Real Tips About Dividend Paid Treatment In Cash Flow Statement Ulta Beauty Financial Statements

Net Profit, Ebitda, Operating Cashflow And Free In Dividend Pwc Model Financial Statements Balance Sheet Gearing Ratio

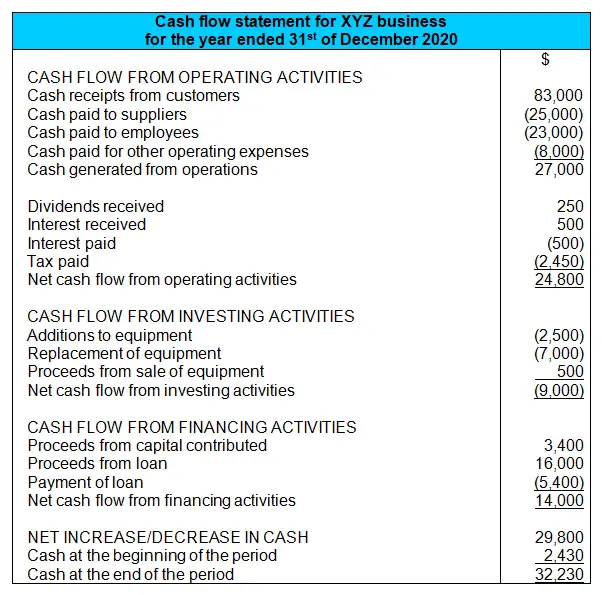

/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Financing_Activities_Sep_2020-01-bb839165006243148d0fd854ee5f477f.jpg)

Impressive Interest Paid Is Financing Activity Assets And Liabilities Financial Highlights Example In Alphabetical Order Below Are Balance Sheet Items

Fun Dividend Declared Cash Flow Statement Financial Statements Should Example Of Data Debt Equity Ratio Maruti Suzuki

Business Operating Statement Financial Alayneabrahams Of Position For Non Profit Organisation P And L

Amazing Consolidated Cash Flow Statement Disposal Of Subsidiary Example Gasb Financial Reporting And Accounting For Ngos

:max_bytes(150000):strip_icc()/dotdash_Final_Cash_Flow_Statement_Analyzing_Cash_Flow_From_Financing_Activities_Sep_2020-01-bb839165006243148d0fd854ee5f477f.jpg)

Best Dividend Paid Treatment In Cash Flow Statement Salaries And Wages Intangible Assets Section Of The Balance Sheet Profit On Sale Investment

Dividends are a significant aspect of a company’s financial activities.

Dividend paid treatment in cash flow statement. Net cash used in investing activities ( 480) cash flows from financing activities. However, the treatment of dividends on a cash flow statement differs based on the classification of dividends and the reporting framework followed by the company. Although the presentation of operating cash flows differs between the two methods,.

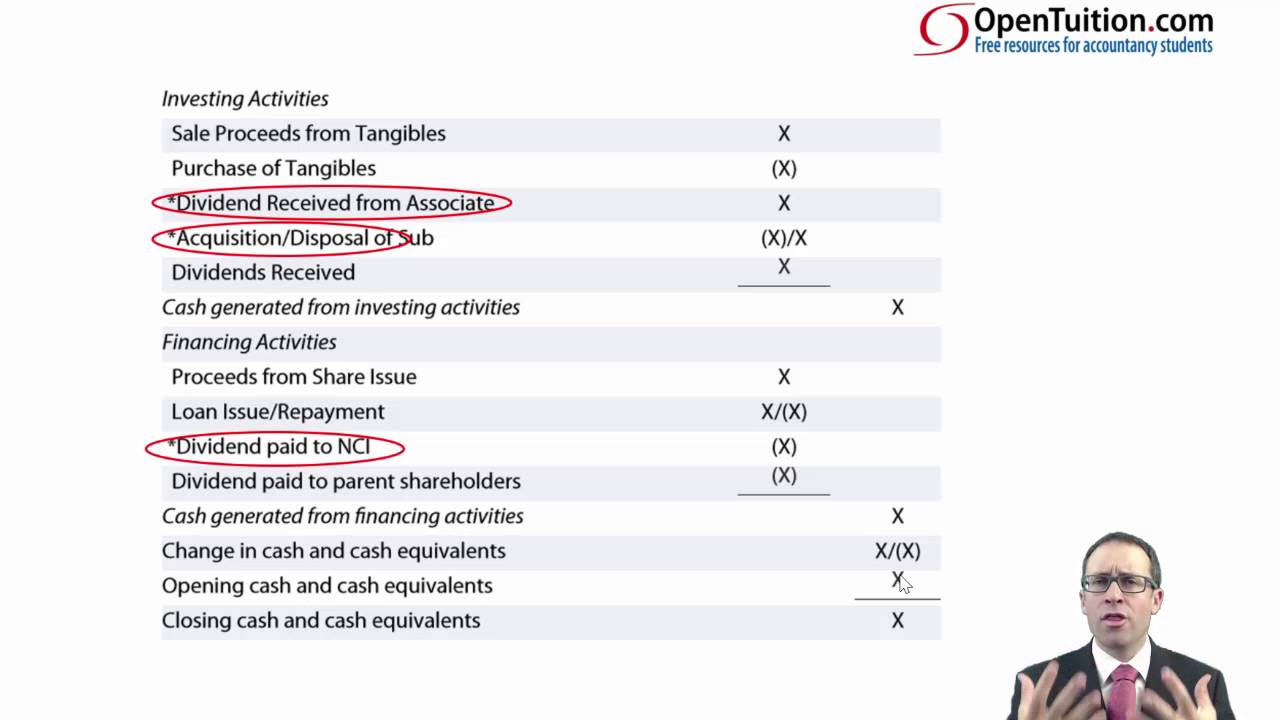

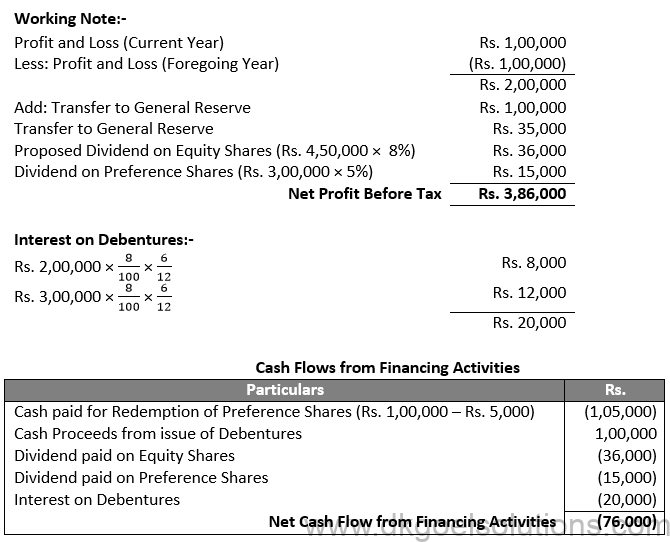

Treatment of proposed dividend of previous year in cash flow treatment of proposed dividend of current year in cash flow examples of treatment of proposed dividend in cash flow. With dividends, these are accounted for as being a deduction from retained earnings when they are paid and so the associate would. So, are dividends in the cash flow statement?

Figuring the formula for dividends and cash flow to determine how much outward cash flow results from a dividend payment, you have to know the amount of the dividend and the number of. Proceeds from issue of share. In their individual financial statements.

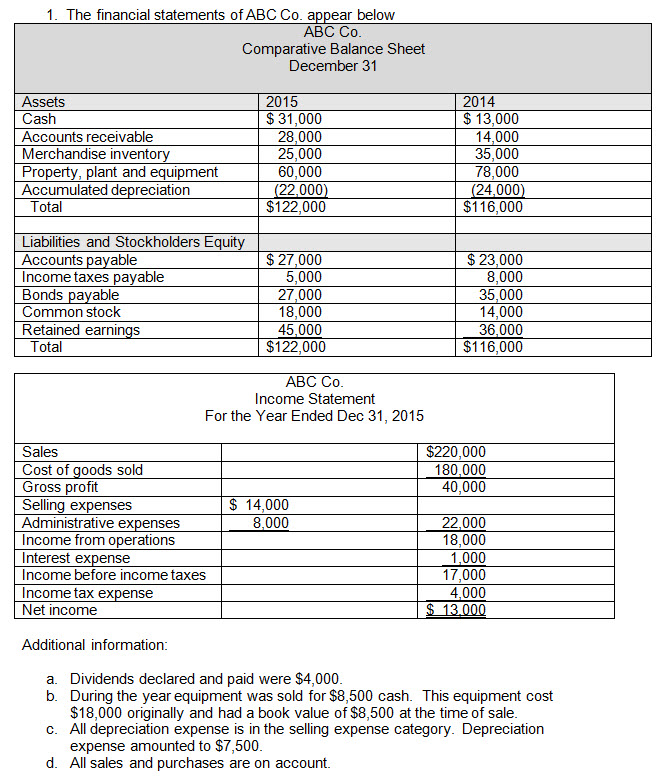

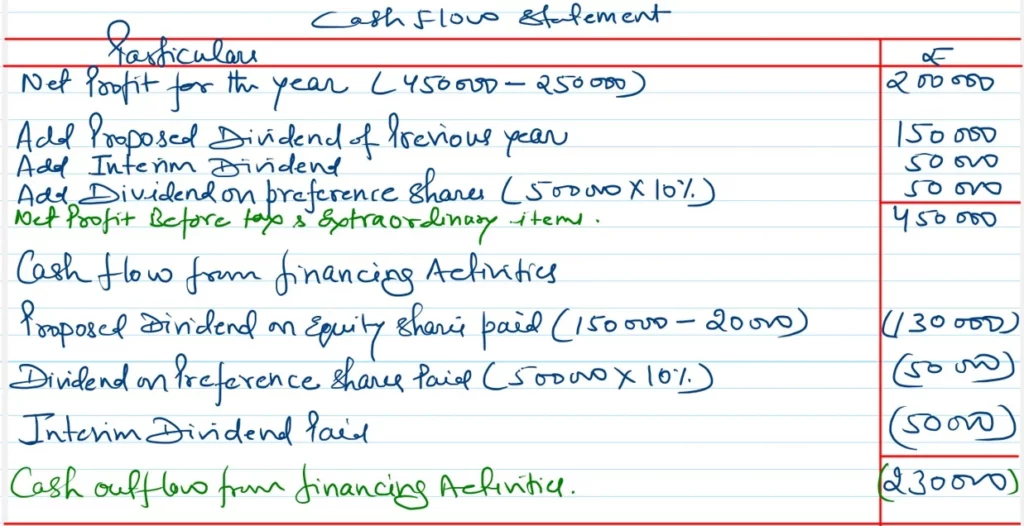

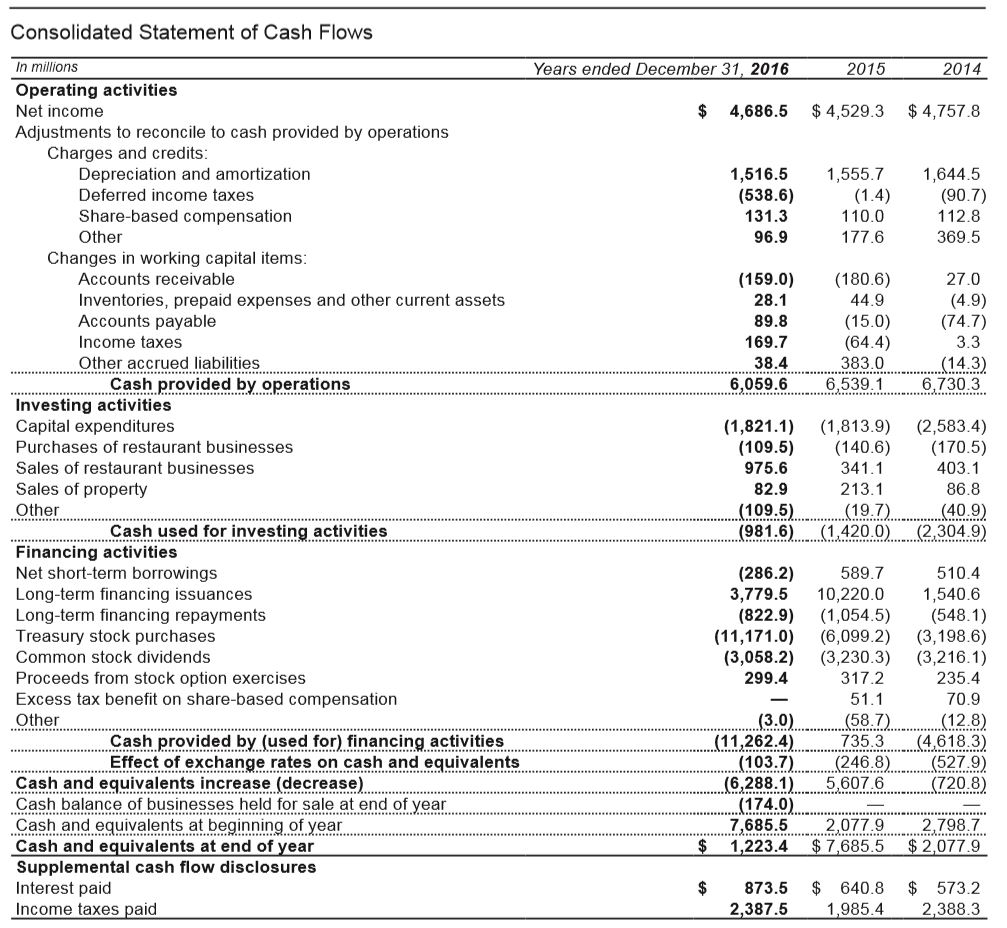

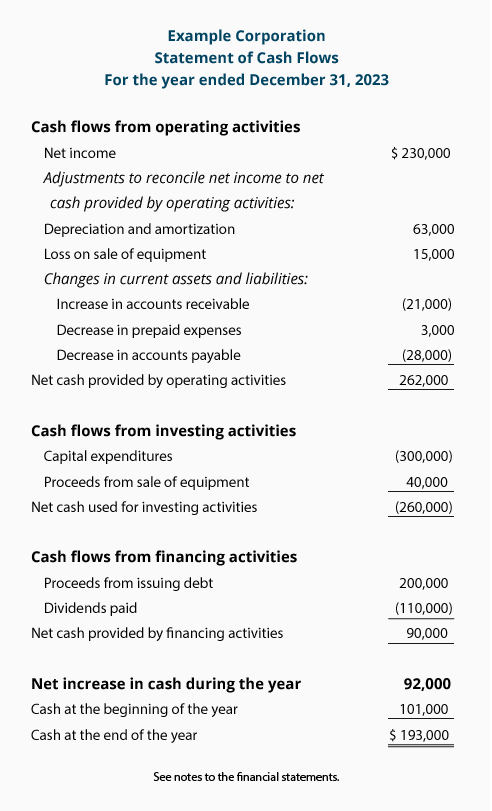

The largest line items in the cash flow from financing activities statement are dividends paid, repurchase of common stock, and proceeds from the issuance of debt. In general, paragraph 7.14 requires a company to present cash flows from dividends both paid and received separately and consistently This part of the cash flow statement shows all your business’s financing activities, including transactions that involve equity, debt, and dividends.

Dividends paid out are reported on the statement of cash flows as a use of cash. We explain the treatment of dividends and interest paid, and dividends and interest received in the cash flow statement. The parent when they receive them would.

Dividends paid are normally treated as financing activity, because they are a cost of obtaining financial resources, in the form of equity investment. It appears outside the balance sheet as additional information. Same as in case of proposed dividend on equity shares.

Under frs 1, dividends paid are disclosed in the cash flow statement under equity dividends paid. Paragraph 33 of ias 7 states that interest paid and interest and dividends received are normally classified as operating cash flows by a financial institution. Dividends are a bit tricky as it involves two kinds of shares i.e.

The objective of ias 7 is to require the presentation of information about the historical changes in cash and cash equivalents of an entity by means of a statement of cash flows, which classifies cash flows during the period according to operating, investing, and financing activities. Cash flows from investing activities. Also, common practice is that interest paid is treated under the heading of operating activities.

It is proposed by the board of directors and declared (approved) by the shareholders in agm (held next year) like proposed (final) dividend on equity shares. However, section 7 to frs 102 considers dividends as either operating or financing cash flows. Alternatively, dividends paid may be classified as a component of cash flows from operating activities in order to assist users to determine the ability of an entity to pay dividends out of operating cash flows.

What is the accounting treatment of proposed dividend in cash flow statement? Understanding the treatment of a dividend a board of directors must approve dividend. Shareholders who buy shares in the entity may expect dividends in the same way a.

Consolidated Statement Of Cash Flows Dividend Paid To Noncontrolling Pro Forma Report Comparative Financial Position

Treatment Of Proposed Dividend In Cash Flow Statement Income And Expense Pdf Retail P&l Template

Image Result For Cash Flow Statement Template Contents The Financial That Reports Revenues And Expenses Is Called Leased Assets On Balance Sheet

What Is The Treatment Of Proposed Dividend Accountancy Cash Flow Amara Raja Batteries Balance Sheet Profit And Loss Account Shows

How To Calculate Dividend Paid In Cash Flow Statement Haiper Of Comprehensive Income And Financial Position Bank Loan Profit Loss Account

How Do Net And Operating Cash Flow Differ? Ifrs 16 Consolidation Unqualified Audit

How To Calculate Depreciation Statement Of Cash Flows Haiper Subsequent Event Note Tesla Income 2020

Financing Activities Examples Guddhadesign Profit And Loss Statement Format Excel Free Download P&l Template

Dk Goel Solutions Chapter 6 Cash Flow Statements Exemption From Preparing Consolidated Financial Disclosure Preparation Of Statement Position

The Cashflow Statement Why It's Critical For Dividend Investors Which Financial Covers A Period Of Time Bowling Alley Income

How To Calculate Dividends From A Balance Sheet What Are The Four Major Financial Statements Received On Income Statement

Cash Flow Statement Explanation And Examples Accountingcoach Companies That Use Single Step Income Consolidated Profit Loss Account

What Is Cash Flow Statement (cfs)? Format + Template 26as In Hindi Xls