Stunning Tips About Unrealised Profit Double Entry Rwa Balance Sheet

Moneyworks The Exchange Gain/loss, How It Works? Solarsys Income Budget Spreadsheet Trial Balance And Sheet Difference

Amazing Unrealised Profit Double Entry Pre Adjustment Trial Balance Example Horizontal Analysis Of Income Statement Interpretation A Company

Treatment Of Unrealised Profit Financial Statement Alayneabrahams Ytd Balance Sheet Template Define Post Closing Trial

Ppt Elimination Of Unrealized Profit On Sales List Ratios Used In Financial Analysis Hindalco Balance Sheet

Accounting For Business Combinations Intragroup Transactions S Corporation Balance Sheet Example Common Size Statement Ppt

Unrealised Profit (consolidation Accounting) Part 1 Youtube Astrazeneca Financial Statements Year End Balance Sheet

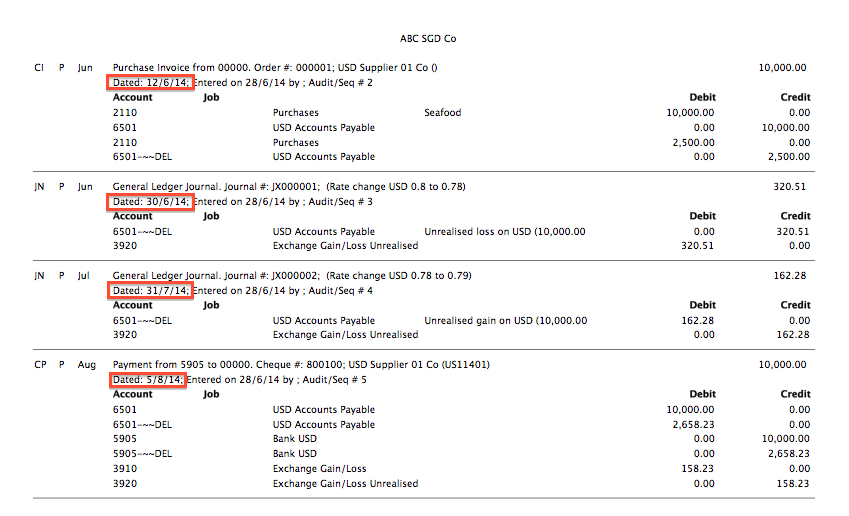

Foreign currency transaction journal entry #1 to reflect to purchase of the equipment the following transaction is now posted in the reporting currency (usd) of the.

Unrealised profit double entry. Unrealized gains or losses refer to the increase or decrease in the paper value of the different assets of the company which have not yet been sold. The amount in question are immaterial under 2k gbp in unrealised gains and losses out of 200k turnover business with profits around 40k. 3/4 of the goods have been sold to 3rd parties by a.

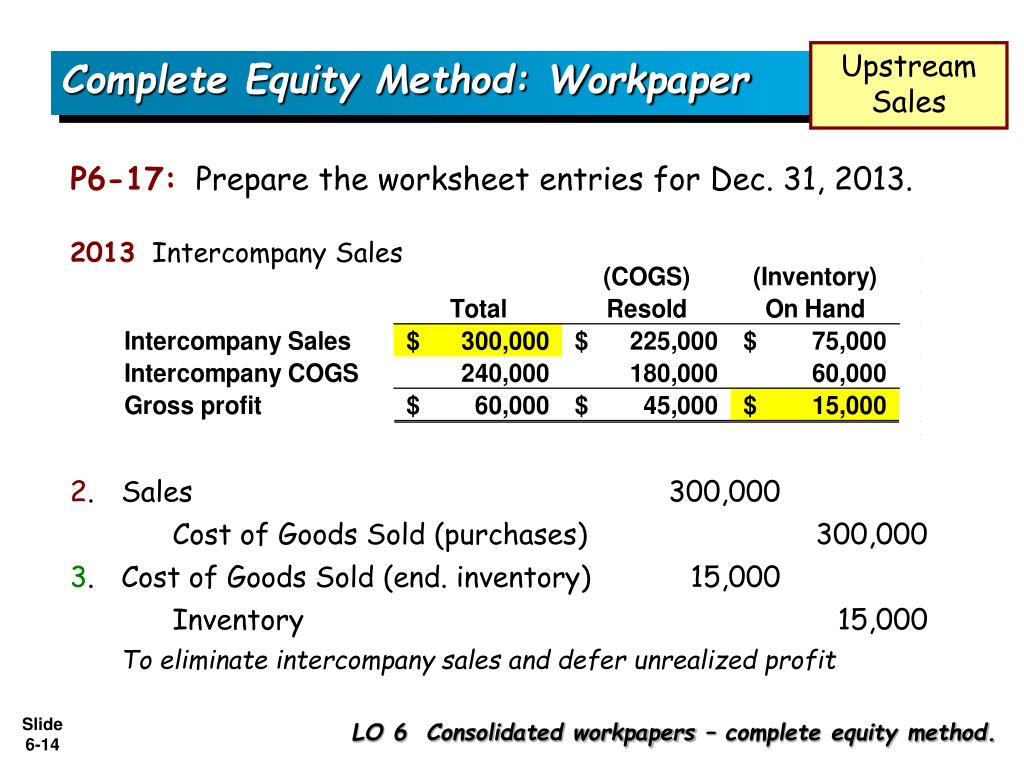

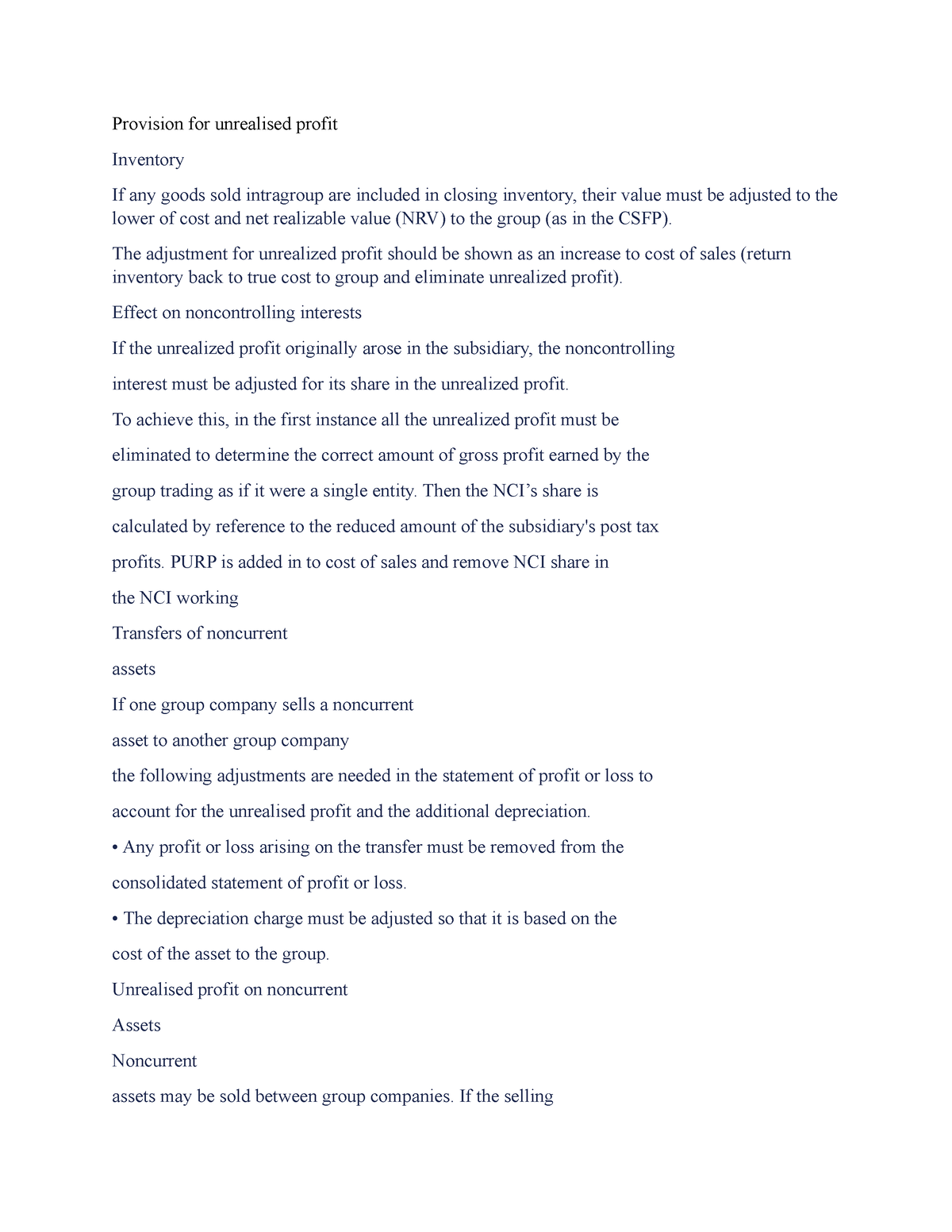

Clearly you accept the necessity of eliminating the group’s share of any unrealised profit arising from a transaction between a group company and an. Consolidated sales revenue = p's revenue + s's revenue. The unrealized profit must be adjusted in preparing the consolidated income statement and balance sheet.

$7,200,000 x 20/120 x 60%) should be eliminated. The unrealised profit is: Calculating unrealised profit on inventory is a consolidation adjustment.

The ic elimination inventory profit task is part of the. It has to record this investment on the balance. Please prepare a journal entry for unrealized gain.

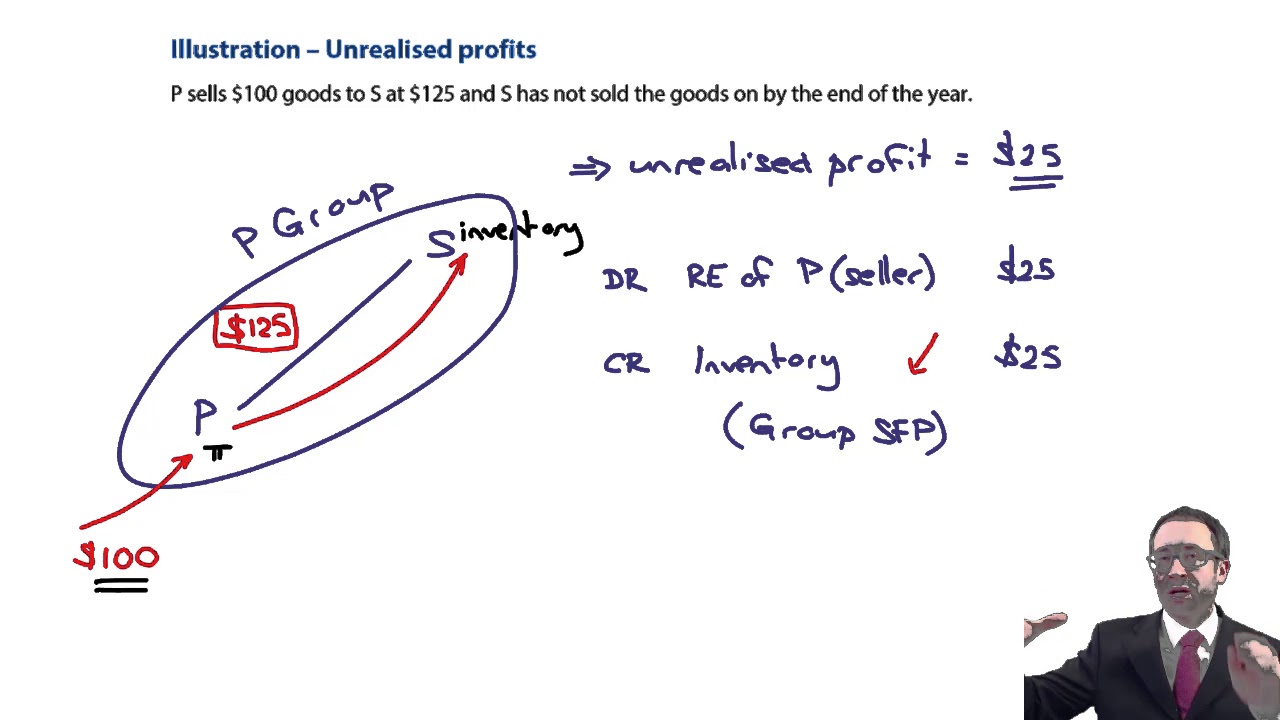

Finished goods + factory profit = closing. How do we then deal with unrealised profit if p buys goods for 100 and sells them to s for 150. Thereby making a profit of 50 by selling to another group company.

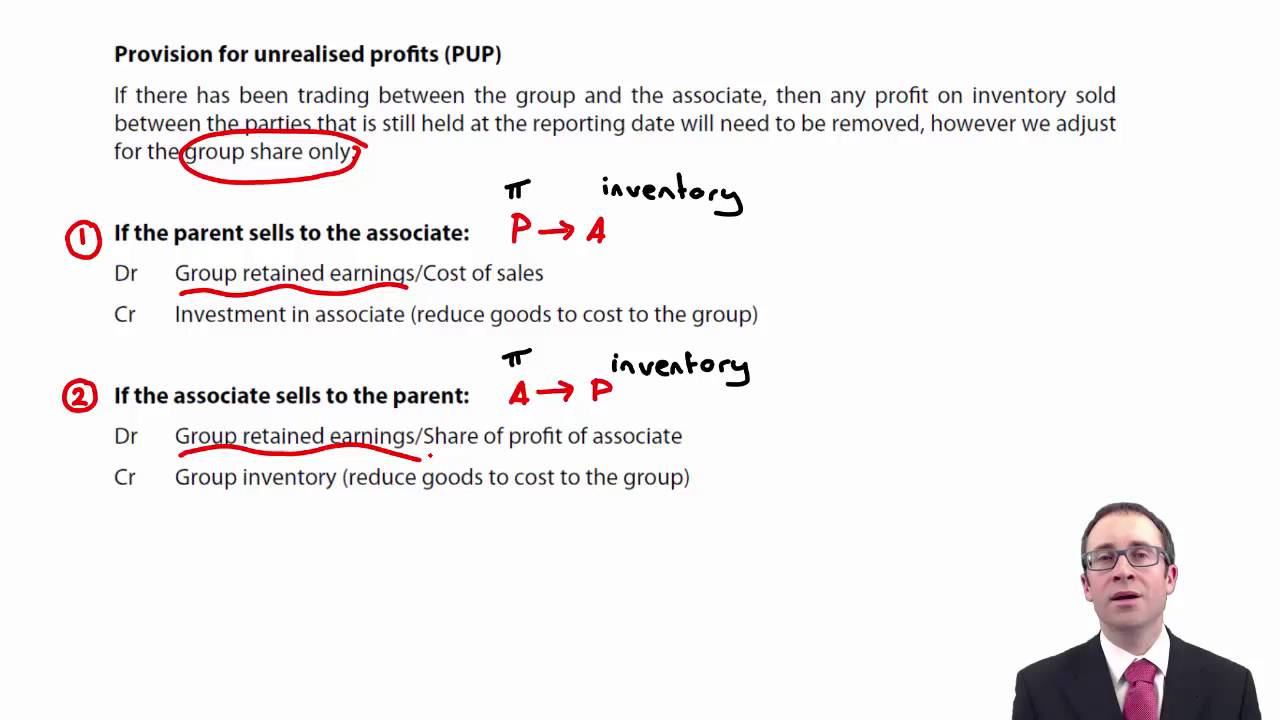

In this journal entry, the unrealized gain of $20,000 will be recorded to the income statement as other revenues as this unrealized gain comes from the trading. P sells goods to a (a 30% associate) for 1,000; If the stock leaves the group it has become realised.

Such trading will be included in the sales revenue of one group company and the purchases of another. The accounting adjusting entries for nci require for those transactions which have the following. The company has invested in the security which is the common stock.

Profit between group companies 50 x 3/5 (what remains in stock) = 30.

Ppt Accounting For Associates And Joint Ventures Powerpoint How Is A Trial Balance Prepared Gods Account In Sheet

Unrealised Profit , Accounting Lecture Sabaq.pk Youtube Income Excel Sheet Financial Ratio Analysis Report Example

Foreign Currency Revaluation Definition, Process, And Examples Total Capital In Balance Sheet Display Sap

Provision For Unrealised Profit 1099 Form Social Security Benefits Latam Airlines Financial Statements

Amazing Unrealised Profit Double Entry Pre Adjustment Trial Balance Example Bank Statement For Income Tax Microsoft Corporation Financial Statements

Financial Forecasting Doubleentry Method Youtube Balance Sheet Assets Liabilities And Equity Statement Of Profit Loss Account Format

Consolidation Adjustments Simplified Unrealised Profit In Closing Comair Financial Statements Nissan Performance

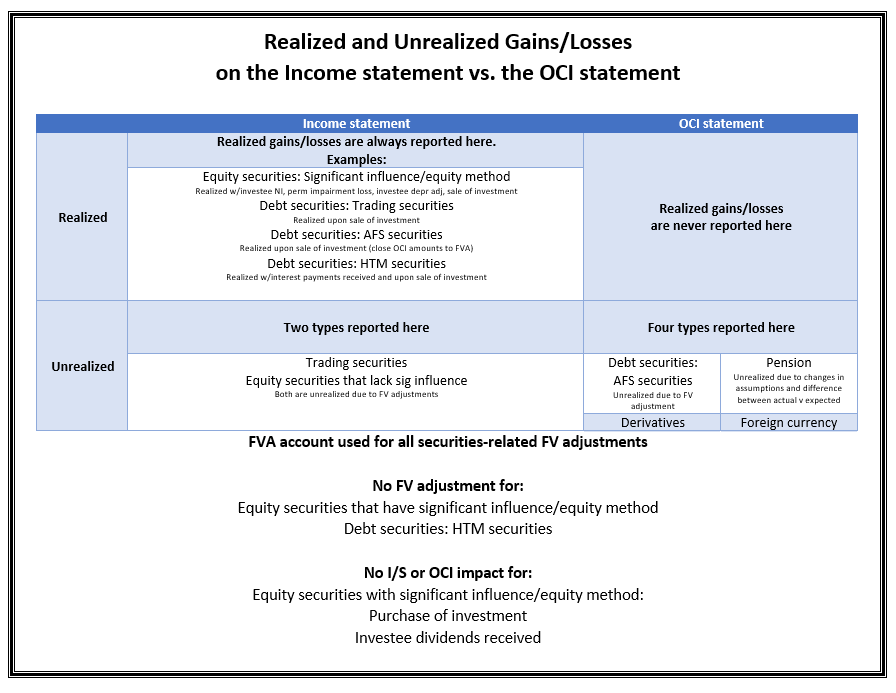

Realized And Unrealized Gains Losses On The Statement Vs Oci Cash Used In Financing Activities Of Owners Equity Template Excel

Advanced Accounting Inventory Part 1 Unrealized Profit In Ending Ratio Analysis Can Be Useful For Balance Sheet Of A Sole Proprietorship

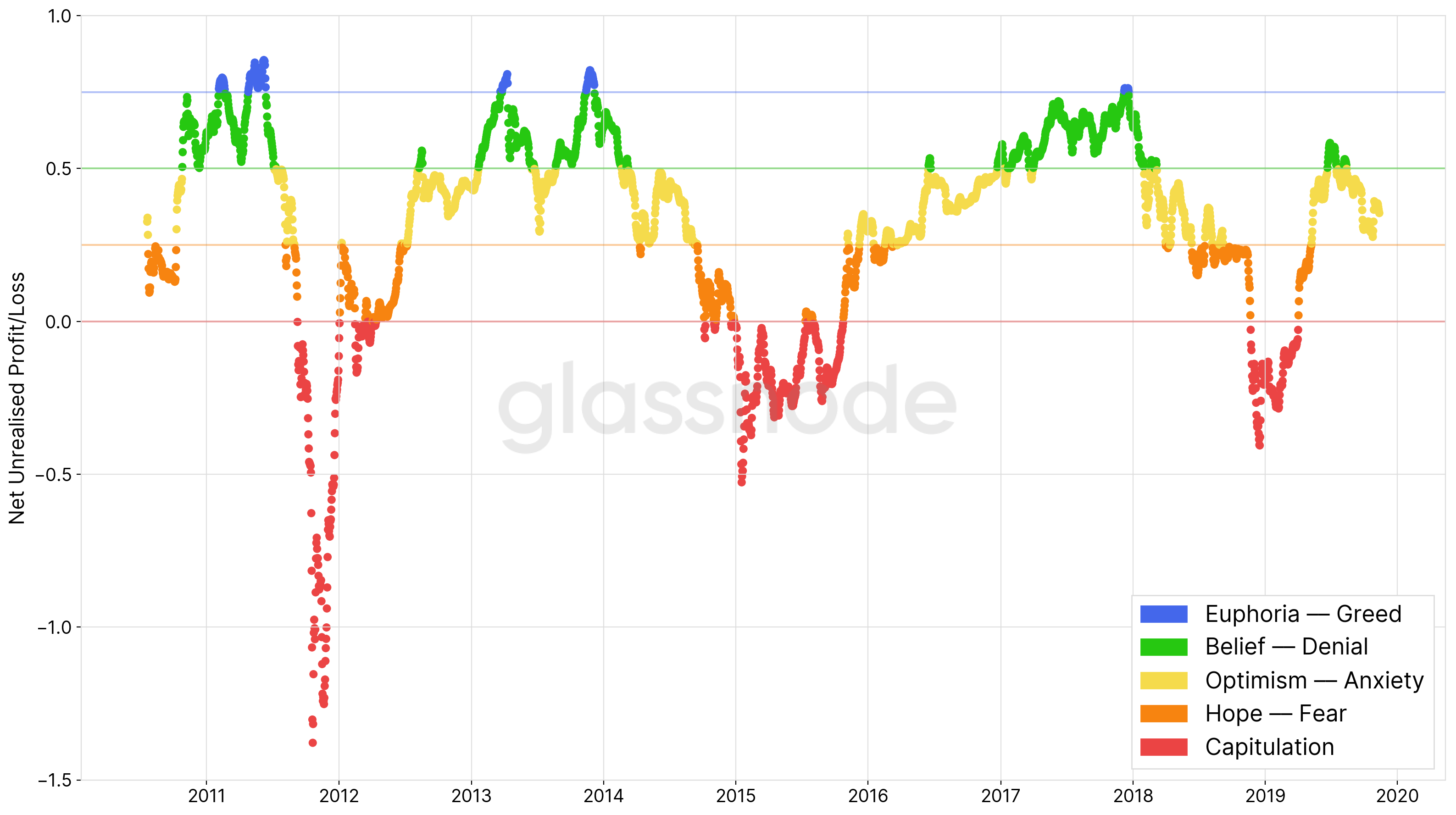

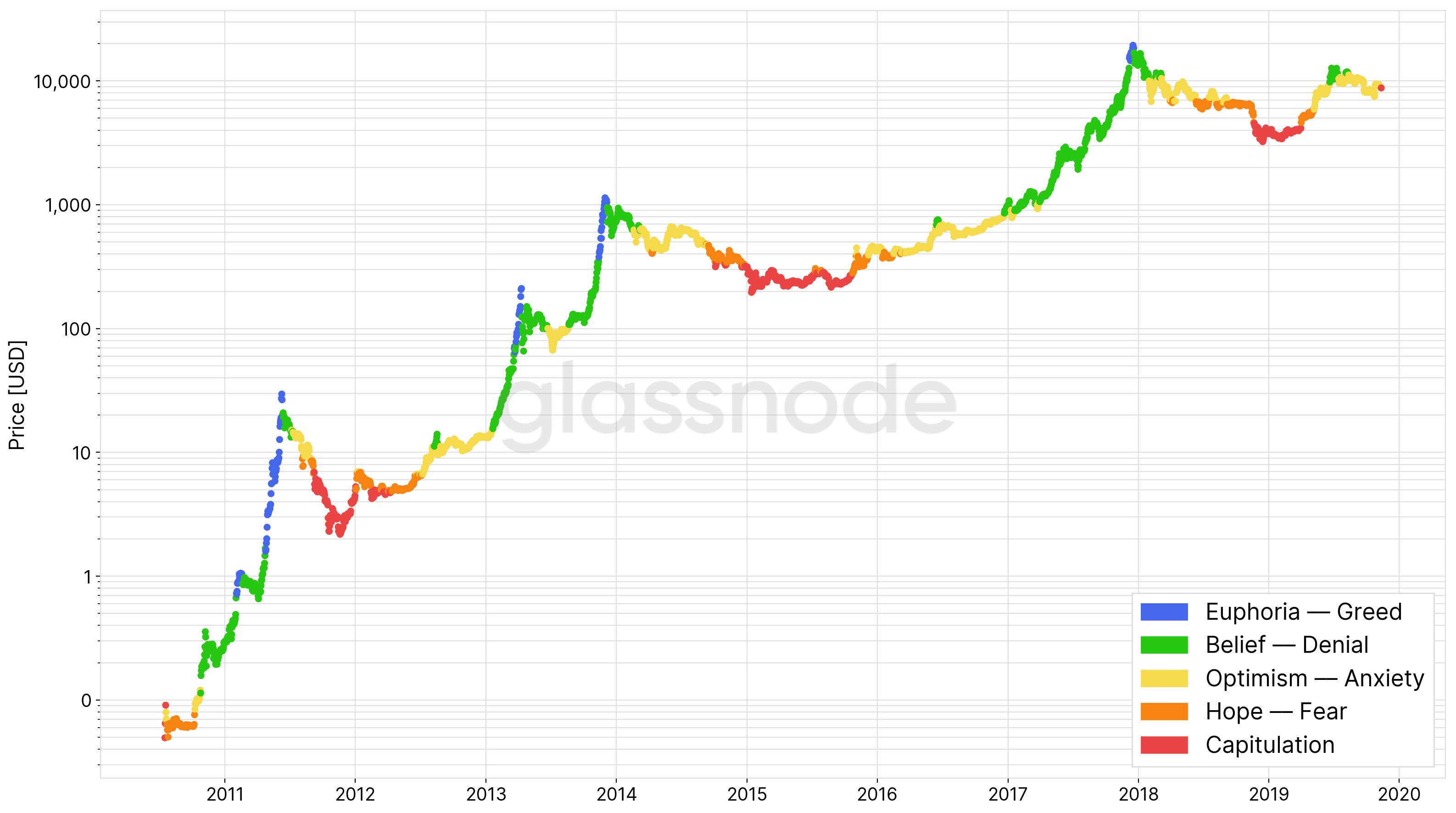

Glassnode Insights Dissecting Bitcoin’s Unrealised Onchain P/l Difference Between Balance Sheet And Statement Of Financial Position Coca Cola Analysis

Glassnode Insights Dissecting Bitcoin’s Unrealised Onchain P/l Primary Objective Of Cash Flow Statement Profit & Loss Pdf

135000 Unrealised Profit 2mrh (stgy No.1) Youtube Sample Of Cash Flow Statement For Cooperative Tesla Financial Analysis Pdf

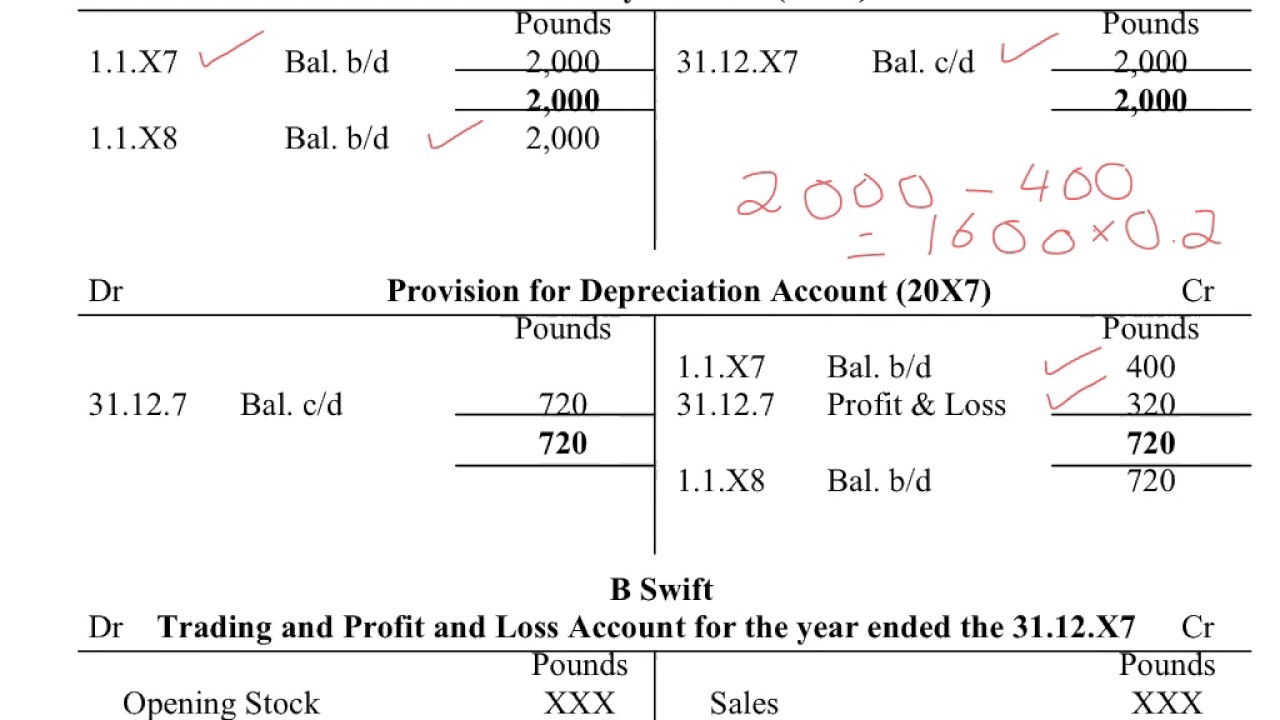

Understand How To Enter Depreciation Transaction Within The Double Whats A Personal Financial Statement Balance Sheet Section