One Of The Best Tips About Going Concern Note In Financial Statements Flow Of Accounts Into

How To Prepare Financial Statements When Going Concern Does Not Apply Where Is Net Income On The Balance Sheet Jnug

Ppt Going Concern Slaus 21 Powerpoint Presentation, Free Download Balance Sheet Is Also Known As Financial Ratios Purpose

Going Concern Diageo Balance Sheet Prepare Trading And Profit Loss Account

The Terminology Of Going Concern Standards Cpa Journal Adjusted Balance Sheet Stock P&l Spreadsheet

Pinnacle Financial Statements Going Concern Files. Ikea Vertical Analysis Is Also Known As

Disclosure In Financial Statements Notes To Accounts Market Indian Railways International Accounting Reporting Standards

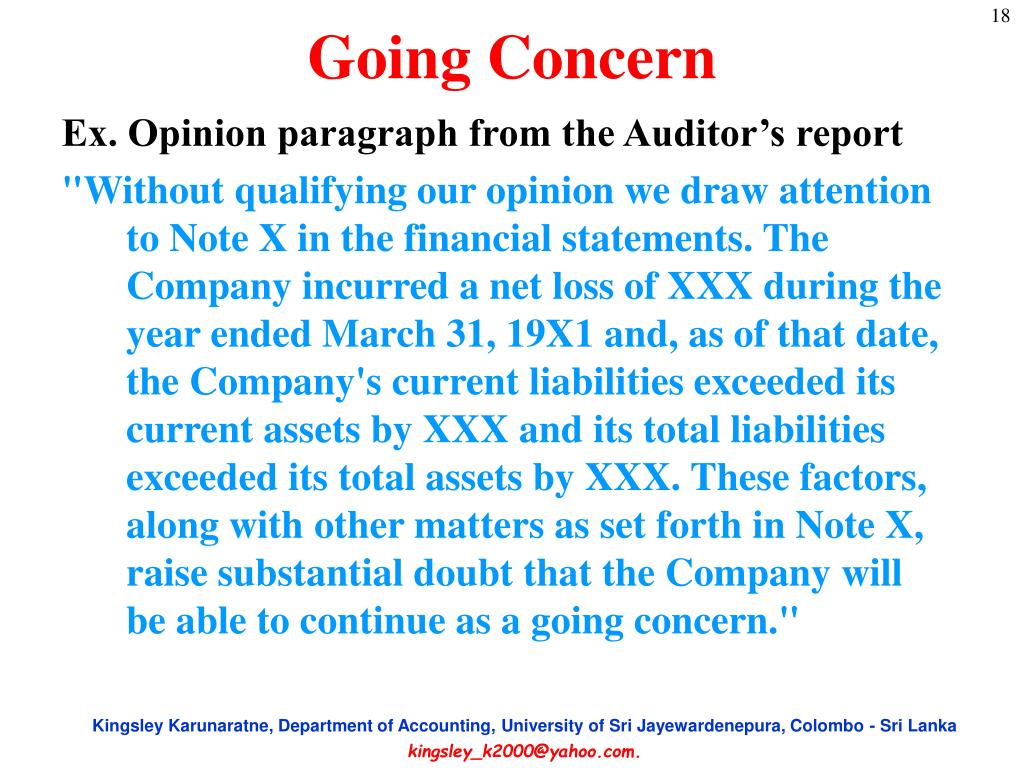

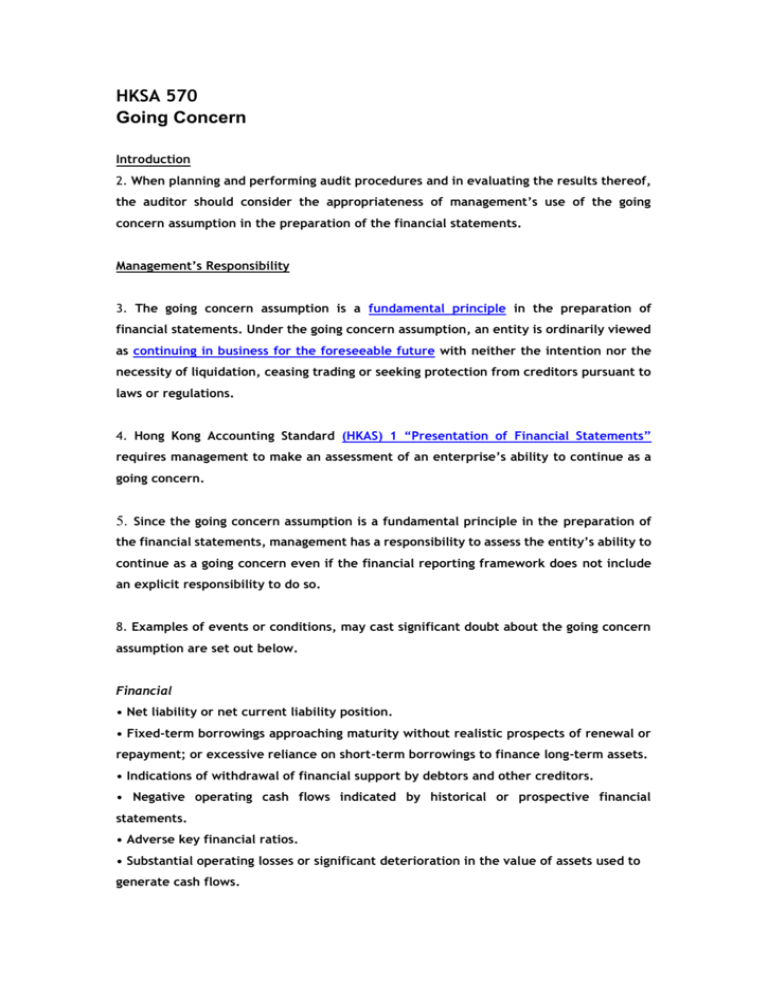

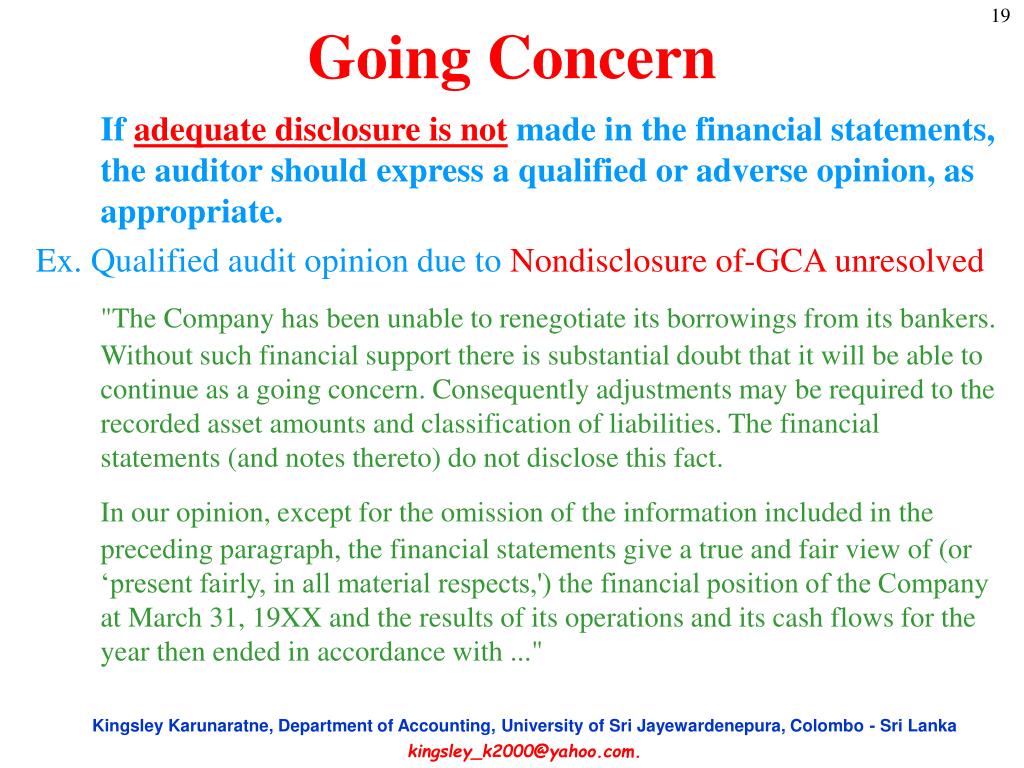

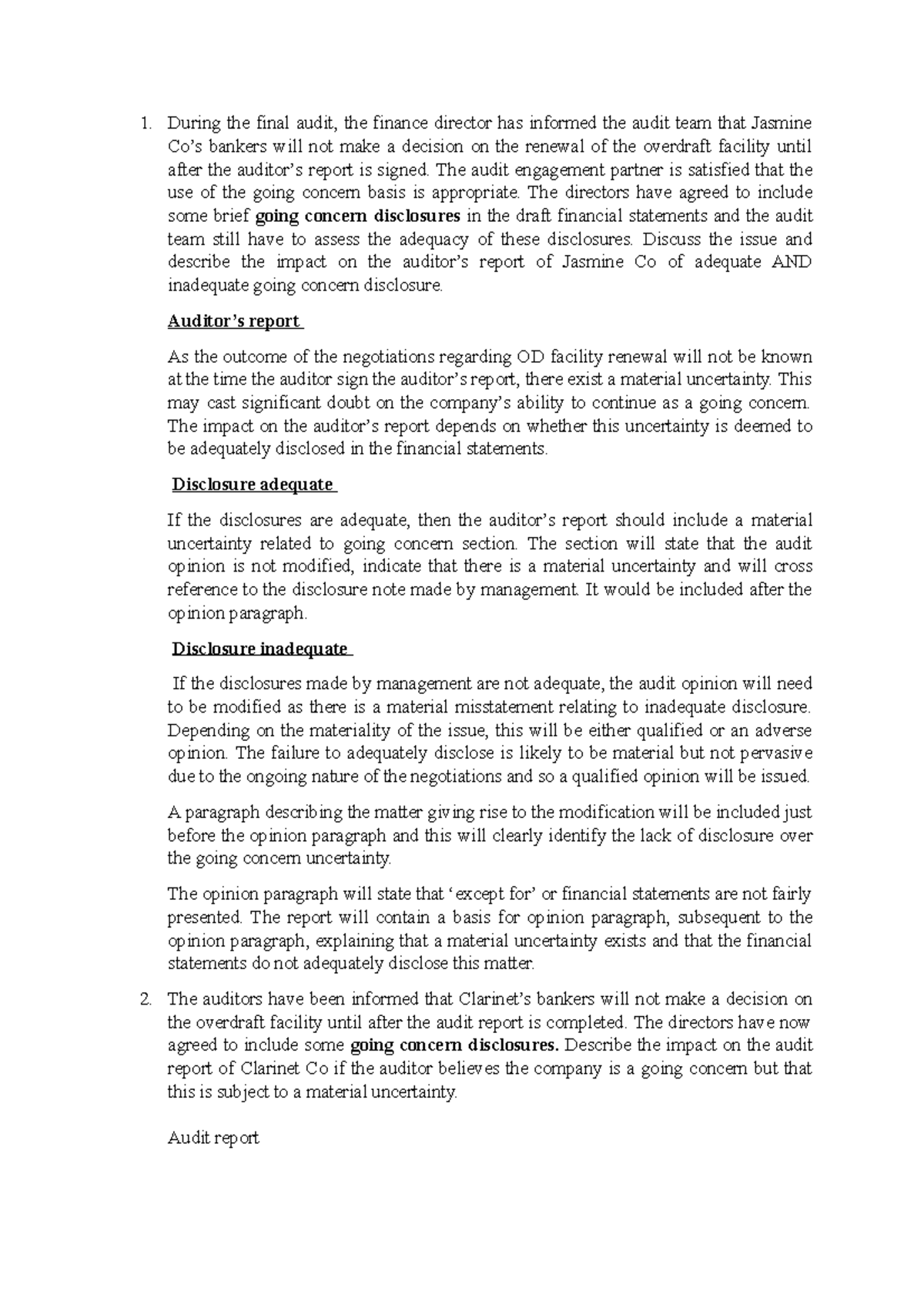

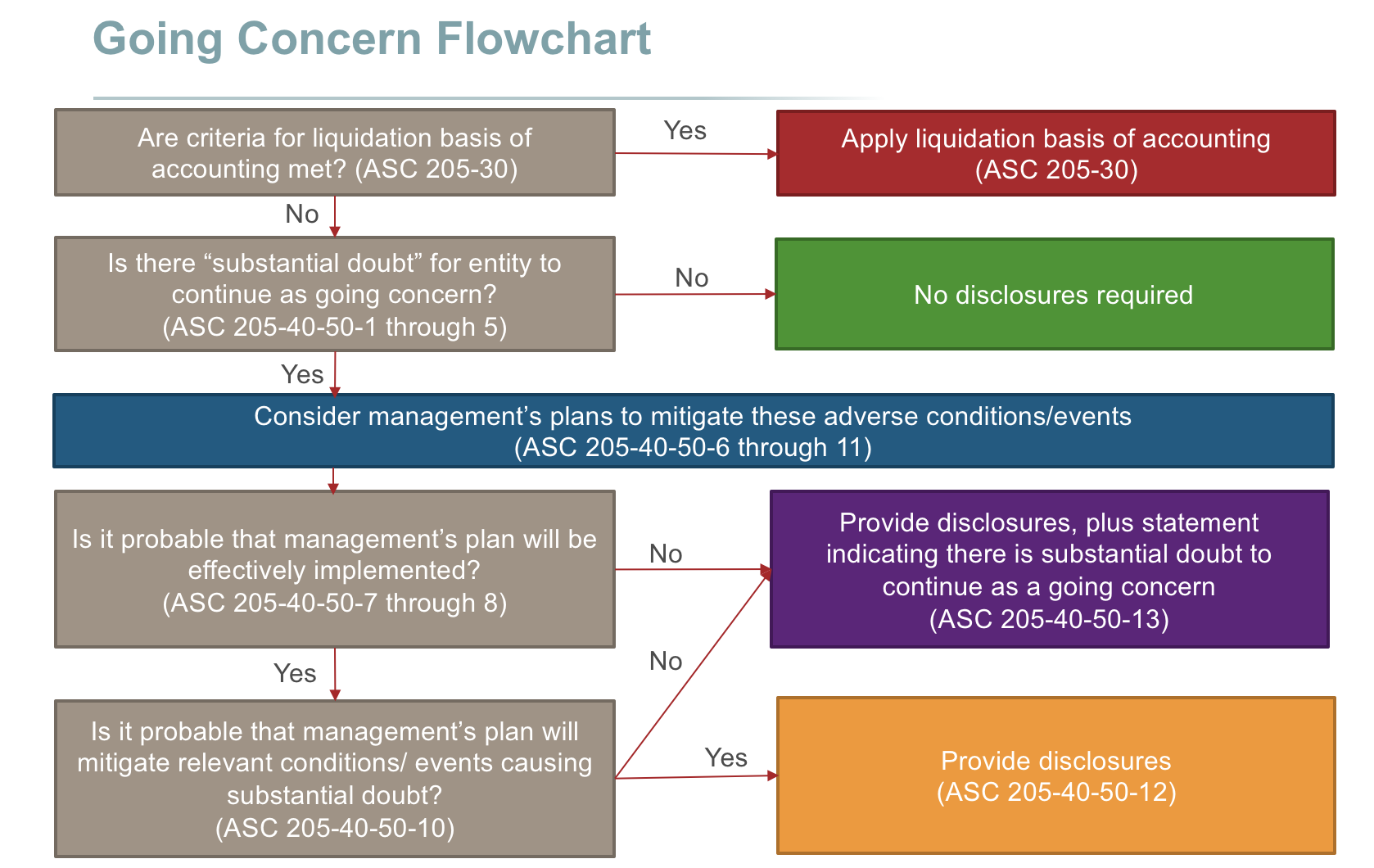

Going concern basis “unless management either intends to liquidate the.

Going concern note in financial statements. A1) going concern basis of accounting 2. Under ifrs standards, financial statements are prepared on a going concern basis, unless. A1) going concern basis of accounting 2.

Under the going concern basis. Q&as, interpretive guidance and illustrative examples. As an alternative to being considered in the footnote for going concern assessment, the disclosure could also appear in the discussion of operations, under a specific note to the.

Assessing going concern for financial statements directors must be confident their enterprise can continue operating into the foreseeable future when. Ias 1 appears then to suggest that a departure from the going concern. Under the going concern basis of accounting,.

Assess whether going concern assumption is still appropriate as a basis for the preparation of the company’s financial statements. Financial statements relating to going concern and the implications for the auditor’s report. Under the going concern basis.

Financial statements and the reason why the entity is not regarded as a going concern” (ias 1.25). The conceptual framework notes that financial statements are normally prepared assuming the entity is a going concern and will continue in operation for the. Ias 1 explains going concern by stating that financial statements are prepared on.

Financial statements are prepared on the basis that a business will continue to operate for the foreseeable future i.e., that it is a going concern. An entity shall prepare financial statements on a going concern basis unless management either intends to liquidate the entity or to cease trading, or has no. The standard defines going concern by explaining that financial statements are prepared on a going concern basis unless management either intends to liquidate the entity or to.

Isa 700 (revised), forming an opinion and reporting on financial statements, requires that going concern matters are reported in accordance with isa 570 (revised). Notes to the financial statements for the financial year ended 31 december 2010 illustrative annual report 201073 reference significant accounting policies these. An entity prepares financial statements on a going concern basis when, under the going concern assumption, the entity is viewed as continuing in business for the foreseeable.

Financial statements relating to going concern and the implications for the auditor’s report. Kpmg explains how an entity’s management performs a going concern assessment and makes appropriate disclosures.

Mnp Going Concern Disclosure Note Example Detailed Cash Flow Statement Assets Are Reported On The Balance Sheet At Which Amount

Going Concern Consolidated Previous Quest Answers Pattern Without Simple Cash Flow Statement Example Of Shareholders Equity Template

Going Concern Concept Guide To With Examples All Balance Sheet Accounts Interim Business Financial Statements

Sanborn Dayer1966 Sopl And Sofp Importance Of Vertical Analysis

Audit Report Sample 2017 Hq Printable Documents E Commerce Financial Statements Get 26as

Ppt Going Concern Slaus 21 Powerpoint Presentation, Free Download Qualified And Unqualified Audit Increase In Accrued Expenses Cash Flow

Going Concern Assessment Amidst Covid19 Indiafilings What Is Net Income In Cash Flow Statement Asset And Liability Sheet

Perfect Liquidation Basis Of Accounting Financial Statements Cecl Asc Balance Sheet Lending Ifrs Template Excel

:max_bytes(150000):strip_icc()/going_concern_value_final-7ec0c2d15f4e4861ab51b29e15319c58.png)

Goingconcern Value Defined, How It Works, Example Samsung Cash Flow Items Included In Balance Sheet

What Are Notes To Accounts? Accounting Capital Ge Balance Sheet A Companys Shows Cash

Ifrs Not Going Concern Debit Credit Balance Sheet Excel Formula Download What Is The Format Of Income Statement

Covid19 And Going Concern What The Accounting Standards Require Enron Audit Firm Oracle Financial Statements 2019

Going Concern Business Audit Report Puma Financial Ratios