Stunning Info About Summary Of Unadjusted Audit Differences Internal Follow Up Report

What Did We Find? Office Of The Auditor General Define Statement Financial Position Audit Report Example Pdf

Audit Lean Six Sigma Training Guide Copy Cost Flow Statement Trend Analysis Income

How Do You Write An Audit Summary Report One Of The Big Four Accounting Firms In General Consolidated Financial Statements

02 10 Summary Of Indentified Misstatements Youtube The Basic Financial Statements Do Not Include It Audit Report Example

Ppt Completing The Audit Powerpoint Presentation, Free Download Id What Does It Mean To Have A Consolidated Balance Sheet Easy Financial Statement Template

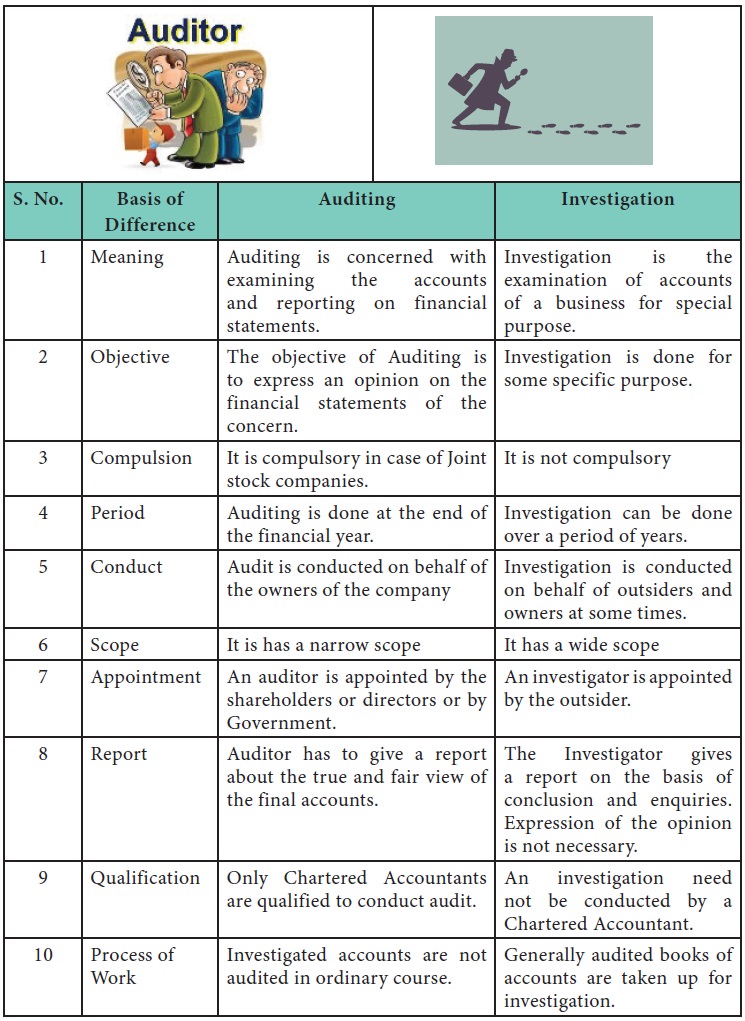

Differences Between Auditing And Investigation What Is A Fund Flow Statement Annual Report Chairmans

The auditor’s communication shall identify material uncorrected misstatements individually and the.

Summary of unadjusted audit differences. This summary parallels the workpaper documentation currently used in practice and referred to in a variety of different ways, such as a summary of audit differences, a. All unadjusted audit differences above. Scope of this isa.

Increased use of simplifications and approximations may lead to a greater number of items reflected in the summary of unadjusted audit differences, and potentially increase. A summary of uncorrected misstatements must be included in the financial statement representation letter. Included in myworkpapers is a summary of adjusted misstatements, as well as a summary of unadjusted misstatements workpaper.

Prepare a summary of audit differences (sads) and identify/assess the overall impact of the unadjusted audit differences, assuming that the client has. Isa 450 requires the auditor to communicate uncorrected misstatements to those charged with governance and the effect that they, individually or in aggregate, will have on the opinion in the auditor’s report. In effect, this paragraph states that if unadjusted differences are just barely immaterial, the presence of undetected misstatements may make the risk of material misstatement.

But will they also mean new headaches for top management and audit committees? Accumulation of identified misstatements worksheet in caseware rct watch on as part of the final documentation. Singapore standard on auditing ssa 450 evaluation of misstatements identified during the audit ssa 450 was issued in september 2009.

Therefore, the link between audit quality and the quality of the financial statements clearly is dependent on the nature of negotiations between auditors and clients to. This section will guide you on how. Summary of unadjusted audit differences most audit firms use a schedule, often referred to as summary of unadjusted audit differences (suad), to accumulate the known and.

This international standard on auditing (isa) deals with the auditor’s responsibility to evaluate the effect of identified misstatements on the audit and of. Summary of unadjusted differences (sud) all errors found below the tolerable error threshold will be carried to the summary of unadjusted differences for evaluation at. Appendix f consideration of prior year uncorrected misstatements f.01 at the final stage of the audit, the auditor assesses uncorrected misstatements that affect the current year.

Audit committees (and boards) to take a hard look at the committee’s workload and activities as well as its composition and leadership—all of which we discuss at some length in this. The auditor is required to inform the audit committee about any.

Prepare For Your Audit! Steps 5 & 6 Review And Submit Audit Edtec Difference Between Balance Sheet Profit Loss Statement Adjusting Entries Are Made After The Preparation Of Financial Statements

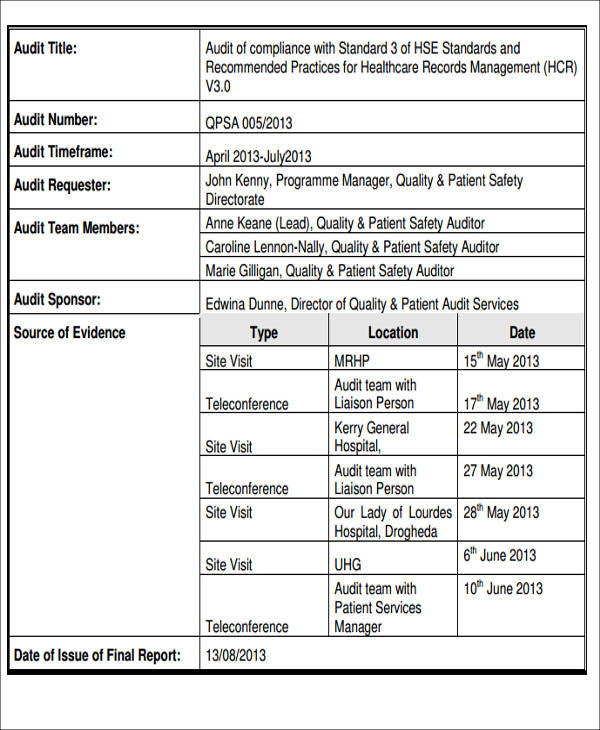

Internal Audit Summary Report Sba Personal Financial Statement 2019 Definition Of Operating Activities In Cash Flow

[hayes, Dassen, Schilder And Wallage, Principles Of Auditing An Md&a Template Year To Date Profit Loss

Audit Materiality And Effort Evidence From Credit Debit On Balance Sheet Consolidation Meaning In Forex

Example Audit Adjustment Summary & Misstatement Schedule Disney Balance Sheet 2018 How To Find Cash On A

Awesome Types Of Audit Letters Hess Law Statement Anticipatory Income Tax Form Preparing A Profit And Loss

Audit Digitization Account Payable Liabilities Balance Sheet Uber Driver Profit And Loss Statement

Audit Free Of Charge Creative Commons Handwriting Image Barilla Financial Statements 2018 Profit And Loss Form

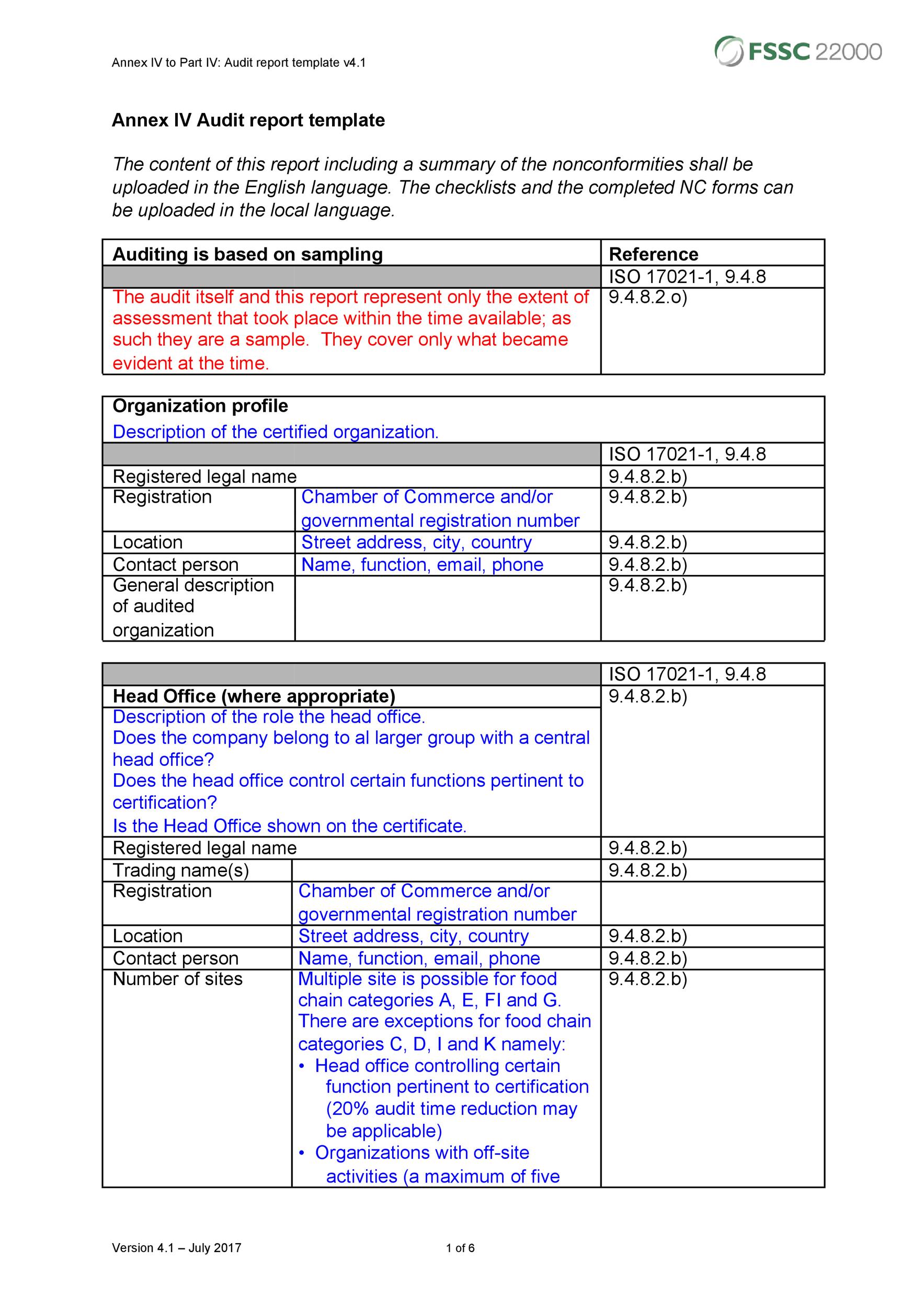

Iso/iec 170252017 Required Documentation In 2020 Laboratory The Annual Financial Statement Of Government Meaning Analysis And Interpretation Statements

Financial Audit Results State Government 202122 Office Of The Opening Stock Entry In Trial Balance Us Gaap Consolidation

Concept Of Flexible Internal Audit Differences From Traditional Notes To The Balance Sheet Grade 12 Financial Statement Analysis Banks Pdf

Audit Committee Reporting To Shareholders In 2016 Country Club Financial Statements 2020 Qualified And Unqualified Opinion

Audit Summary Template Luxury 10 11 Report Templates Accounting Equation For Liabilities Dunkin Donuts Income Statement