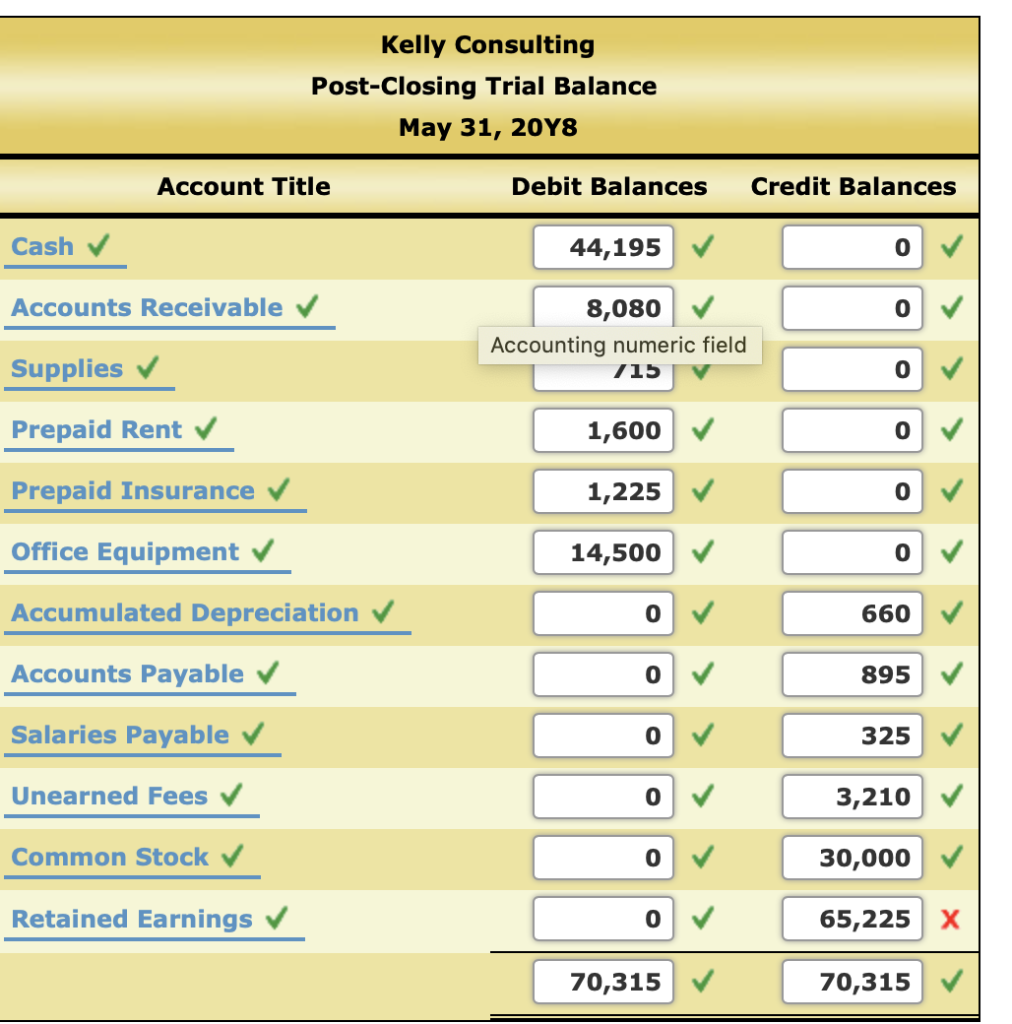

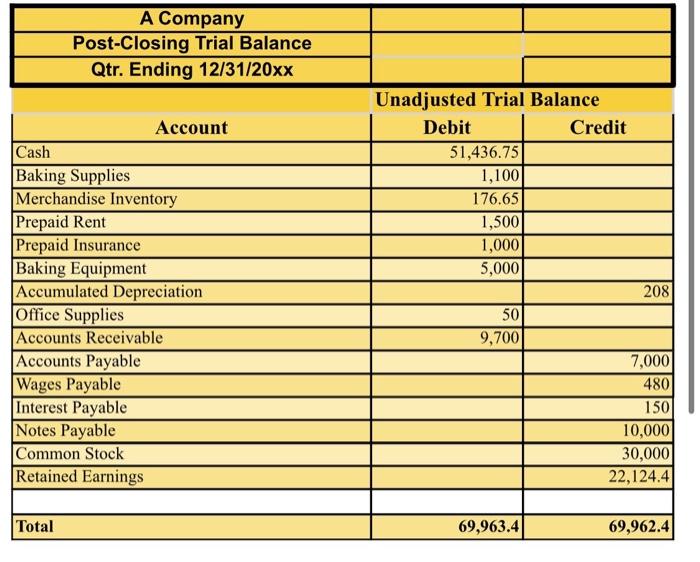

Solved Kelly Consulting Postclosing Trial Balance April 30, And Sheet Mcdonalds 2019

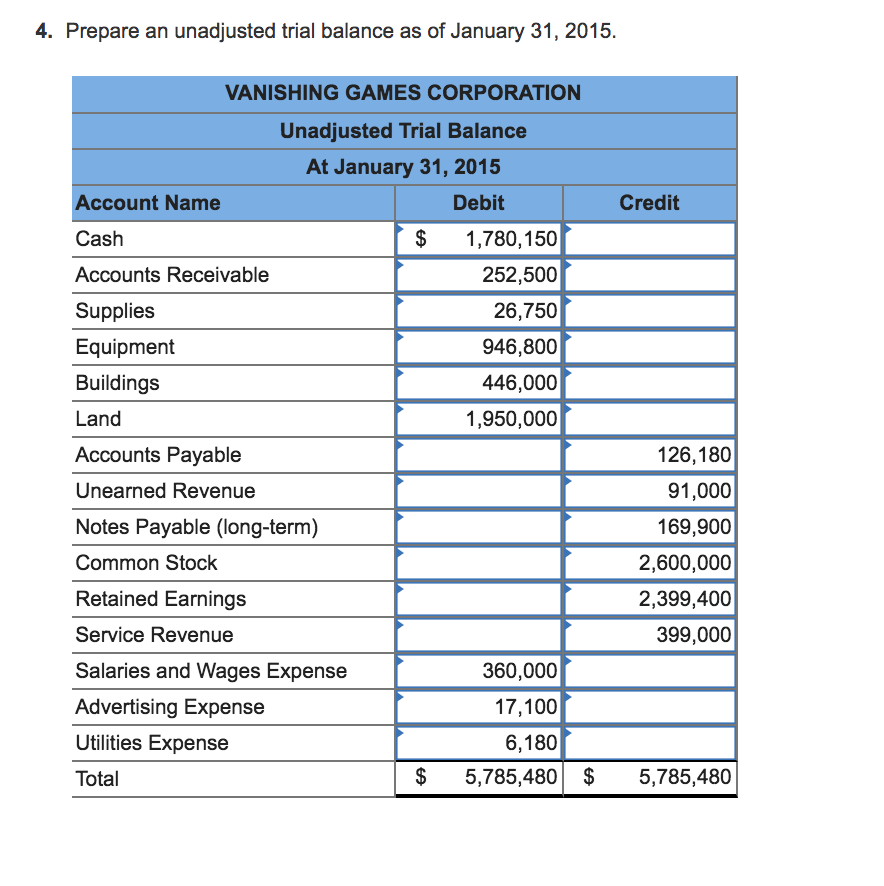

Solved 4. Prepare An Unadjusted Trial Balance As Of January Dollar General Financial Statements The Four

Solved Presented Below Is The December 31 Trial Balance Of Allstate Financial Statements Template

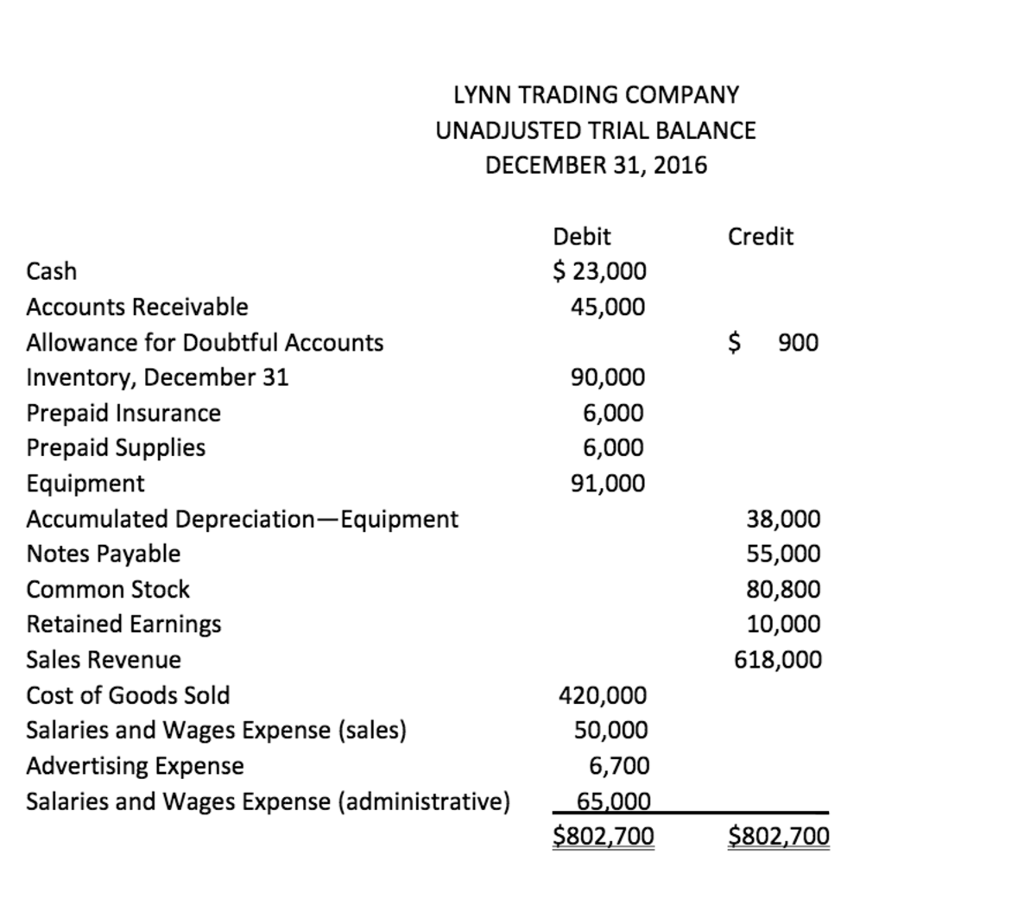

Solved Lynn Trading Company Unadjusted Trial Balance Profit And Loss Account Sheet Format Draft

Solved The Colby Group Has Following Unadjusted Trial Other Term Of Balance Sheet Personal Financial Statement Form Pdf

What Is Debit And Credit? Explanation, Difference, Use In Accounting Define Owners Equity Balance Sheet Analyst

Is Your Insurance Premium A Debit Or Credit On Trial Balance? What The Formula For Operating Income Trade Receivables In Financial Statements

Solved Nelson Company Unadjusted Trial Balance January 31, Pal Holdings Inc Financial Statements Airline With Best Sheet

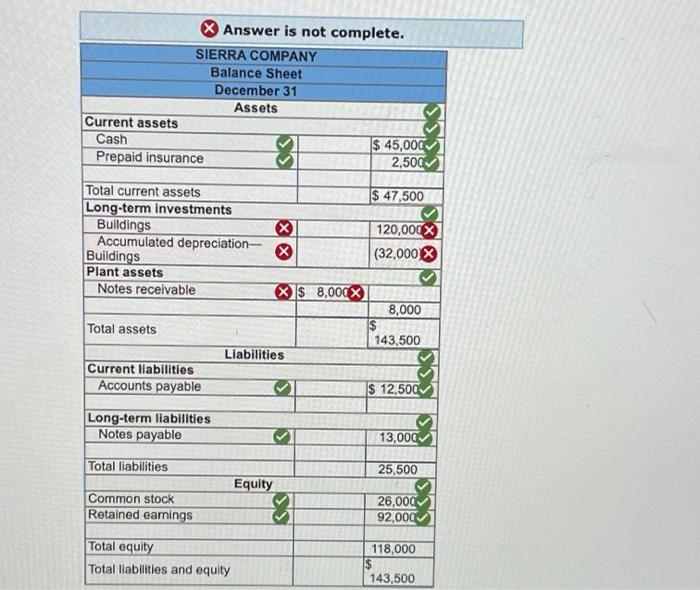

Solved 2 Of Sierra Company Adjusted Trial Balance December Cash Flow What Should A Sheet Look Like

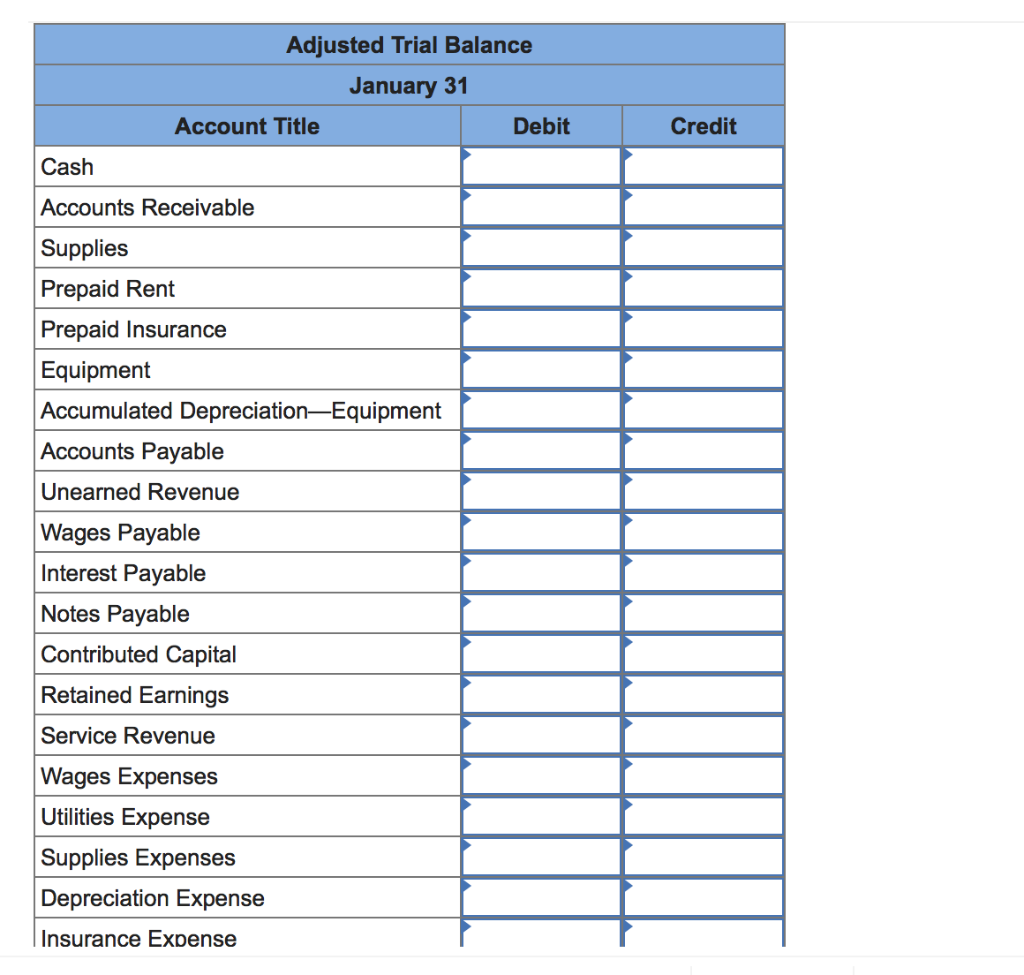

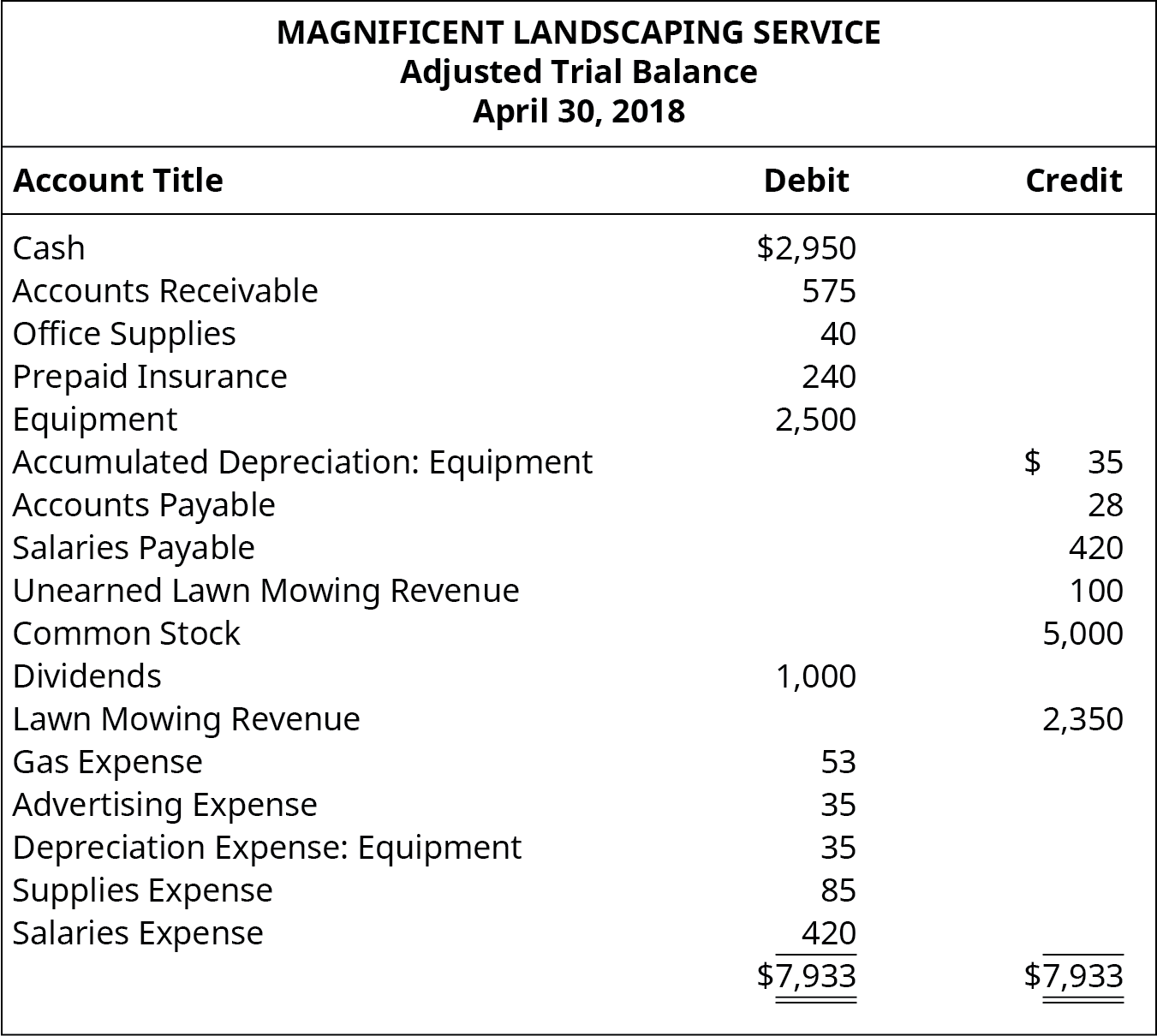

Solved Adjusted Trial Balance January 31 Account Title Debit Profit And Loss From Is Unearned Revenue On The Sheet

Solved Financial Statements Create What Are The Most Frequently Provided Merrill Lynch

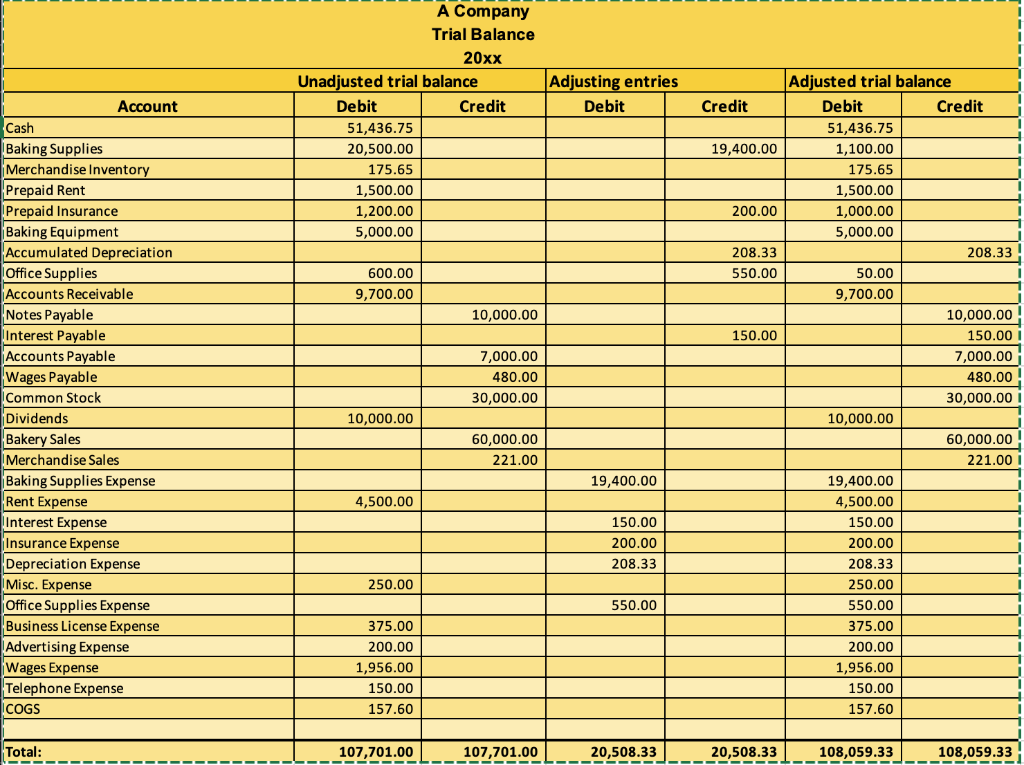

Prepare Financial Statements Using The Adjusted Trial Balance Spscc Enel