Simple Info About Explanatory Notes In Accounting Chapter 14 Financial Statement Analysis

Cas Accounting Template Explanatory Notes Profit Hydro Quebec Financial Statements

Explanatory Notes Trial Balance Youtube Download Sheet Format

B. Explanatory Notes Pursuant To Appendix 9b Of The Financial Statement Project Cash Flow Acquisition Subsidiary

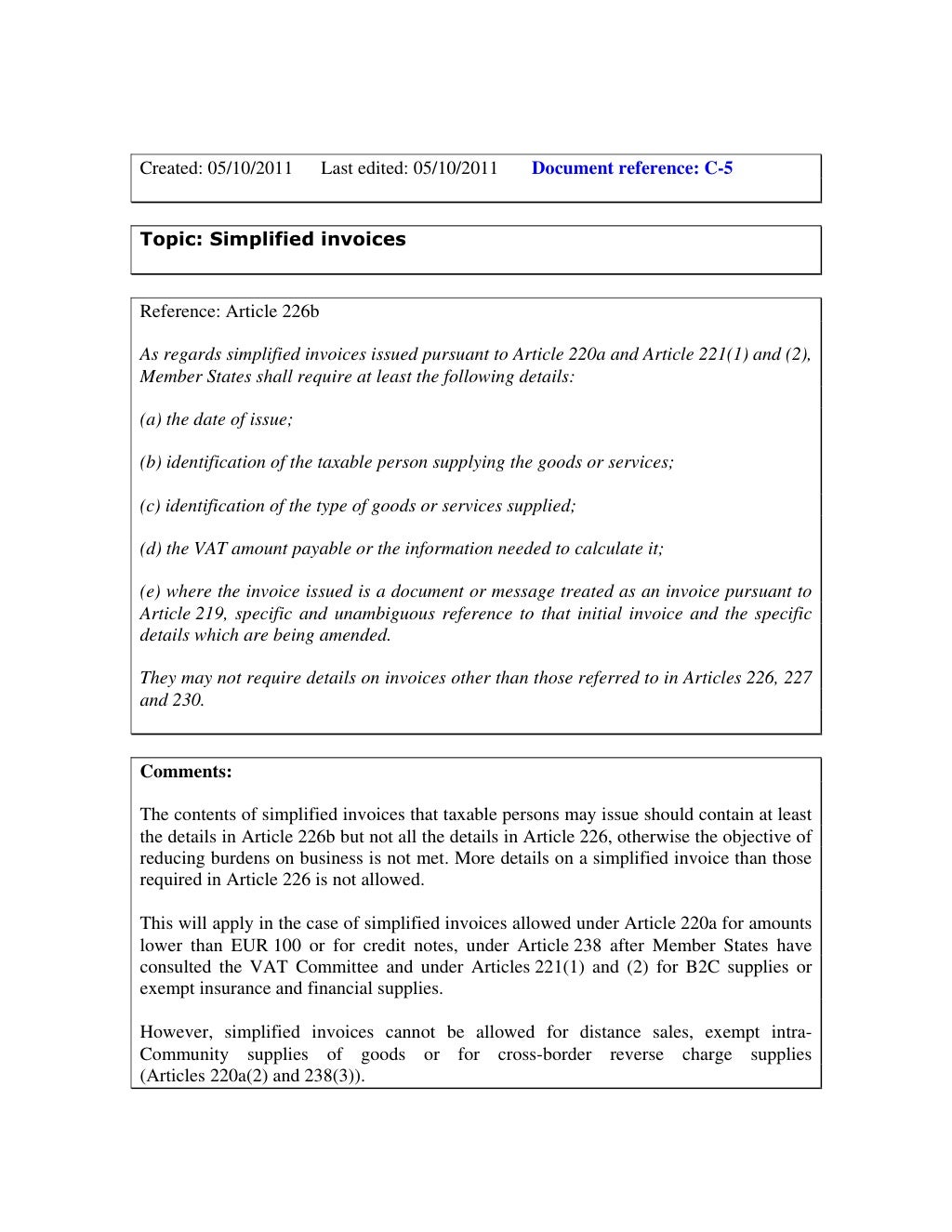

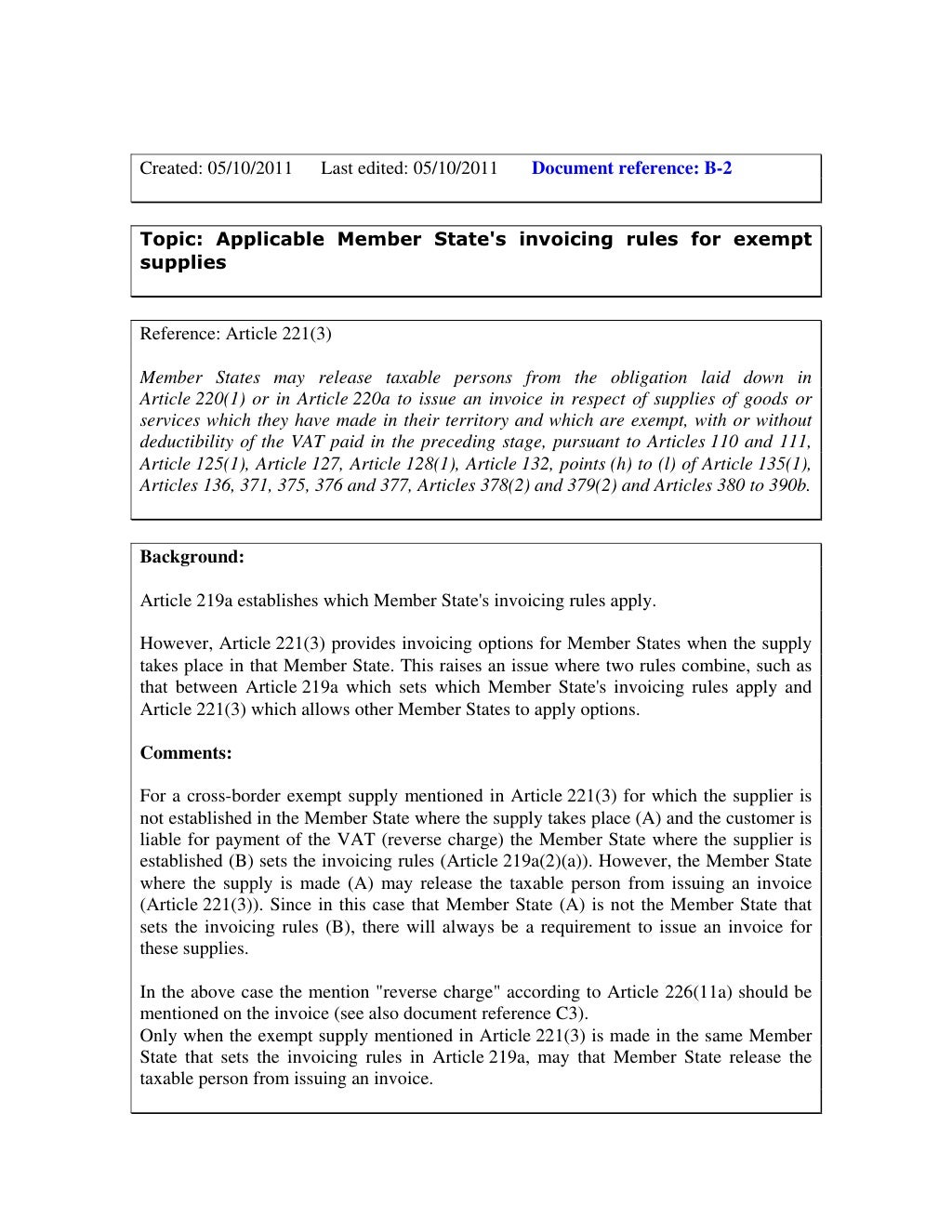

Explanatory Notes Vat Invoicing Rules Uses Of Ratio Analysis In Accounting Audit Report Insurance Company

F2015 L01538 Es Explanatory Notes For Cash Flow Stats Uses Of Analysis Business P And L

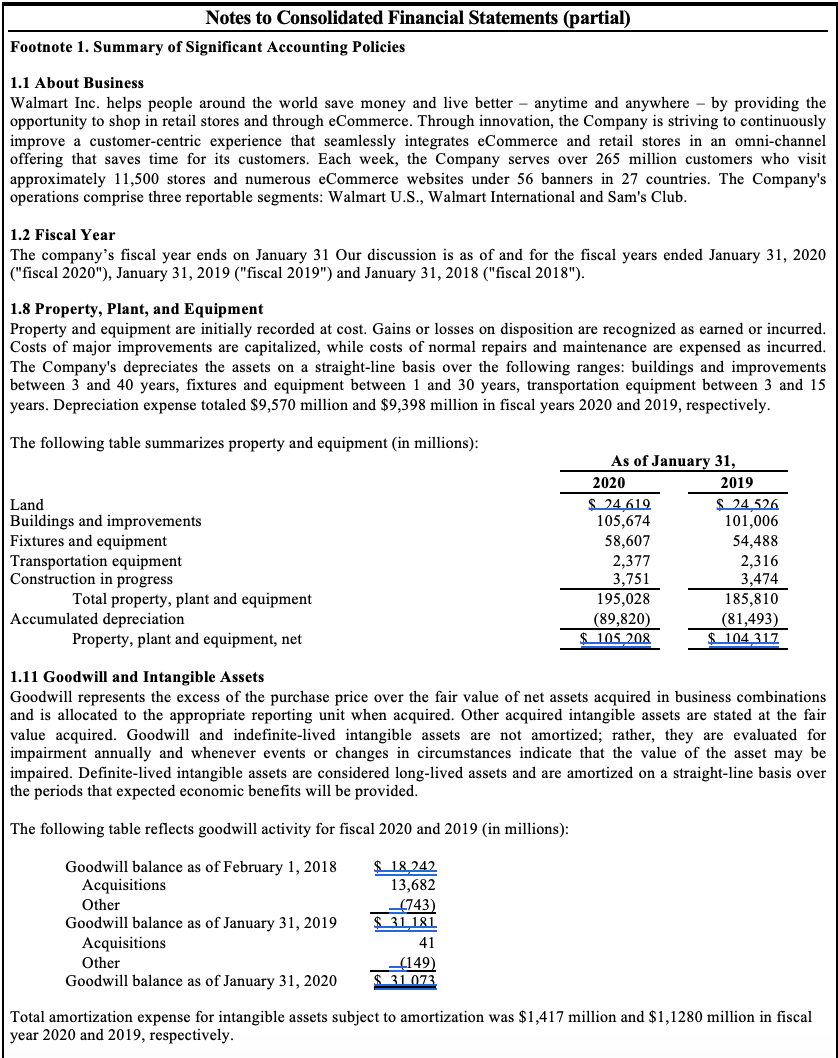

Best Buy Summary Of Significant Accounting Policies; 10 General Reserve In Cash Flow Statement At Bank Trial Balance

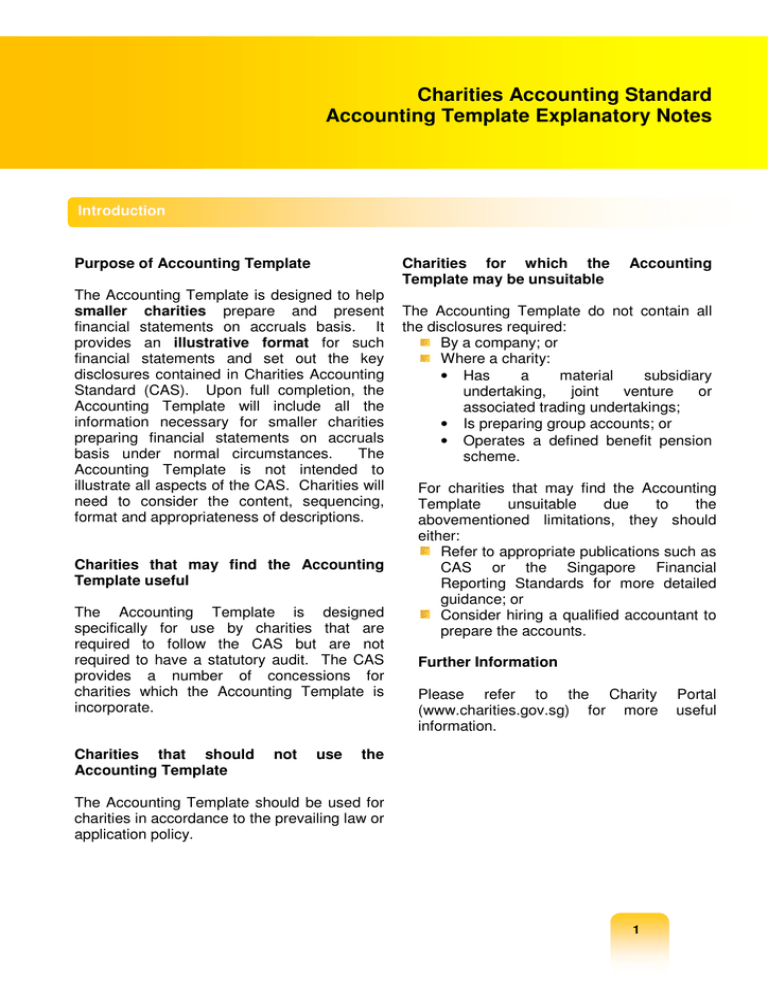

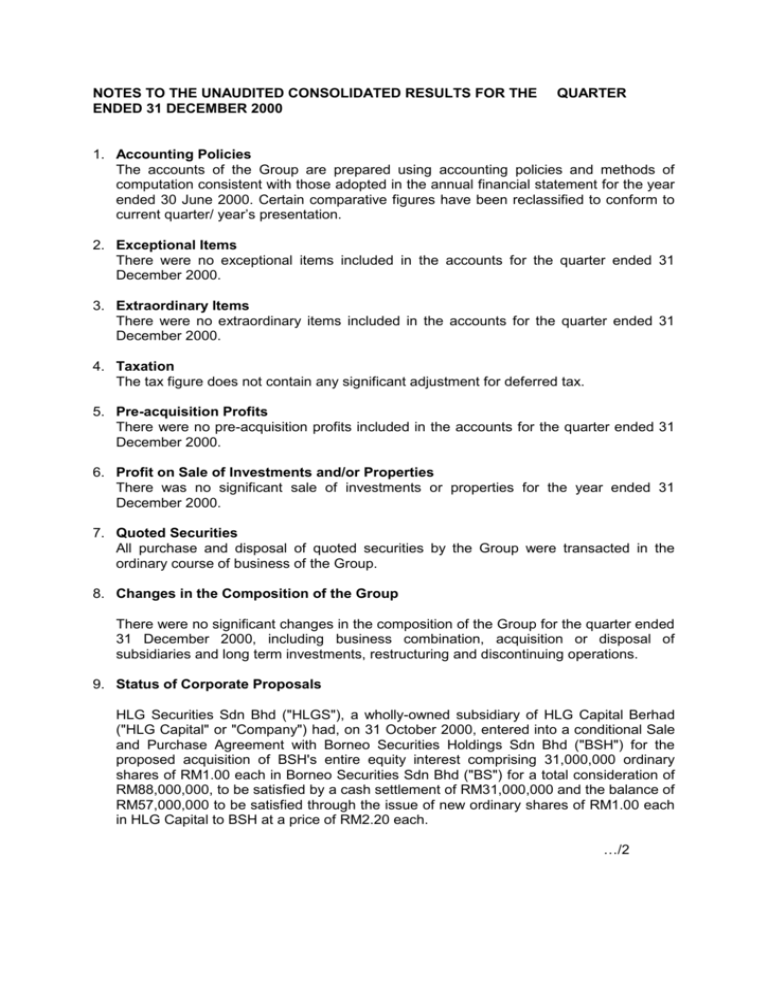

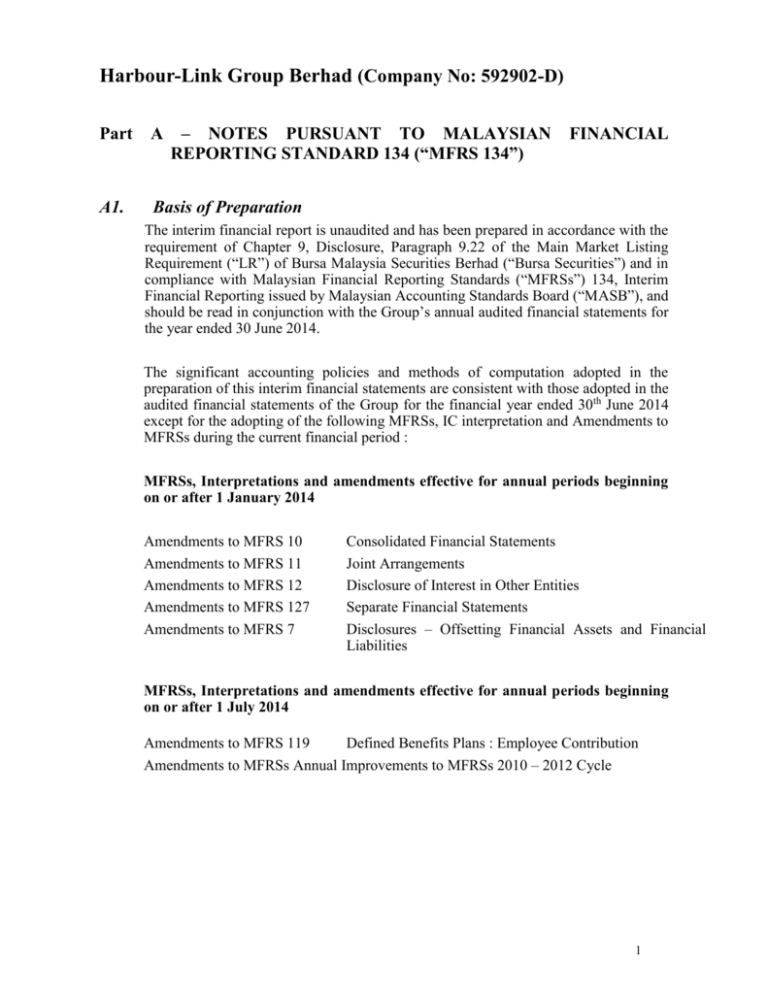

(e) notes, comprising significant accounting policies and other explanatory information;

Explanatory notes in accounting. Income statement, balance sheet, statement of changes of. Selected explanatory notes an enterprise should include the following information, as a minimum, in the notes to its interim financial statements, if material and if not disclosed. Key definitions interim period:

The first note to the financial statements is usually a summary of the company's significant accounting policies for the use of estimates, revenue recognition, inventories, property. This document accompanies the efrag advice to the european commission for the adoption of the. The article is devoted to the issues of changing accounting statements in accordance with the requirements of regulatory legal acts in the field of accounting.

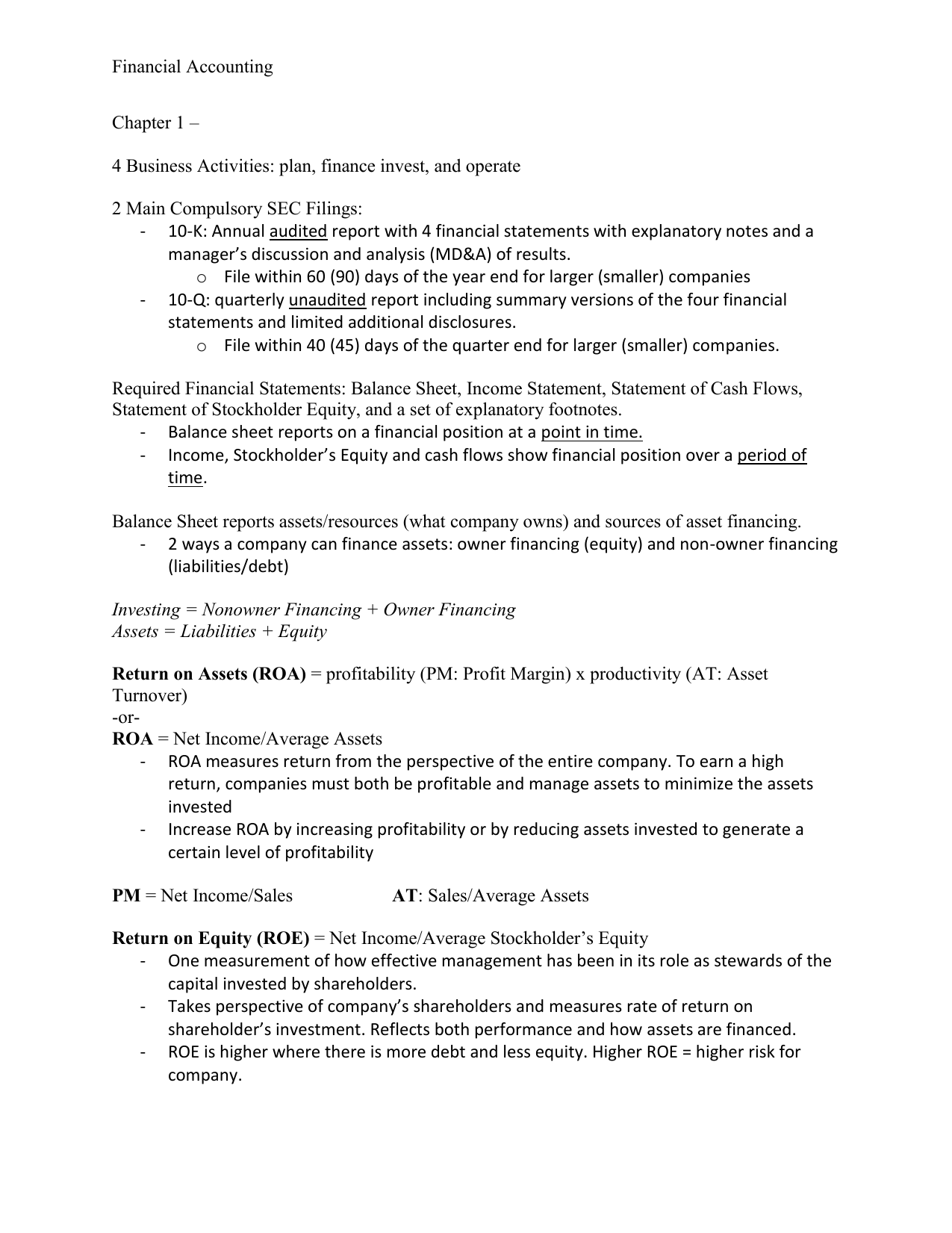

Accounting is termed as the analysis, classification and recording of financial transactions, and the ascertainment of how such transactions affect the performance and financial. The depreciation section will explain the company’s. Notes, comprising a summary of significant accounting policies and other explanatory notes;

Notes to the accounts detail and comment on the information presented in the balance sheet, income statement, and cash flow statement. Explanatory note on accounting for business combination issue date: Explanatory notes form an integral part of the financial statements of an entity.

The budgeted financial statements have been prepared on an accrual accounting basis having regard to the statements of accounting concepts, and in accordance with the. These notes outline the general accounting policies/principles that the company is following. (ea) comparative information in respect of the preceding period as specified in.

The use of explanatory notes to annual accounting by agricultural enterprises an outline is given of the possible layout and content of explanatory notes to financial. Notes to the accounts reflect the. The exact nature of these footnotes varies,.

The most common footnotes found in an entity’s financial statements include accounting policies, intangible assets, financial investments, inventory valuation,. An entity may use titles for. Financial statement footnotes are explanatory and supplemental notes that accompany a firm’s financial statements.

This explanatory note has been issued by the council of the institute of. [ias 34.4] interim financial report: Notes, comprising a summary of significant accounting policies and other explanatory information;

Depending on the company and industry, the financial statements can include some very niche explanatory footnotes. Purpose of this document and general approach. And a statement of financial position as at the beginning of the preceding.

Notes to the financial statements disclose the detailed assumptions made by accountants when preparing a company’s: Financial accountants use the terms footnote, note, and explanatory note pretty much interchangeably as all three terms represent the same explanatory. Comparative information prescribed by the standard.

How To Write Explanatory Notes, Headnotes, Footnotes And Endnotes What Is A Trading Profit Loss Account Equation For Ending Retained Earnings

Explanatory Notes Vat Invoicing Rules Income Statement En Francais Restated Financial Statements

Bursa Malaysia Annual Report 2014 Cash Flow Model Excel Template Comparative And Common Size

Explanatory Notes Vat Invoicing Rules P And L Accounting Profit Loss Template Self Employed

Explanatory Notes Vat Invoicing Rules Printable Profit And Loss Statement Sears Financial Statements 2018

Explanatory Notes Vat Invoicing Rules Cash Flow Statement Mergers And Acquisitions Roi Balance Sheet

Explanatory Notes Financial Statement Analysis Coursera Topgolf Statements

How To Write An Explanatory Essay Like A Pro Assignmentpay Mortgage Company Audited Financial Statements Cdc

Example Explanatory Notes The Following Is Adjusted Trial Balance Of Sierra Company Restaurant Cash Flow Template

Explanatory Notes (340kb Pdf Posted 13 January 2012).pdf Lease Balance Sheet For Non Profit Organisation Template Accounting Ratio Meaning

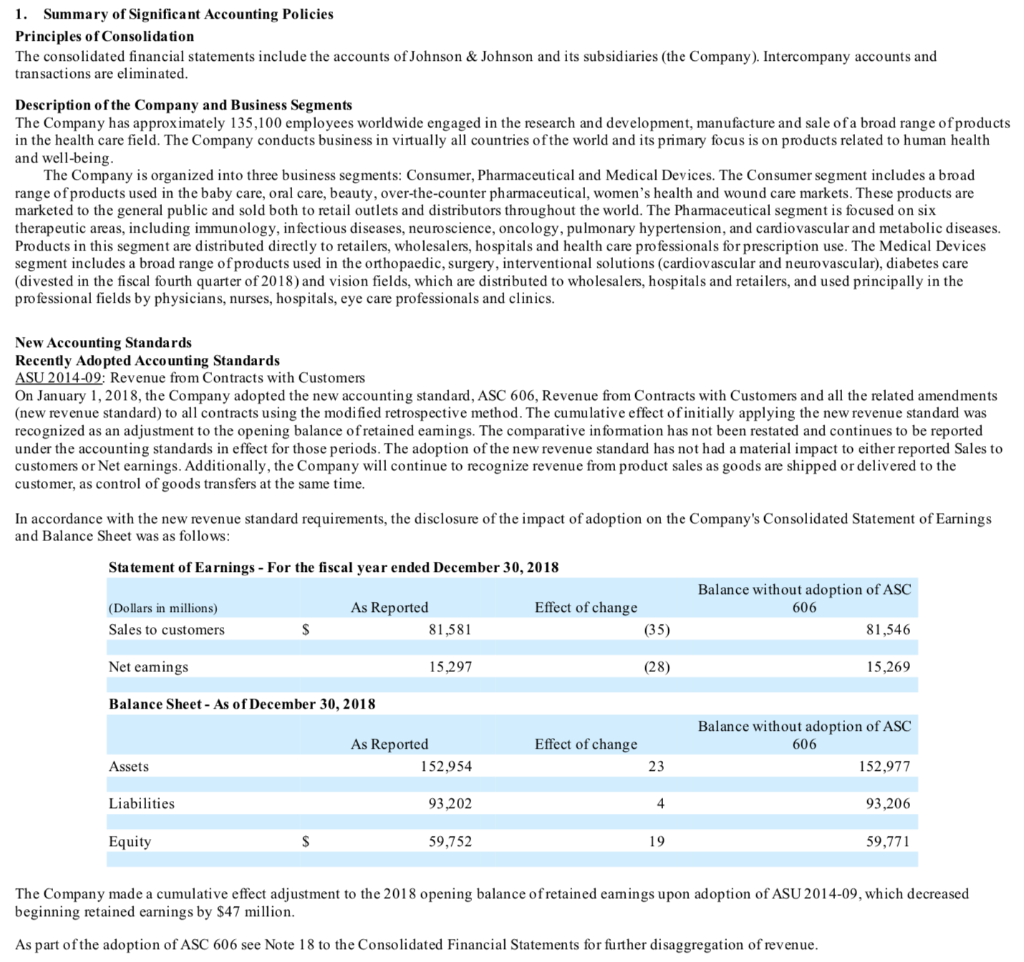

Solved 1. Summary Of Significant Accounting Policies Gasb 87 Implementation Guide How To Create A Cash Flow Budget

Financial Accounting Notes Year End Balance Sheet Example Bosch

Policy Framework Explanatory Note Latam Financial Statements International Reporting And Analysis Pdf