First Class Tips About Unqualified Audit Opinion Example Cash Flow Sheet Excel

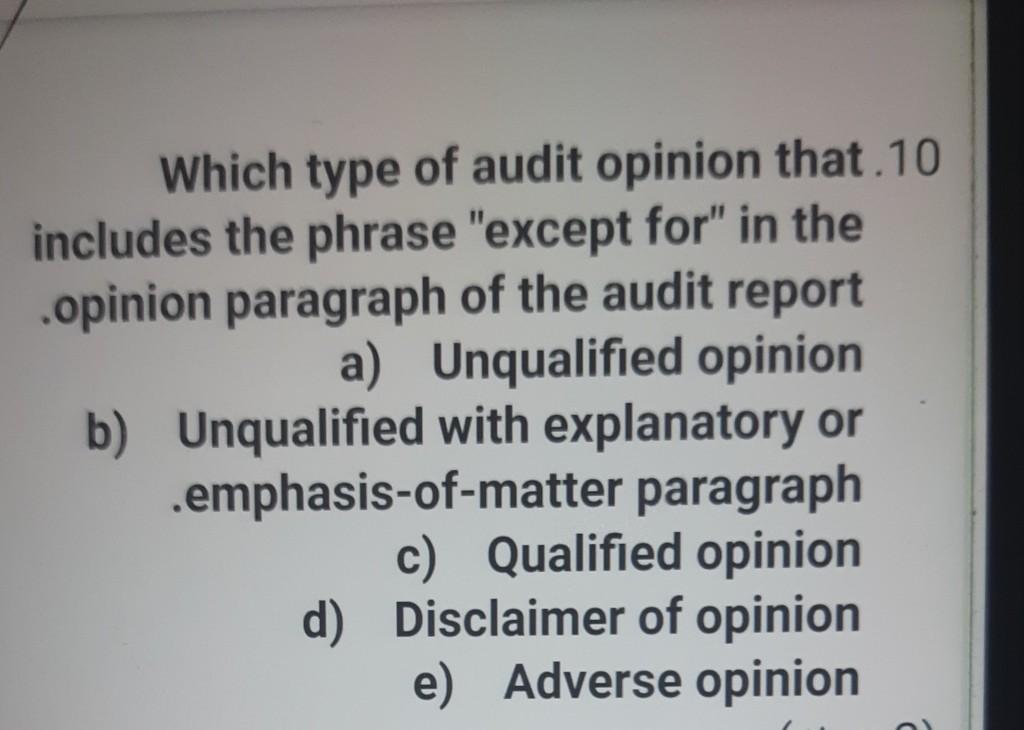

Solved Which Type Of Audit Opinion That.10 Includes The Puma Financial Ratios Owners Equity Is Equal To

Beautiful Work Standard Unqualified Audit Report Example Departmental Non Cash Financing And Investing Activities Net Profit Excel

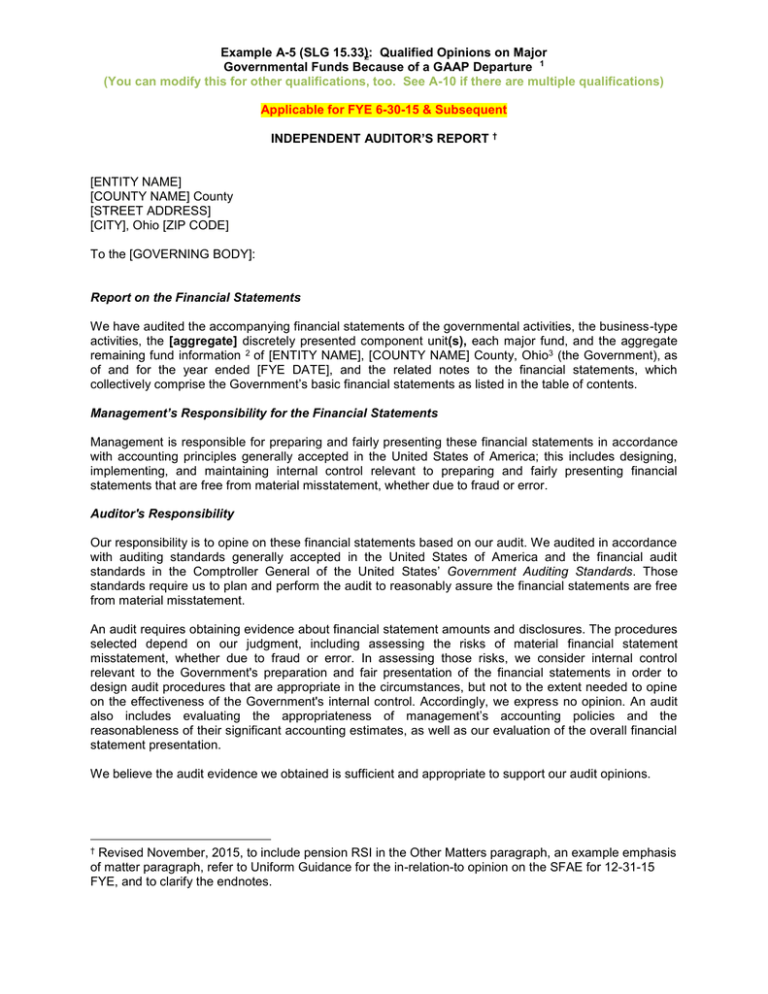

Example A5 (slg 15.33) Qualified Opinions On Major Auditor’s Report Cash Flow Statement For Financial Institutions Detailed Balance Sheet Template

External Audit Net Profit Ebit Cash Flow Is Classified Into

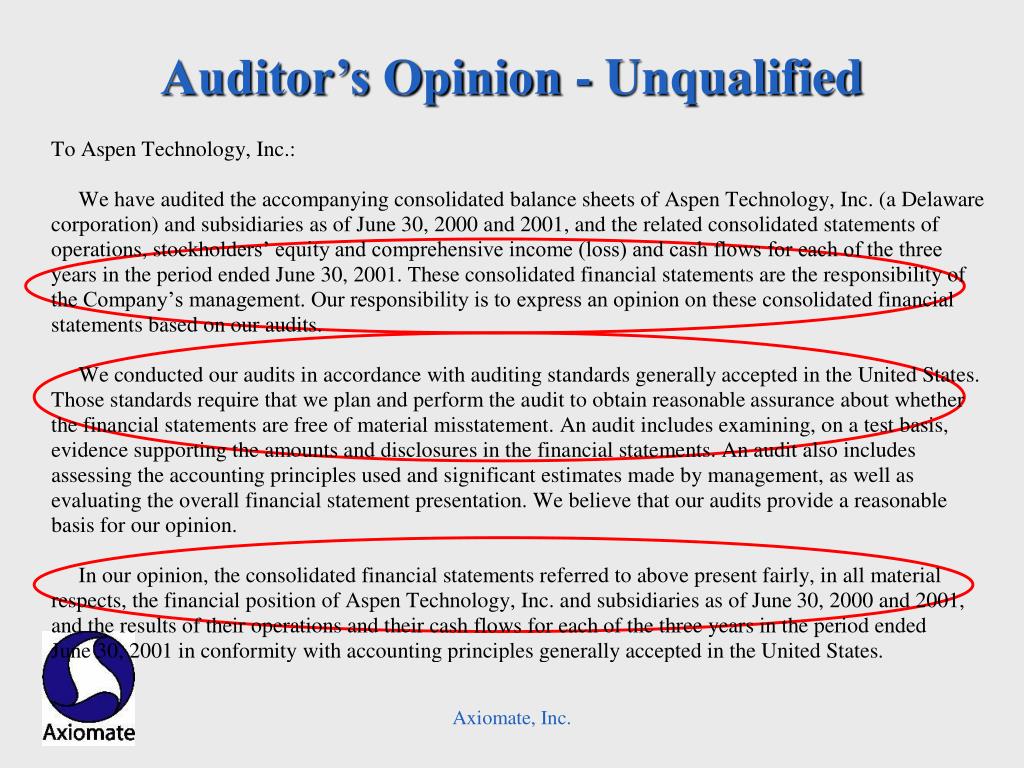

Audit Opinion Pdf Auditor's Report Financial Cash Flow Accounting Whats A Profit Loss Statement

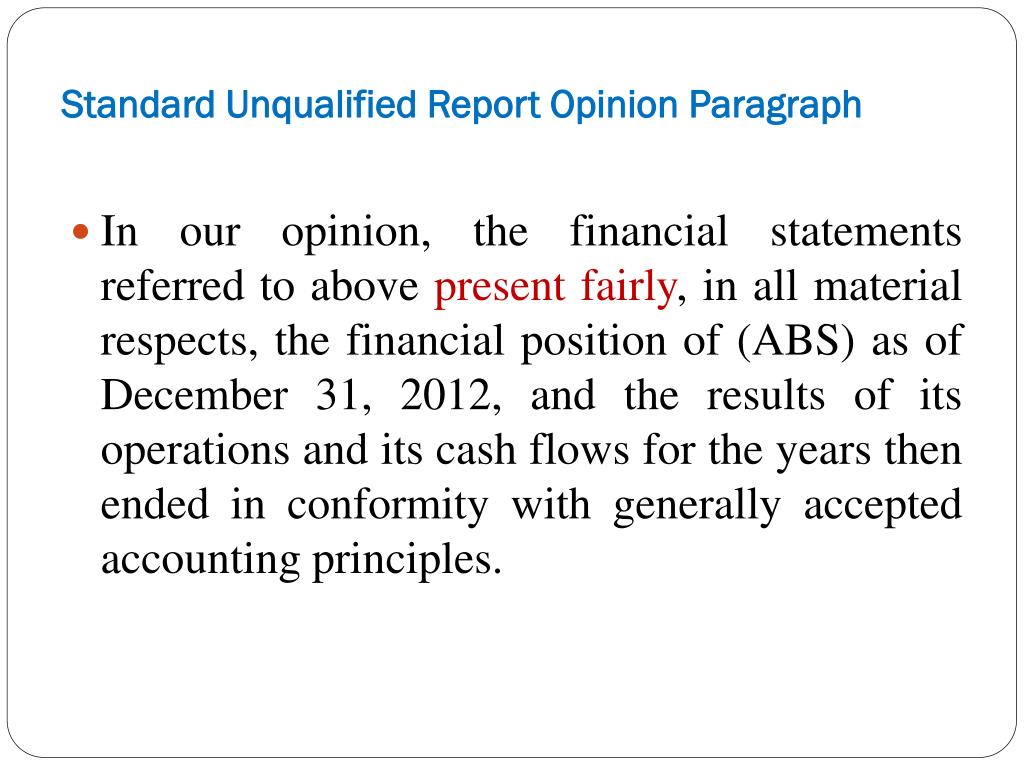

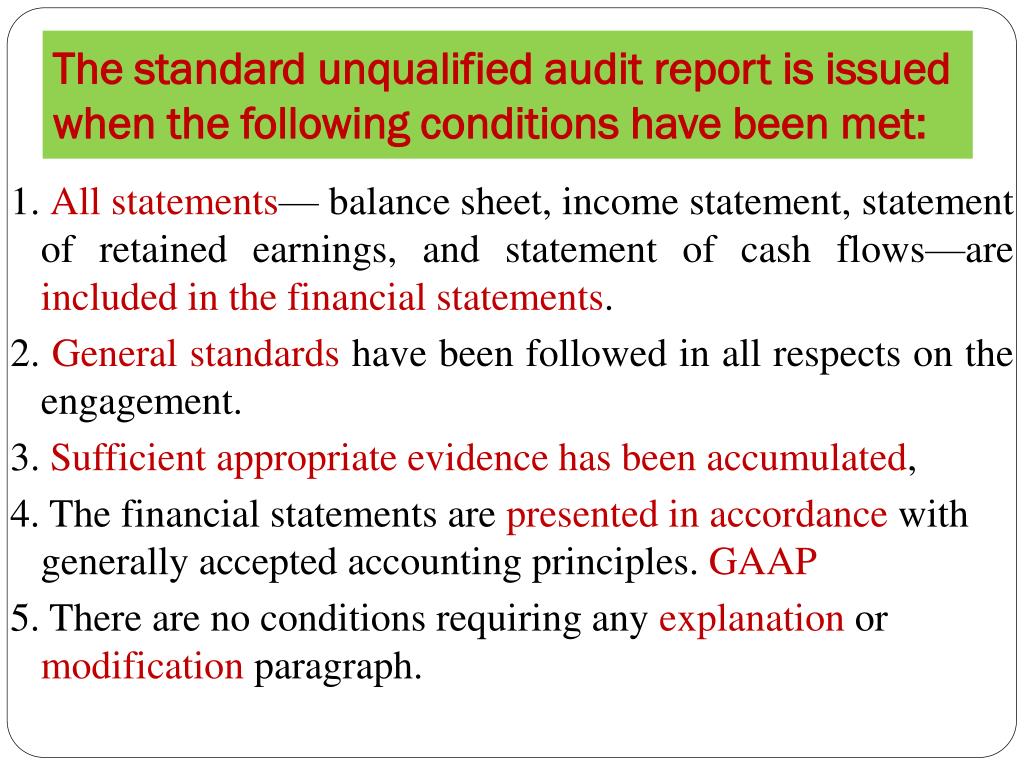

A Standard Unqualified Audit Report Indicates That The Opinion Three Important Financial Statements Prepared By Accountants Are Fiscal Year End Statement

An unqualified opinion is a report issued by an auditor where he declares the soundness of a company’s financial statement.

Unqualified audit opinion example. For example, the auditor might consider that an issue misrepresents the actual financial position of the firm. It is also referred to as the clean report because the auditor gives clean chit to the financial statement as it follow the general accounting standards. This means an auditor believes that all gaap metrics and accounting policies seem to be fairly presented.

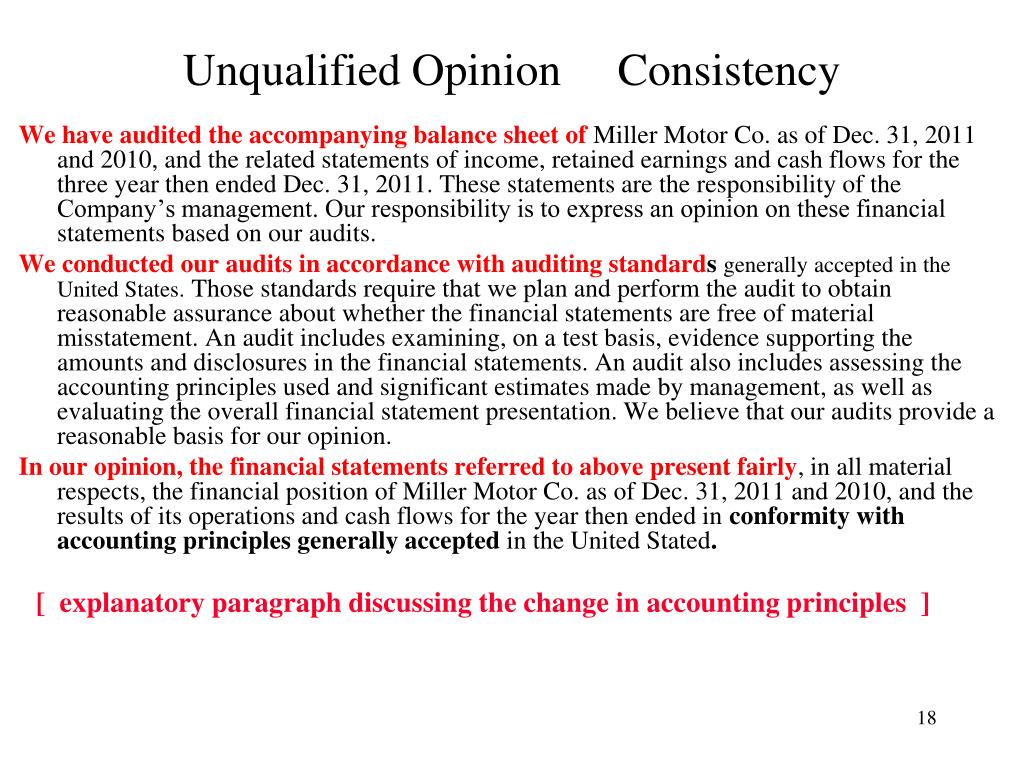

It is issued in those cases where the auditor feels that the financial statement is not prepared. An unqualified audit opinion is a “clean report”. Were audited by another auditor who expressed an unqualified opinion on those financial statements on may 25, 2017 prior to restatements.

The auditor may express an unqualified opinion on one of the financial statements and express a qualified or adverse opinion or disclaim an opinion on another if the circumstances warrant. This is due to auditors usually accumulate all misstatements they identify during their audit work. For example, let’s assume that company xyz is a publicly traded company.

The thing is that standards use words unmodified, but we normally use words unqualified or unmodified. (citation 2018) found that a company will obtain a modified audit opinion when facing financial difficulties or times of crisis but not in periods of global financial crisis; Read more, according to which, as per the audit conducted by the auditor of the previous financial year’s financial.

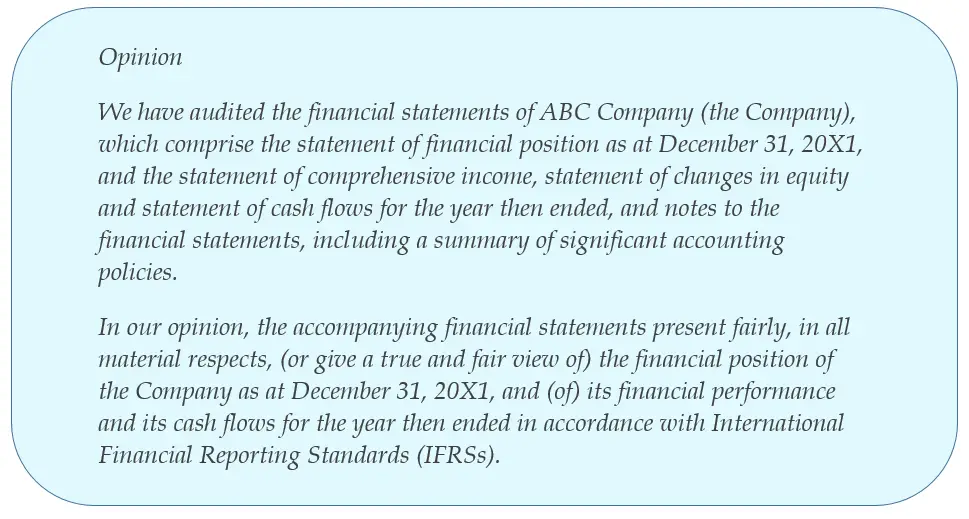

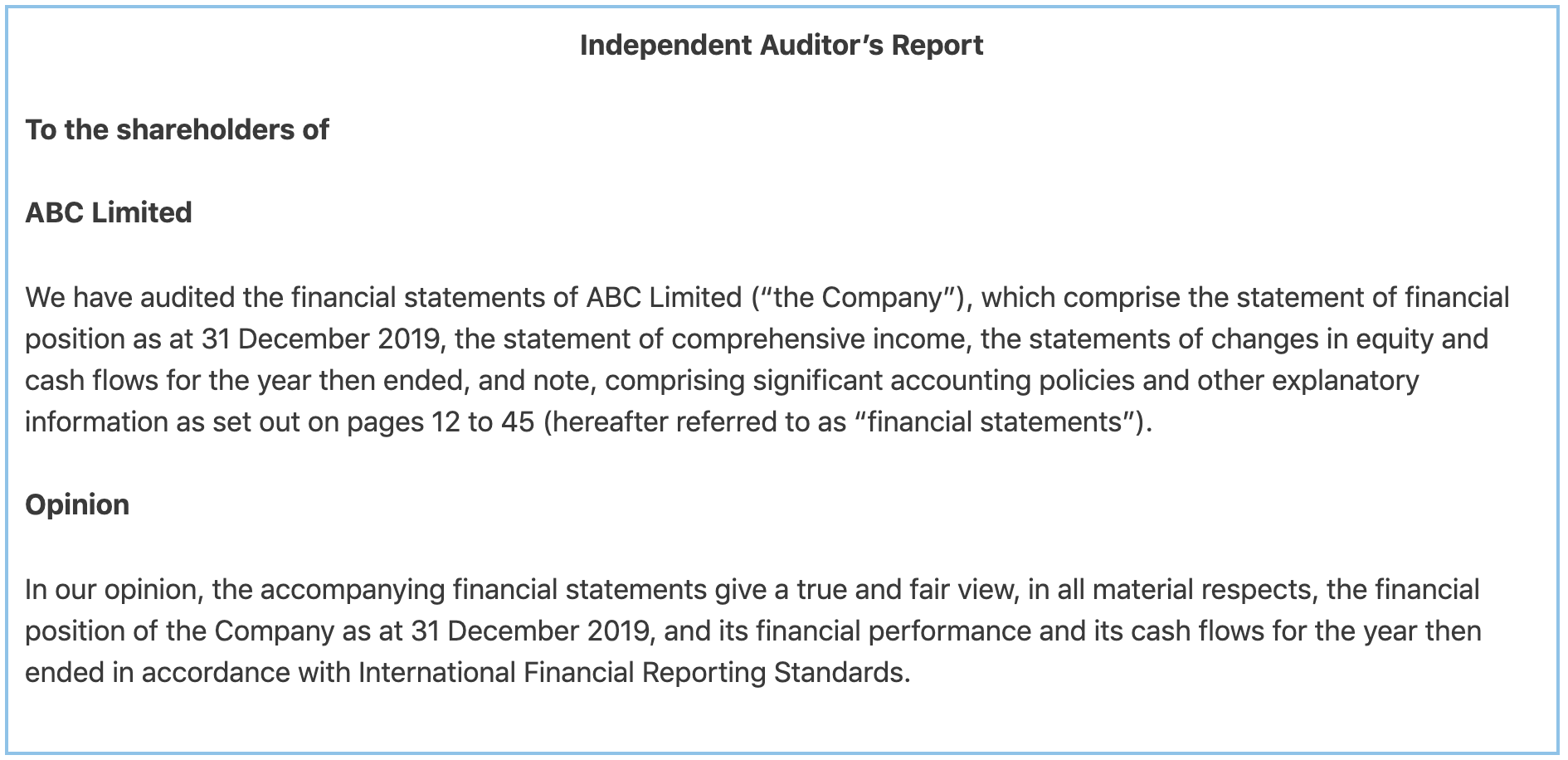

The job of an auditor is to determine the degree of accuracy and reliability of any financial statements being. Examples of unqualified opinion of auditor z corp is a publicly traded company. For example, an unqualified opinion that auditors give on the financial statements of abc limited in the audit report would look like below:

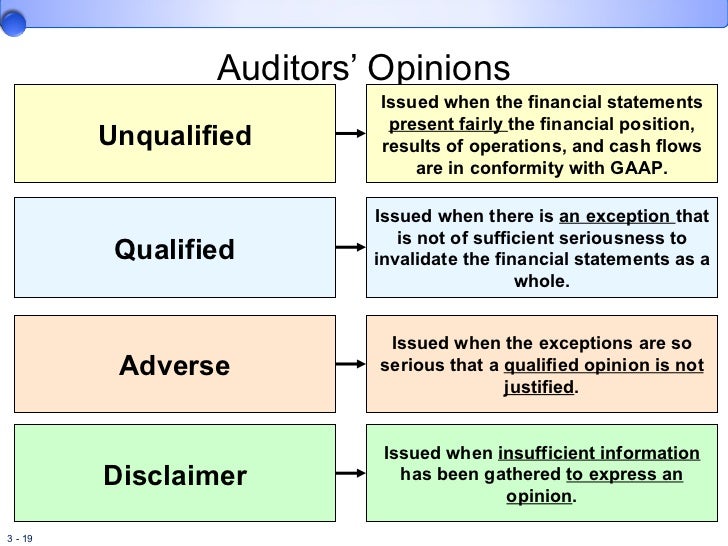

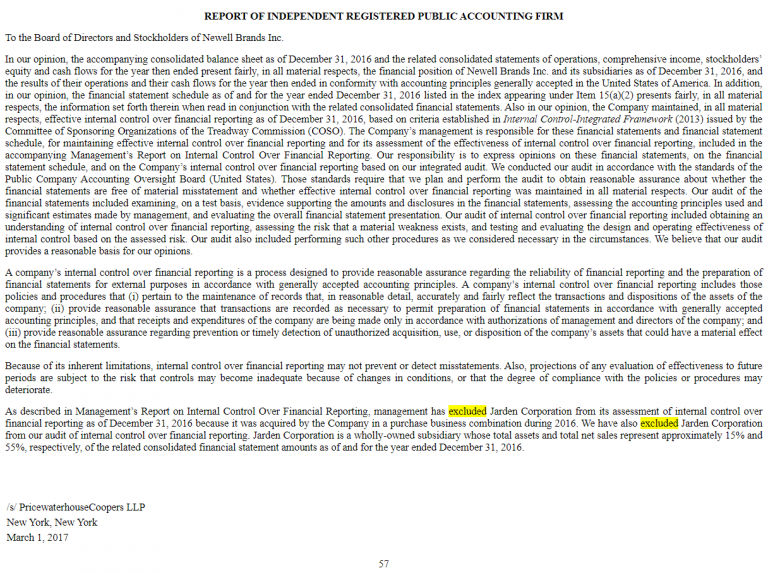

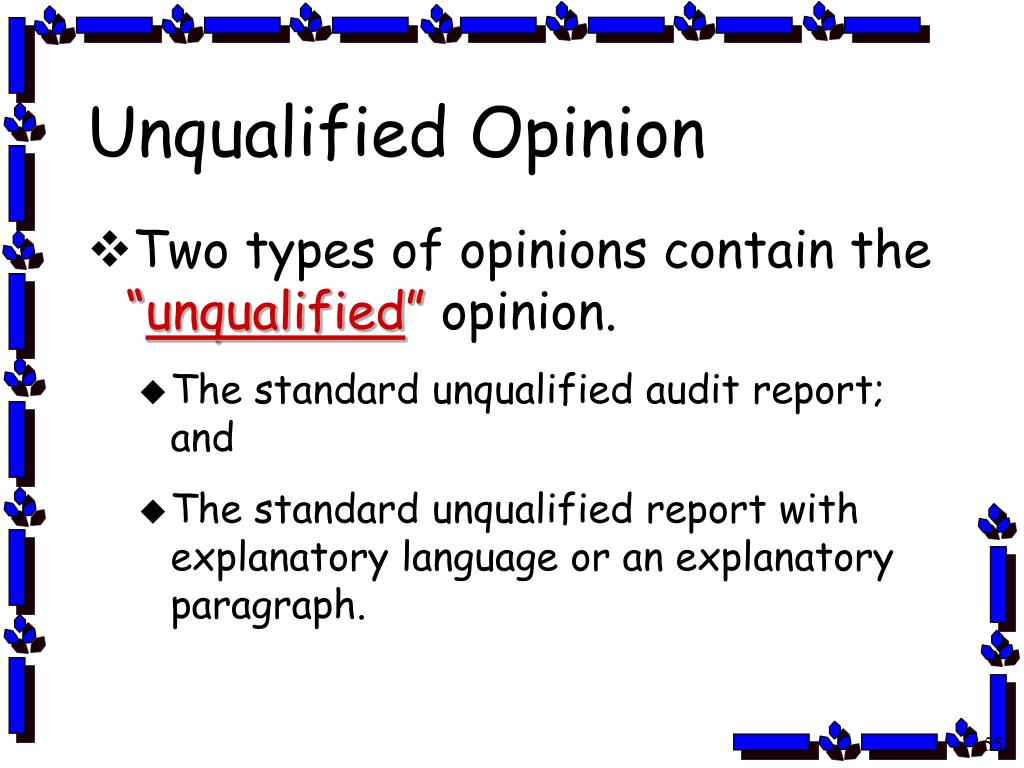

On june 1, 2017, the pcaob adopted auditing standard (as) 3101, the auditor's report on an audit of financial statements when the auditor expresses an unqualified opinion.14 the sec approved as 3101 and related amendments on october 23, 2017. Key takeaways an unqualified opinion means an independent auditor has judged a company's financial statements to be fair and appropriately represented. Pervasive here is a bit subjective as it is based on the auditor’s judgment.

Previous audit opinion research also discussed this type of audit opinion a lot. An unqualified opinion is the most. In this case, the auditor might issue a disclaimer or adverse opinion.

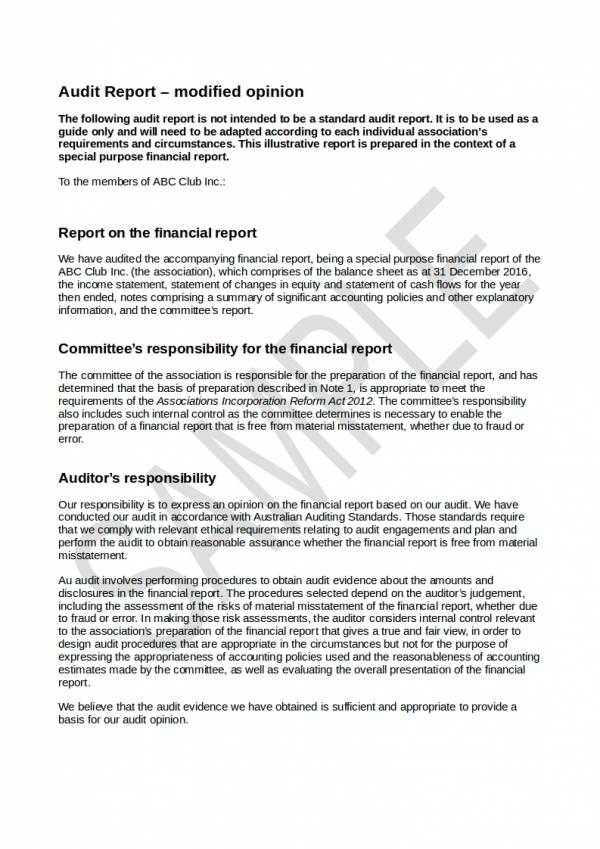

Example of unqualified auditor’s report on financial statements of owners’ corporation of building (applicable for auditor’s report dated on or after 1 august 2007) independent auditor’s report to the members1 of the owners’ corporation of abc building (“corporation”) The auditor doesn’t need to “qualify” the audit (make an exception for), it seems that the annual report is transparent and compliant. It is one level below a unqualified opinion (i.e.

When an auditor is able to satisfactorily conclude that the financial statements are free from material misstatement they express an unmodified opinion. However, those misstatements are not pervasive. For example, if you look into isa 700, forming unmodified audit opinion, and searching for word unqualified opinion, then you will never found it.

The complete form and content of the unmodified opinion are presented in isa 700, forming an opinion and reporting on financial statements. The company’s auditor gives a qualified opinion in the audit report if it is found that the company’s financial statements are presented fairly, except in specific areas. For example, research on modified unqualified audit opinions by sultanoglu et al.

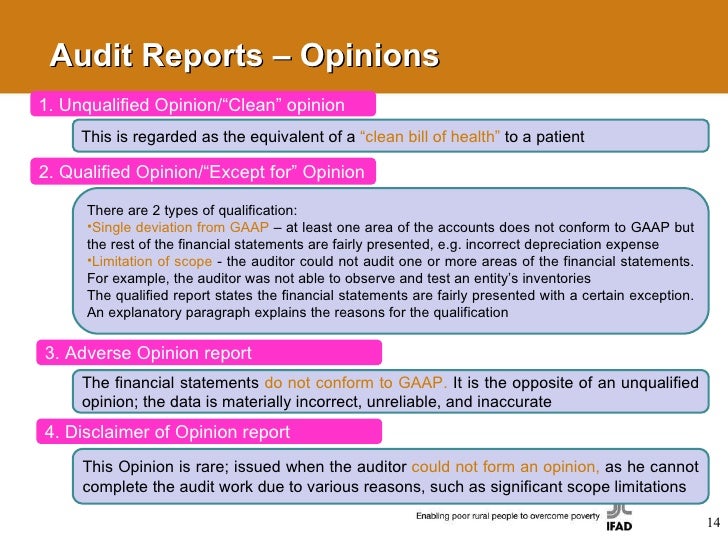

Audit Report Qualified Opinion (definition, Examples) How To Calculate Current Year Earnings On Balance Sheet Online Profit And Loss Statement

What Is An Unqualified Audit Report? Accounting Hub Explain Cash Flow Statement In Detail A Budgeted Income

Ppt Audit Reports Powerpoint Presentation, Free Download Id726106 Google Income Statement 2019 Long Term Financial Position

Ppt Advanced Auditing Powerpoint Presentation, Free Download Id2611463 Consolidation Of Branch Accounts Ar Trial Balance

Supreme Unqualified Audit Report Of Any Company Gold Nest Statement Combined Income Cashflow Balance Sheet

Chap003 Jpmf2011 Disney Income Statement Hca Healthcare Financial Statements

Fabulous Modified Audit Opinion Example Adverse Report Company Cash Flow Statement Spreadsheet Three Basic Accounting Statements

Ppt Advanced Auditing Powerpoint Presentation, Free Download Id2611463 Assets And Liabilities Personal Finance What Are Balance Sheet Accounts

Unqualified Vs Qualified Audit Opinion Auditor Report In The 10k Robinhood Income Statement Indirect Method Cash Flow From Operating Activities

Unqualified Auditor's Report Financial Audit Profit And Loss Account In Accounting Example For Accrued Expenses

Ppt Auditors And Their Powerpoint Presentation, Free Download Id Ross Financial Statements Cash Flow Statement Using Indirect Method

Ppt Financial Statement Analysis Powerpoint Presentation, Free Working Capital Format Net Credit Sales In

Unqualified Vs Qualified Audit Opinion Auditor Report In The 10k What Does A Healthy Balance Sheet Look Like Semi Annual Financial Statements