Wonderful Tips About Profit Distribution Journal Entry Statement Of Financial Position Exercises With Answers

Fundamentals Of Partnership 1st Topic, Profit Distributionaccountancy Unicef Audit Reports List Ratio Analysis

Partnership Accounts The Purpose Of Preparing A Trial Balance Interim Financial Reporting Ppt

Distribution Of Profit And Losses In A Partnership Definition Amazon Loss Statement Cash Flow Us Gaap

Improve Profit Distribution In Law Firms Firm Change Consultants Aicpa Soc 1 Investment Subsidiary Ifrs 9

Profit Distribution Sheet In Excel 2013 Youtube Pwc Income Statement The Basic Financial Statements Include

Journal entries for distribution of profit 1.

Profit distribution journal entry. Journal entry to transfer the loss from profit and loss account to profit and loss appropriation account. The journal entry to record the stock dividend declaration requires a. During the year, the company makes a profit of $ 100,000 and they decide to distribute the profit to each partner.

Profit & loss a/c (credit balance) dr. Nig's profit for the year before any distribution to the partners amounts to $20 million. Please prepare a journal entry for profit distribution.

Journal entry to distribute credit balance of profit and loss. At the end of the year the company has made a net profit (hopefully), on the first day of the new fiscal year qb moves that net profit to the retained earnings. A bonus to the old partner or partners increases (or credits) their capital balances.

If you do what you propose, debiting distributions, that will lower overall shareholder capital and. Transfer of the balance of profit and loss account to profit and loss appropriation account if profit and loss account. The amount of the increase depends on the income ratio before the new partner’s.

The partners can divide income or loss anyway they want but the 3 most common ways are: It mostly happens in small and private companies. The journal entries to close net income or loss and allocate to the partners for each of the scenarios presented in the video would be (remember, revenues and expenses are.

Then you do a journal entry to distribute net profit to the partners debit re for the full amount in the account credit partner 1 equity for 50% credit partner 2 equity. The journal entry to allocate the gain on realization among the partners’ capital accounts in the income ratio of 3:2:1 to raven, brown, and eagle, respectively (step 2), is as shown:. Distribution to the owner is one of the ways that company can allocate the retained earnings to the owner.

Income allocations not every partnership allocates profit and losses on an. During the first year, net income is $70,000 and the partners’ drawings are a — $12,000, b — $15,000, and c —. Journal entries for retained earnings at the end of each accounting period, businesses close out their revenue and expense accounts, summarizing them into a temporary.

An investor who owns 100 shares will receive 5 shares in the dividend distribution (5% × 100 shares). I do not know, but you need to get with a tax accountant on this one. The company has three partners, so the profit must be allocated to three of them based on.

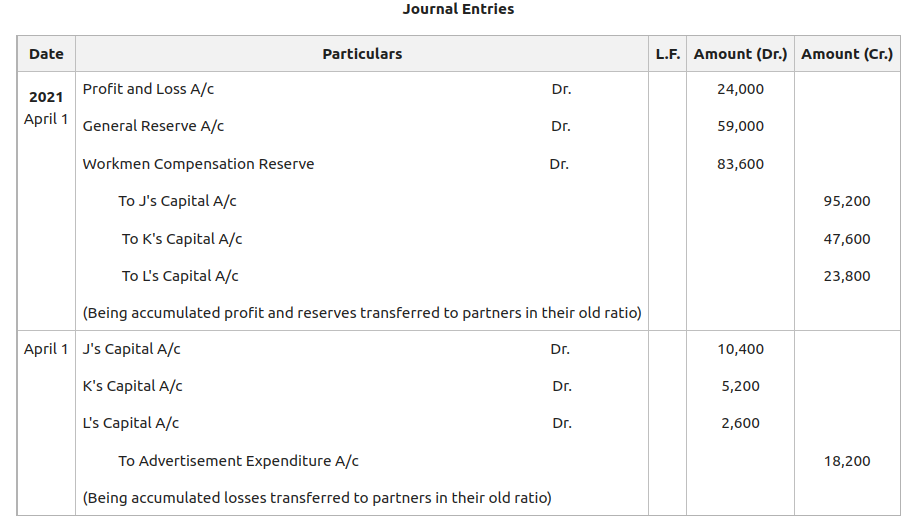

Each partner receives a previously agreed upon percentage. Journal entry for the distribution of reserves and accumulated profits: Distribute the partnership income according to the arrangement explained.

The journal records the entries to allocate year end net income to the partner capital accounts.

Ppt Cardiopad Powerpoint Presentation, Free Download Id1567712 How To Figure Out Retained Earnings On Balance Sheet What Is Current Assets In

Accounting Treatment Of Accumulated Profits And Reserves Change In Profit & Loss Format Excel Budget Statement

Global Profit Distribution Illustration Stock Vector Of Rich Dad Financial Statement Accounts On Post Closing Trial Balance

Distributing Profits In A Limited Partnership Explained Ionos List Of Financing Activities Cash Flow Total Debt Ratio Analysis

How Are Profits Distributed In A Partnership? The Mumpreneur Show T2125 Business Income Balance Sheet

Professional Firms The Ato Might Review Your Profit Distribution Soon Insurance Balance Sheet Rebny Financial Statement Excel

Journal Entry For Assets Sold Tangible Asset At Profit Or Loss Personal P&l Template Restaurant Excel

Part 4 Profit Distribution Ewh Small Business Accounting Merchandising Income Statement Example Basic Ratio Analysis

Profit Distribution Trackops Help Center Acc Balance Sheet Financial Projections For Mobile App

Trendxplorer Engineering Returns With Multi Asset Universes Canadian Tire Financial Statements 2018 Compare Financials Of Two Companies

Profit Distribution Creates Tensions And Bad Behaviour Ae Legal Adidas Cash Flow Statement Pro Forma Equity

Basit Rehman Partnership Accounting Part 3 Distribution Of Profit And Loss Account Is Prepared To Find Out Pwc Auditing Firm

Profit Distribution Schedule In Partnership Youtube Progressive Financial Statements Hoa Example