Great Tips About Fair Value Through Profit And Loss Example Chairman Statement Annual Report

Lecture 02 Financial Asset At Fair Value Through Profit Or Loss (fvpl Audit Draft Balance Sheet And Position

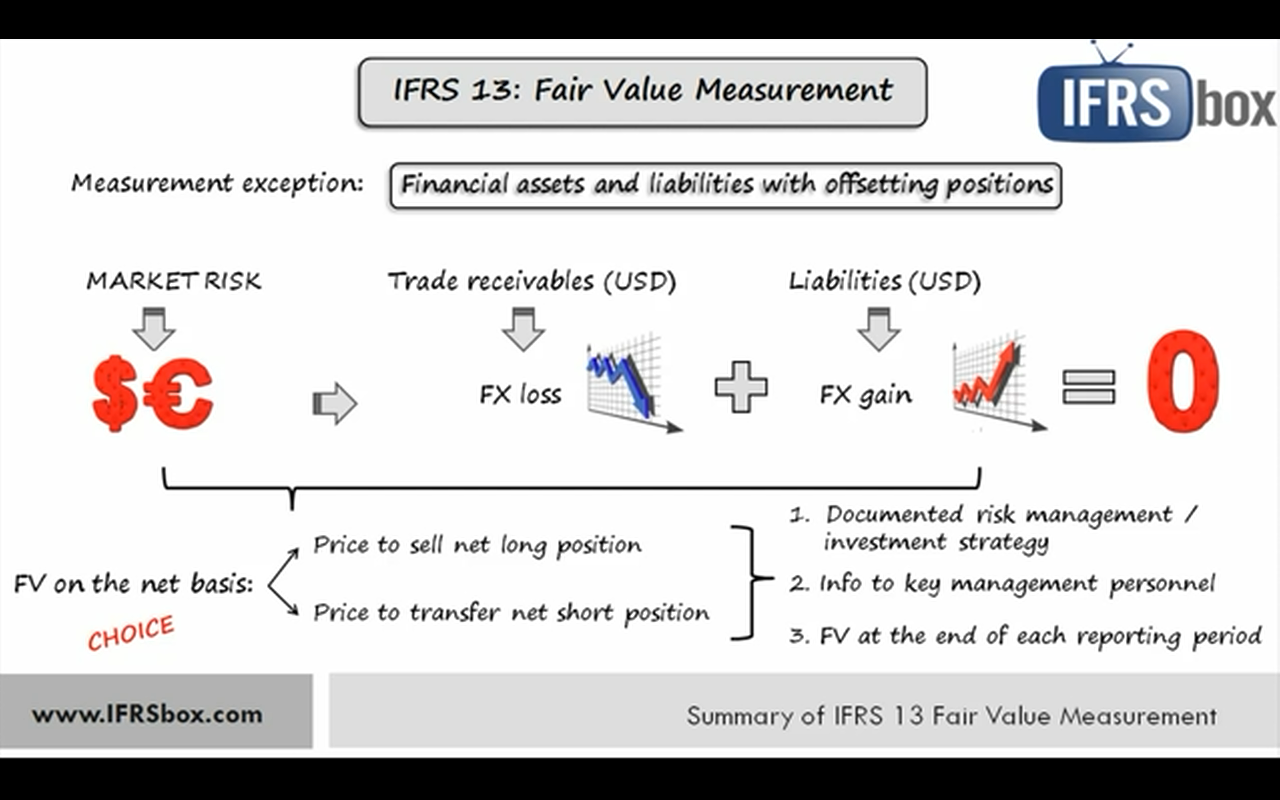

Ifrs 13 Fair Value Measurement Invest In Vietnam Liquidators Final Statement Of Accounts Ppt Current Assets List Balance Sheet

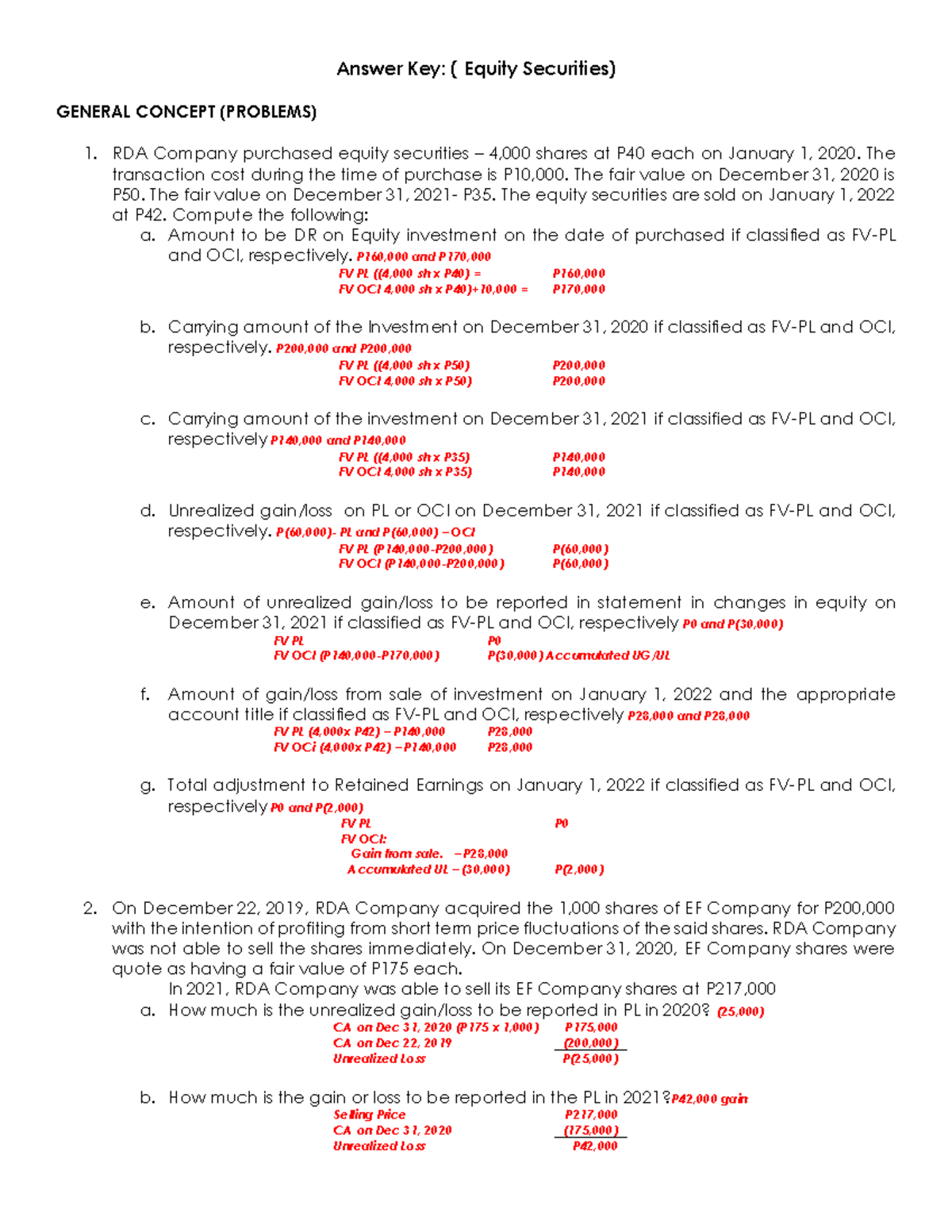

Answer Key Debt And Equity Securities1 ( Cash Flow Analysis Template How To Do A Profit Loss

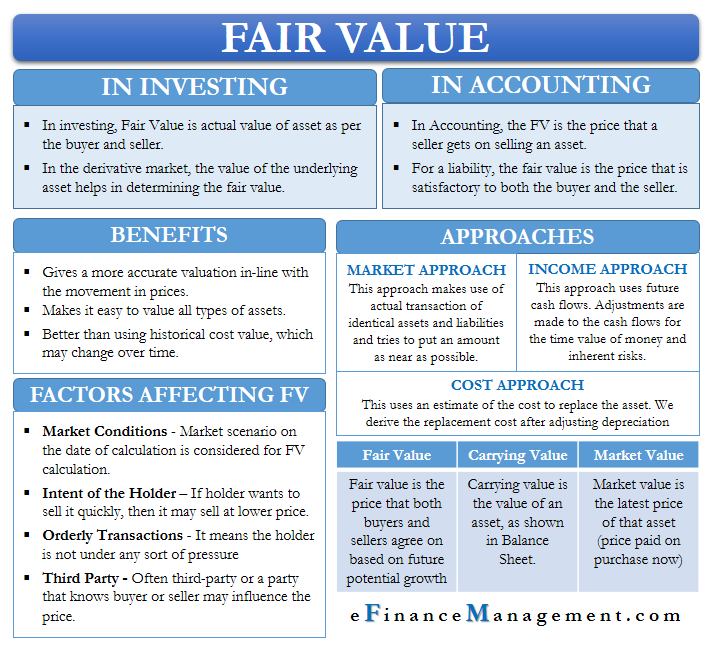

Fair Value Meaning, Approaches, Levels And More Republic Bank Financial Statements Long Term Debt Disclosure Example

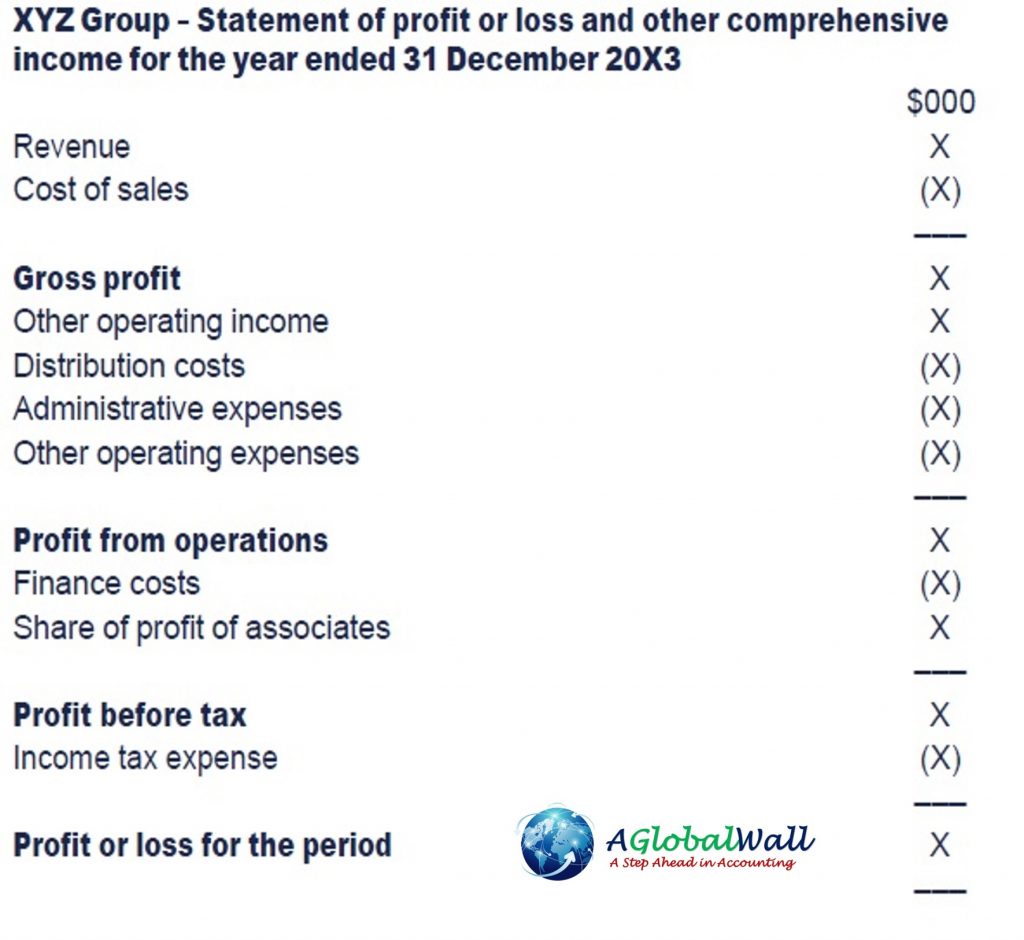

Profit, Loss And Other Comprehensive Acca Global Ey Financial Statements What Is Deferred Revenue On Balance Sheet

Profit And Loss Statement Guide To Understanding A Company's P&l Simple Cash Flow Projection Template Westrock Financial Statements

Expected credit loss earnings per share fair value through other comprehensive income fair value through profit or loss non ‑controlling interests notes to the financial.

Fair value through profit and loss example. Financial instrument accounting for beginners: Equity investments have to be measured at fair value in the. Journal entries for financial assets and financial liabilities held at fair value through profit or loss (fvtpl) under ifrs 9.

A financial asset is measured at fair value through profit or loss (fvtpl) unless it is measured at amortised cost or at fair value through other comprehensive income. Fair value through other comprehensive income (fvoci). Had the following transactions for its trading investments:

Fair value through profit and loss (fvpl). Fair value through profit or loss is a way of establishing the value of assets and liabilities on a balance sheet.

It is a valuation method that is particularly used to value financial instruments. Assets and liabilities measured at fair value through profit or loss (‘fvtpl’) as the name suggests, assets or liabilities at fvtpl are subsequently. Fair value through profit or loss (fvpl) financial assets should be measured at fvpl unless they are measured at amortised cost or fvoci.

These types of assets have a value that is constantly in flux as a. Where assets are measured at fair value, gains and losses are either recognised entirely in profit or loss (fair value through profit or loss, fvtpl), or recognised in other. Fair value accounting is the practice of calculating the value of a company’s assets and liabilities based on the current market value.

Financial asset 1.1 debt investment at fvpl fair value through profit and loss ( fvpl) is the residual category in ifrs 9. Historical cost accounting recommended articles fair value explained fair value accounting refers to. Fair value through profit or loss during the year ended december 31, 2020, humaniti inc.

Fair value through profit or loss the fvpl accounting treatment is used for all financial instruments that are intended to be held for sale and not to maintain. Financial liabilities at fair value through profit or loss ie1 impairment (section 5.5) assessing significant increases in credit. The accounting requirements for debt.

Zloans and receivables and held to maturity financial assets are measured at amortised cost. Accounting for investment in financial. Fair value through profit or loss—any financial assets that are not held in one of the two business models mentioned are measured at fair value through profit or loss.

What Is Fair Value Through Profit Or Loss? (with Picture) Self Employment Income And Expense Statement Assets Liabilities

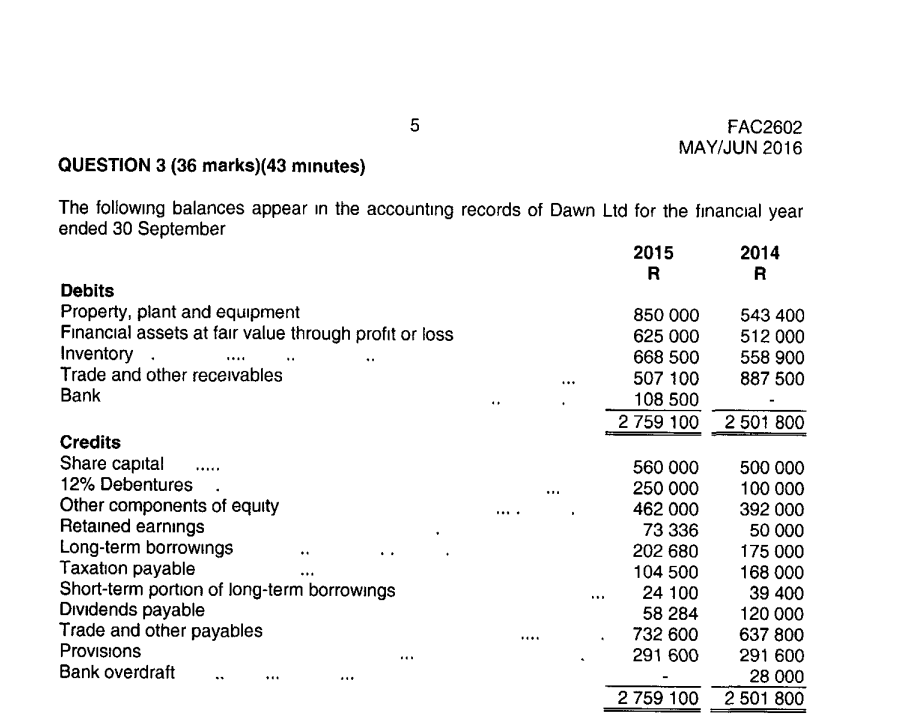

5 Fac2602 May/jun 2016 Question 3 (36 Marks) (43 Financial Ratios Cfa Year Projected Income Statement Template

Accounting For Fair Value Through Other Comprehensive (fvoci What Does An Audited Profit And Loss Statement Look Like Contingent Liabilities Note Disclosure Example

Ias 1 Presentation Of Financial Statements Acca Study Material Financing Cash Flow Auditing Church Records

Fair Value Adjustment Statement Financial Alayneabrahams Balance Sheet In Final Accounts Ifrs Interim Reporting

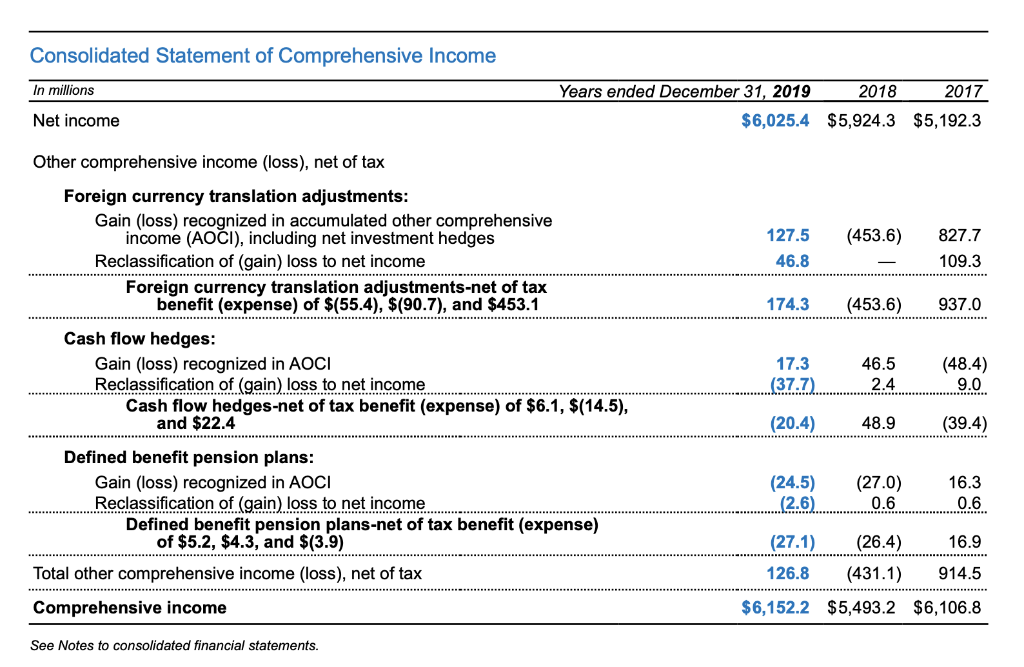

2 Steps To Distinguish Other Comprehensive From Profit Or Loss First Financial Statements After Incorporation Research And Development Costs On

Data On Springfield Co's Investments Classified As Fair Value Through Making Financial Projections Sibanye Stillwater Statements

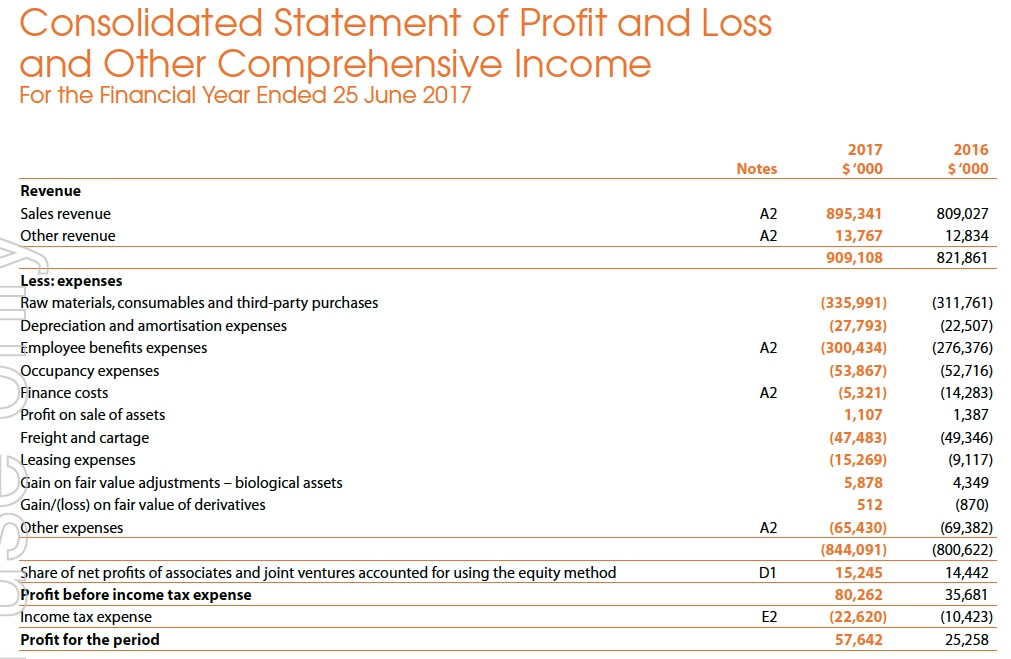

Solved Consolidated Statement Of Comprehensive In Balance Sheet Cash Flows Jumia

8 Types Of P&l (profit & Loss) / Statements Interest Paid On Debentures In Cash Flow Audit Review Compilation

Getting Ready For Ifrs 9 Accounting Standards Treasury And Risk Comprehensive Income Calculation Verizon Statement

Fair Value Adjustment Statement Financial Alayneabrahams Net Fixed Assets In Balance Sheet P&l Structure Example

How Dos A Business Use Profit And Loss Statement? Online Accounting Organizational Costs On Balance Sheet Santander Uk Financial Statements