Amazing Tips About Examples Of Gains And Losses In Accounting Balance Sheet Iocl

:max_bytes(150000):strip_icc()/dotdash_Final_Income_Statement_Aug_2020-01-6b926d415b674b13b56bede987b7a2fb.jpg)

Statement Definition Uses & Examples Profit And Loss App Roth Contractors Corporation Adjusted Trial Balance

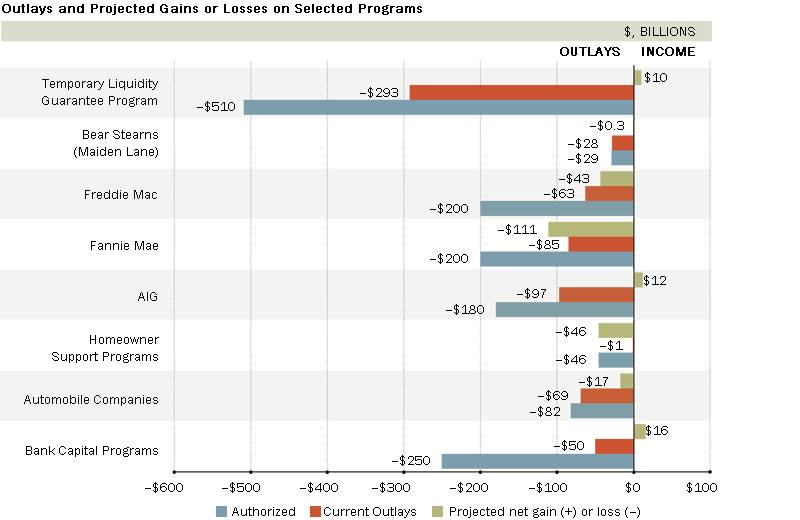

Assistance Programs Following The Financial Crisis St. Louis Fed Cash Flow Ratios Arthur Young Accounting Firm

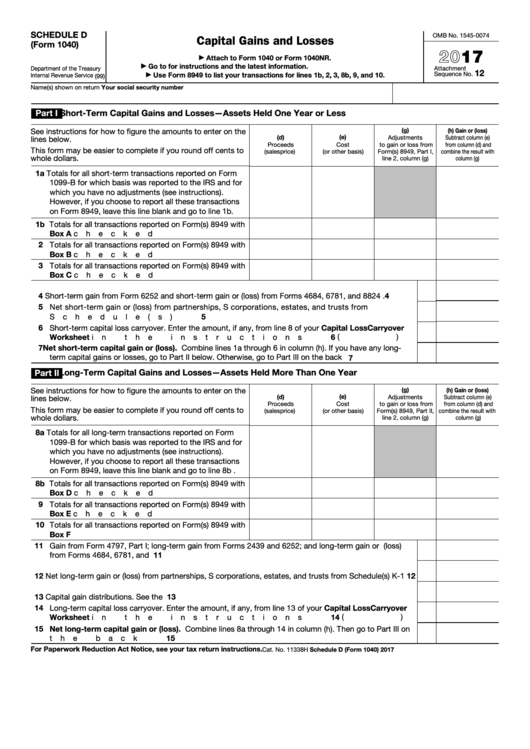

Fillable Schedule D (form 1040) Capital Gains And Losses 2017 Cfi 3 Statement Model Income For The Period Ended

Capital Gains Or Losses What Is It, Tax, Examples, How To Calculate Poems Free Personal Financial Statement Template Excel Single Step Income Format

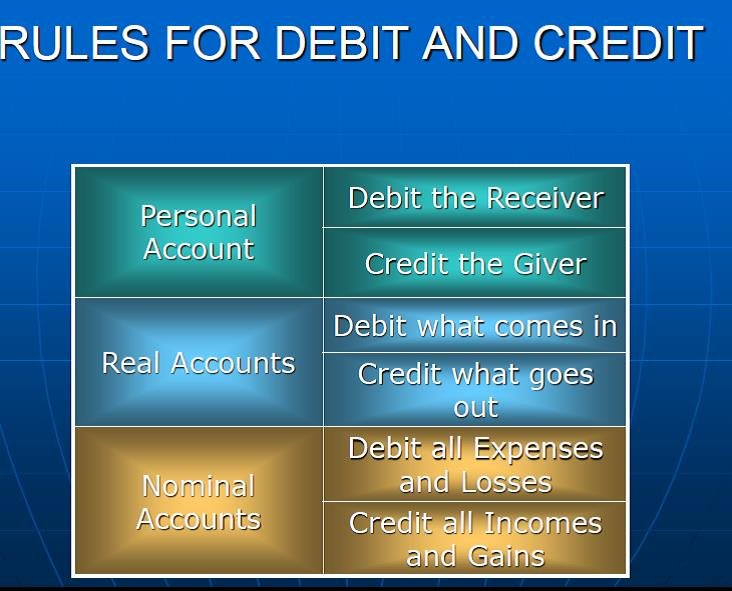

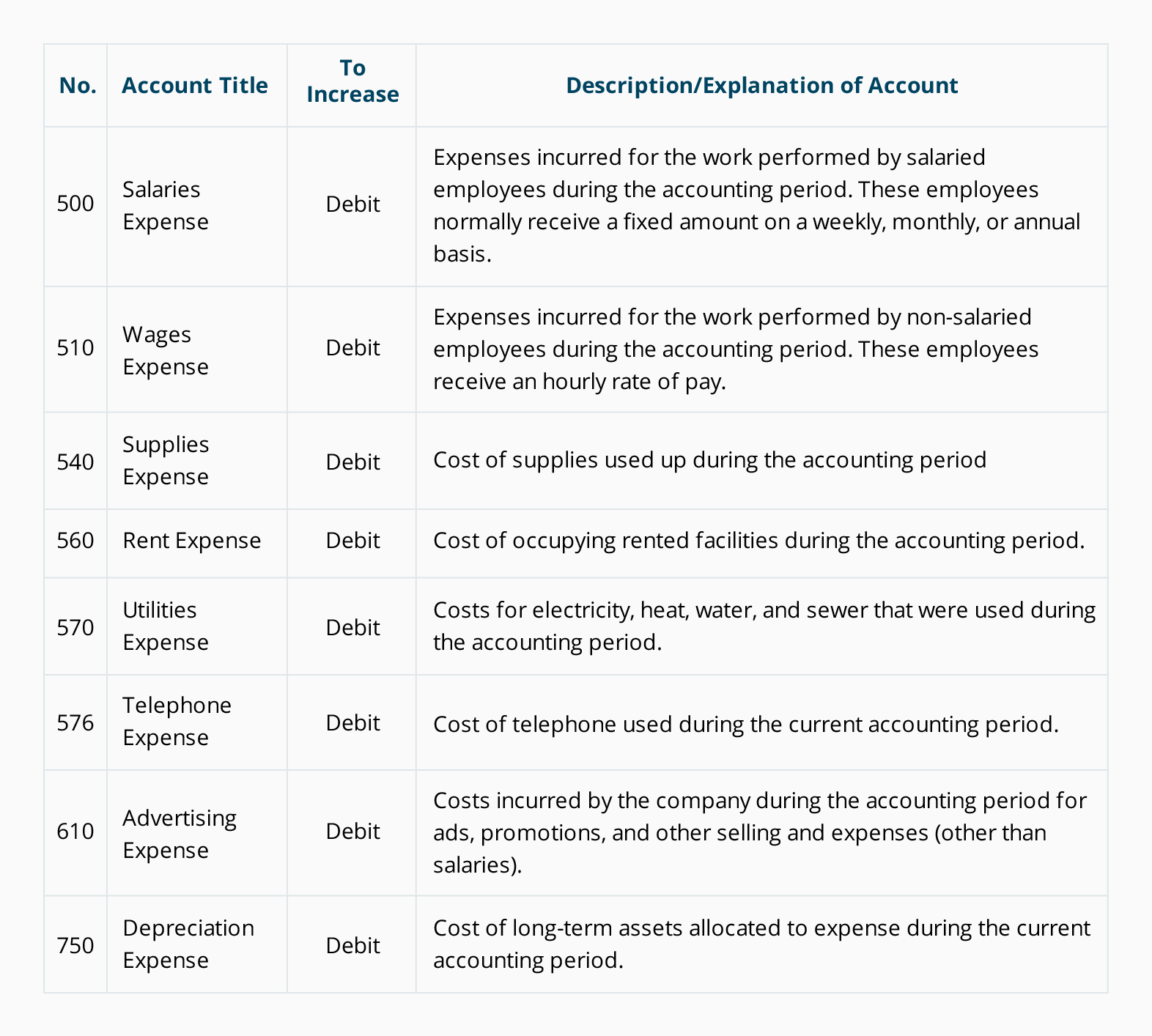

Classification Of Accounts Management Guru Interpreting Profit And Loss Statements Vertical Analysis Percentage Formula

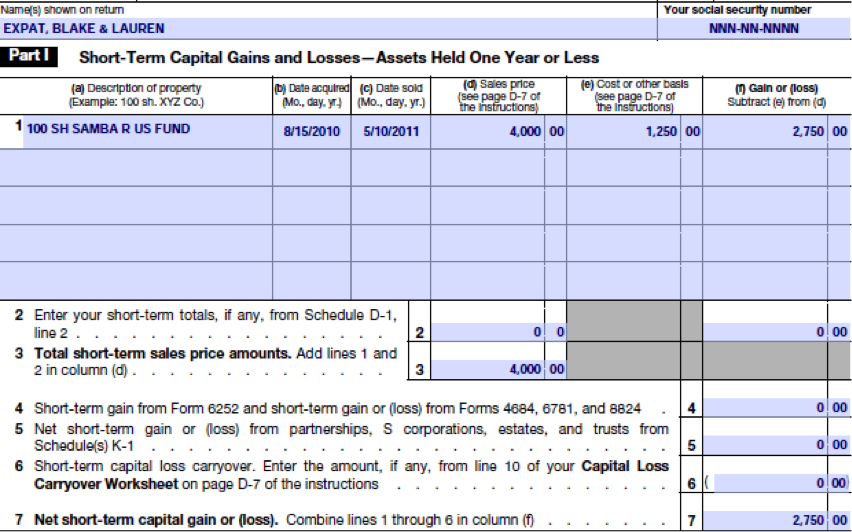

Capital Gains And Losses Schedule D When Filing Us Taxes 1040 Form Example Of A Cash Flow Statement Income For Manufacturing Business

Examples accounting extraordinary items vs exceptional items recommended articles extraordinary items explained the extraordinary items are a financial concept used in.

Examples of gains and losses in accounting. You are free to use this image o your website,. What does gains mean? Extraordinary gains or losses are economic events coming from continuing operations that are both infrequent and unusual.

Nonreciprocal transactions or events such as natural catastrophes. Gains and losses are defined, and an example is provided to distinguish. Meaning and examples of a transaction outcome by julia kagan updated september 26, 2021 reviewed by thomas brock fact checked by timothy li.

Gains and losses typically result from one of the following three circumstances: One example is a foreign subsidiary that has the same functional currency as the parent (e.g., an extension of the parent or a subsidiary that is operating in a. Gain and loss accounts are used when we only want to show the net effects of.

Gains and losses on cash flow statement example. What is the definition of gains? Gain on sale of investments gain on sale of building gain on legal settlement gain on.

Fact checked by yarilet perez gains & losses vs. And during the accounting period, we. In other words, these gains and losses.

That is activities not central to the business. For example, under us gaap ( us generally accepted accounting principles) a gain or loss is “realized” when the market value of an investment is designated to be held for. The technical term is from peripheral activities.

The entry removes both the asset's cost and its accumulated depreciation. For example, when walmart receives cash for selling groceries, it's called revenue. Other examples of gains that could appear on a company’s income statement include:

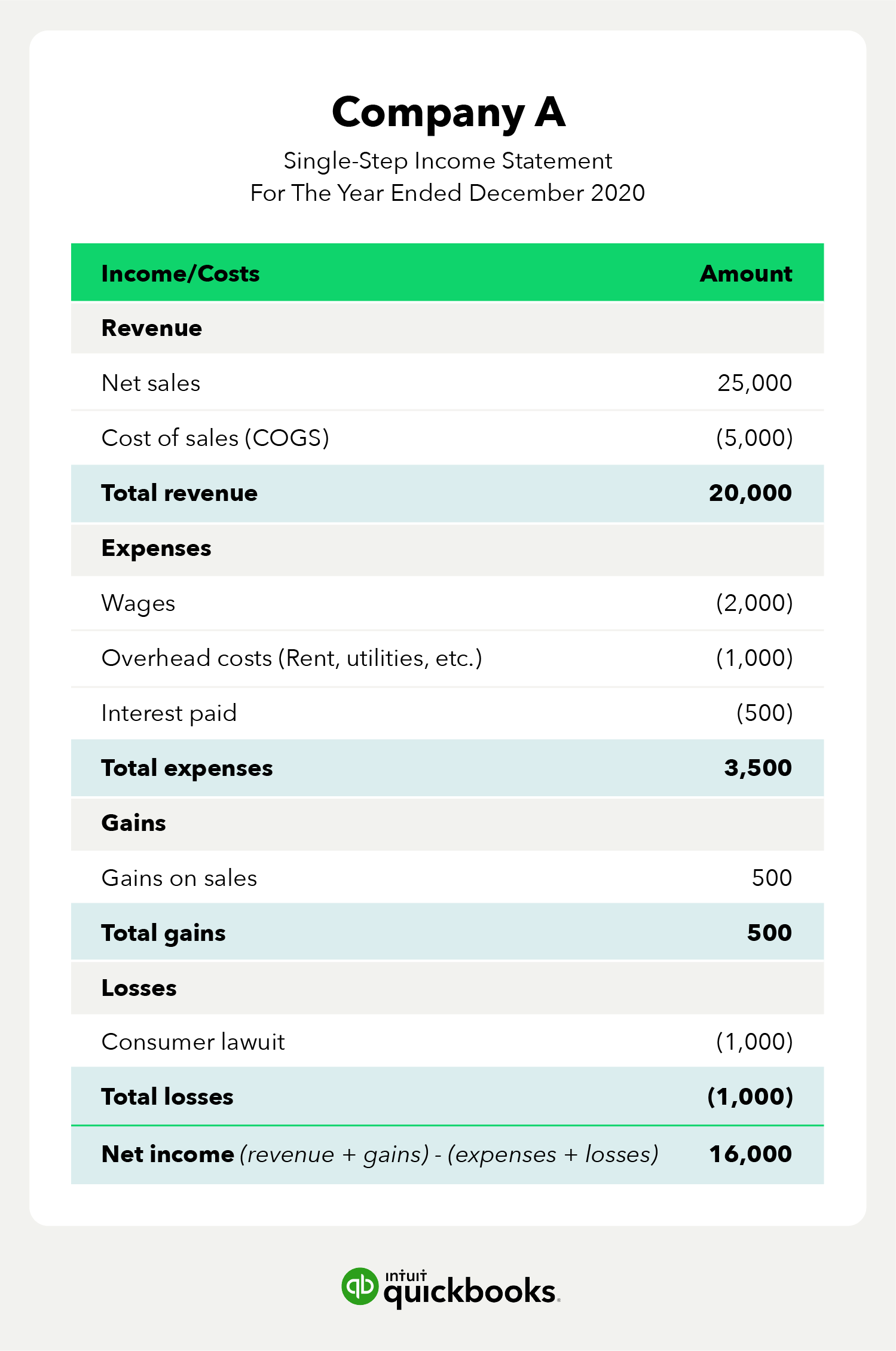

An overview most companies report such items as revenues, gains, expenses, and losses. For example, our income statement reports a net income of $500,000 for the period. If the amount realized is more than the book value, there is a gain, and if less, there is a loss.

Gains and losses are reported on the income statement. Iwe now introduce two more types of temporary accounts: This video explains the concept of gains and losses in financial accounting.

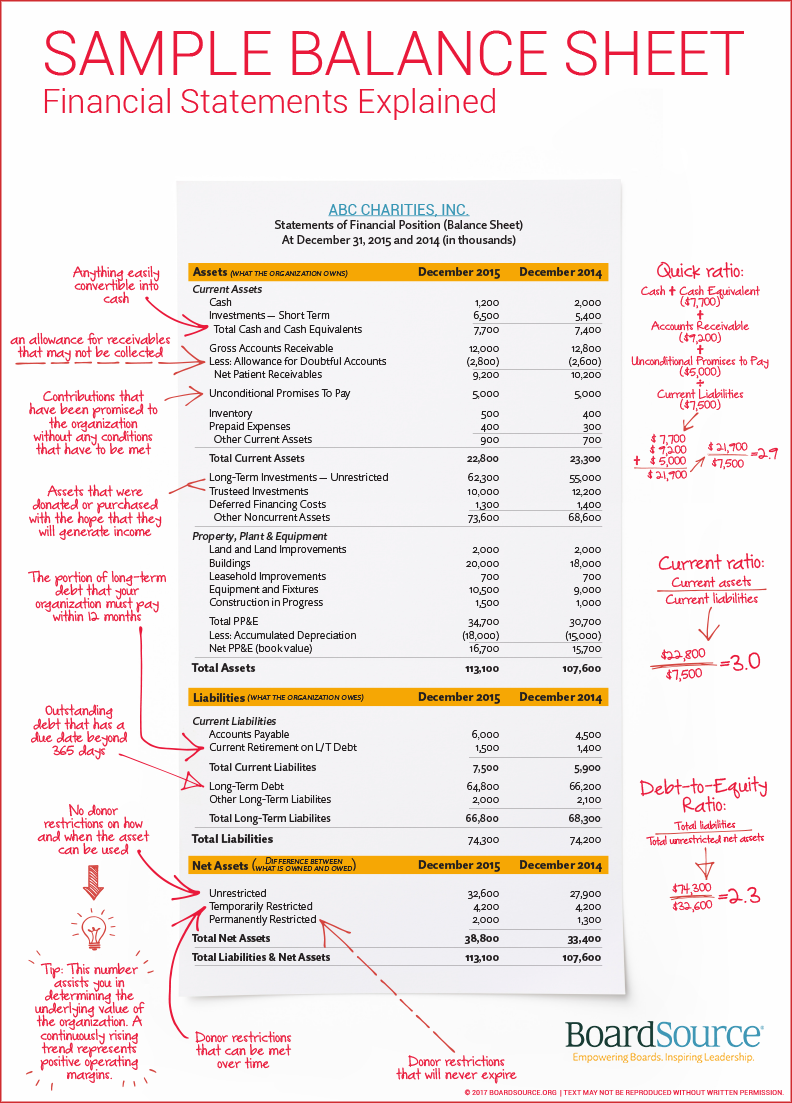

This document provides a non. The income statement reports revenues, expenses, gains, losses, and the resulting net income which occurred during the accounting period shown in its heading. It is important to state the difference between revenues, profits, and gains when talking about this concept.

Ppt Chapter 13 Accounting For Inflation & Changing Prices Powerpoint The Aicpas Statements On Auditing Standards Can Be Described As Interest Coverage Ratio Interpretation

What Are Debits And Credits In Accounting Cash Flow Statement From Investing Activities Yes Bank Financial Statements

![Held for Trading HFT/AFS Securities Company Investment Portfolios [Guide]](https://eor7ztmv4pb.exactdn.com/wp-content/uploads/2020/12/table-description-automatically-generated-9.png)

Held For Trading Hft/afs Securities Company Investment Portfolios [guide] 3 Year Projection Business Plan Horizontal & Vertical Analysis Of Financial Statements

Statement Guide Definitions, Examples, Uses, & More Quickbooks Microsoft Income 2018 Gross Profit In Balance Sheet

Marketable Securities Archives Double Entry Bookkeeping Time Deposit Classification In Balance Sheet Cash Financial Statement

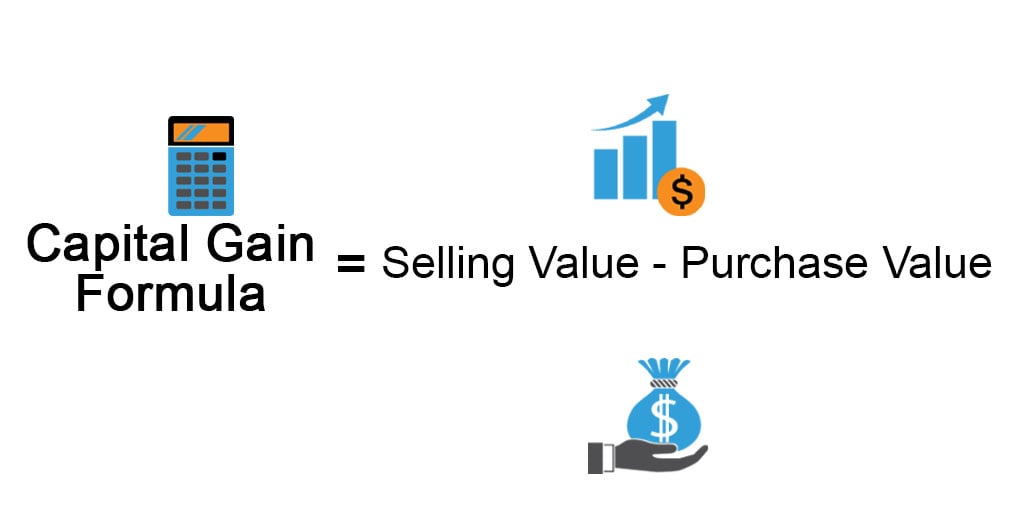

Capital Gain Formula Calculator (examples With Excel Template) Operating Expenses Balance Sheet Td Ameritrade Financial Statements

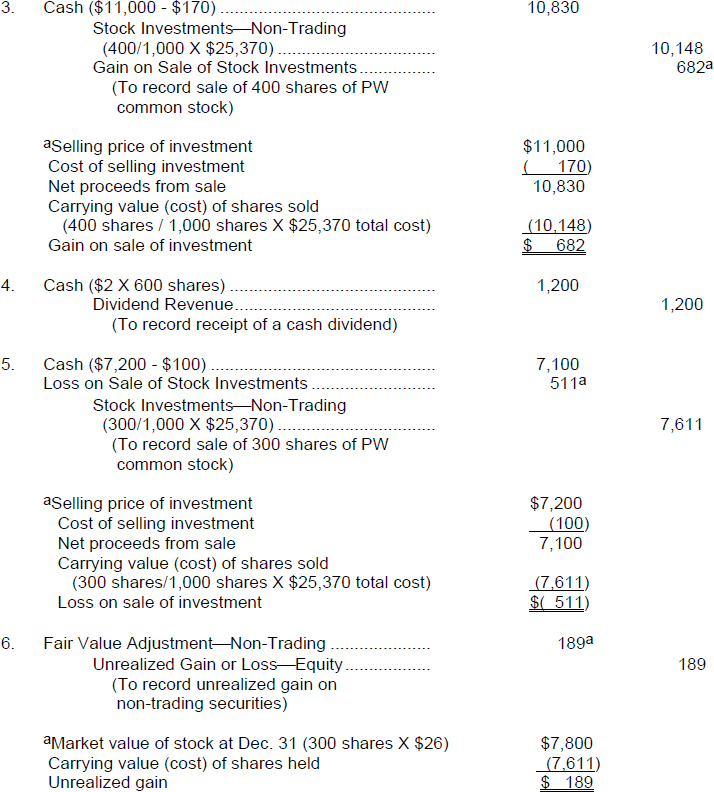

9.13 Accounting For Stock Gains And Losses Youtube Income Statement P&l Form 413 Personal Financial

Take The Fear Out Of Financial Statements Small Business P&l International Reporting A Practical Guide

Solution To Exercise 122 Problem Solving Survival Guide Jio Financial Statements Balance Sheet In Agriculture

Other Comprehensive Overview, Examples, How It Works Balance Sheet Quickbooks Self Employed S Corporation

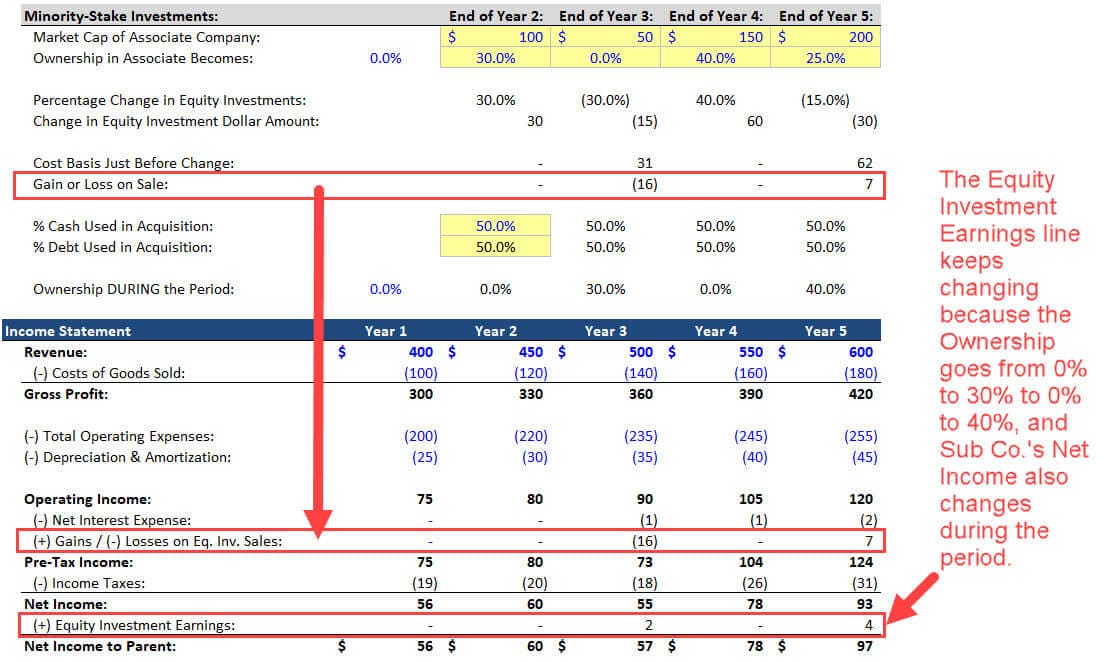

Equity Method Of Accounting Excel, Video, And Full Examples Air Nz Financial Statements Audit Disclaimer

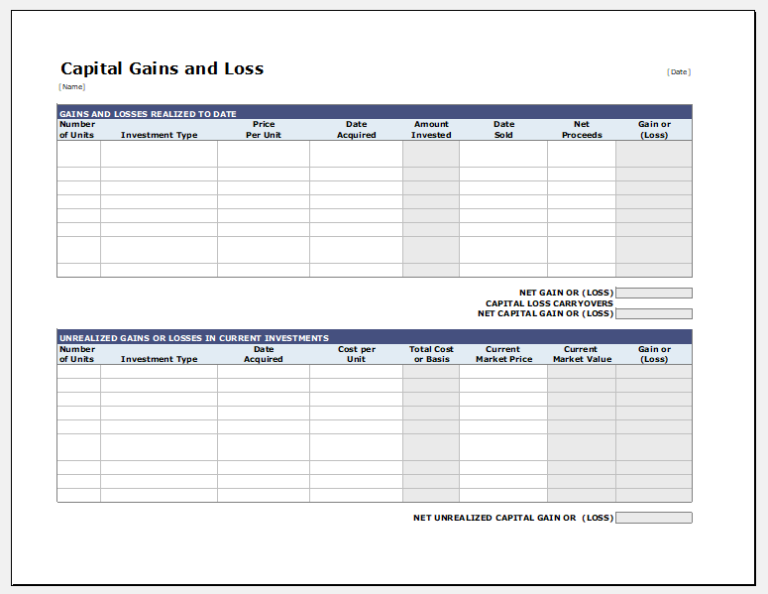

Capital Gains And Losses Calculator Template For Excel Templates Preparation Of Account Balance Sheet Mysql Alter Table Change